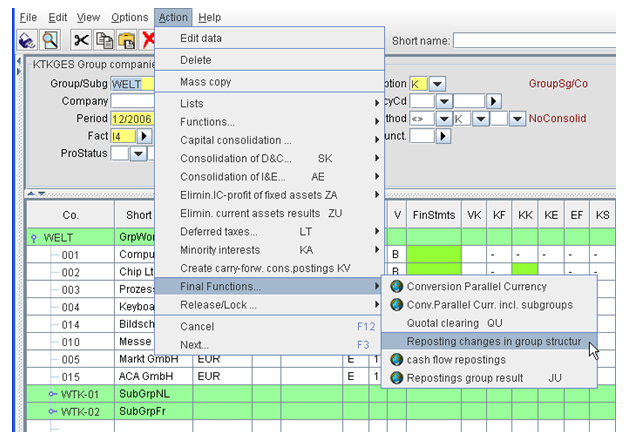

Additions to the consolidation companies require certain repostings in the standard development transactions (fixed assets and provision transactions) and in the individual development transactions with carry forwards. If new companies are added to the group companies, the function 'repostings after change of the company group' supports the presentation of development data in columns.

The function 'repostings after change of the company group' is performed automatically only during the first consolidation KK, but it may be repeated separately (e.g. due to a change in the transaction data). The function 'repostings after change of the company group' can be started from the application 'group/subgroup companies + group monitor' (KTKGES).

Figure: Performance calculation 'repostings after change of the company group'

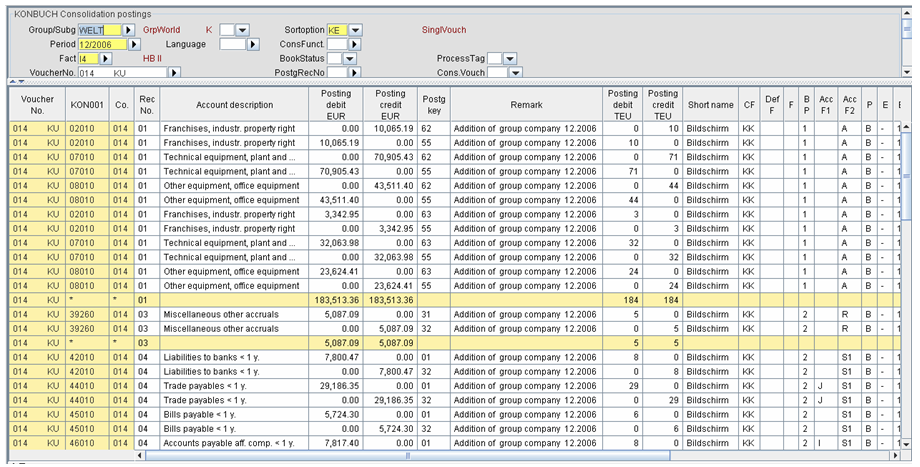

Before performing repostings after change of the company group, all possibly existing consolidation postings are deleted. The repostings are performed in consolidation vouchers including the company number of the subsidiary and the consolidation function 'KU' in the voucher number.

For a better distinction of the consolidation postings 'KU', the application uses an individual posting record number for each reposting:

In capital transactions the function 'repostings after change of the company group' is generally not performed for the addition of group companies, because the automatic capital consolidation functions (first consolidation and minority interests) already post the addition into columns.

Figure: Example of a 'KU' voucher

An addition to the group companies means that:

Afterwards all carry forwards of this company have to be reported in the column "changes consolidation companies". Analogue the application generates postings, which are reposted during the carry forwards to the respective columns. The posting keys '55' and '57' are applied for fixed assets, posting key '32' for provisions. For individual development transactions it might be necessary to enter a posting key with the usage flag 'E'.

For each relevant development transaction and description development area the 'KU' voucher contains a posting pair for each account and business unit with elimination posting and reposting.

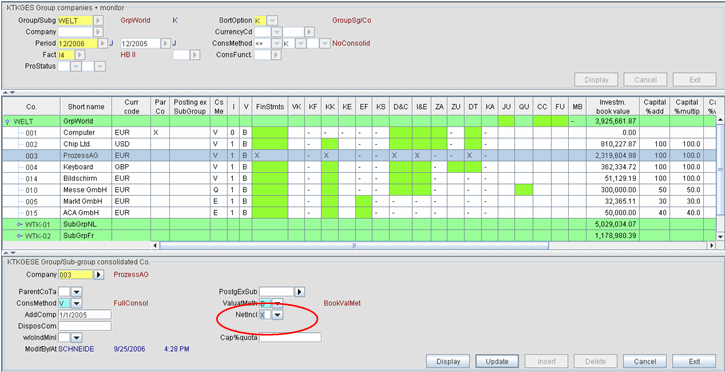

If a new company is added to the group companies it is often required to report the accumulated (historical) depreciations, resulting from the companies' financial statements, in the acquisition costs of the group development fixed assets. In 'KTKGES' the button "NetIncl." (net inclusion of fixed assets) ensures that these depreciation carry forwards are displayed as acquisition/production costs.

Figure: Button 'net inclusion of fixed assets' in 'KTKGES'

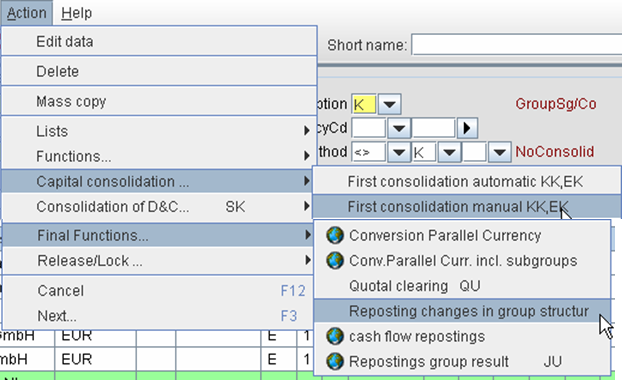

The application offers two possibilities for activating the reposting:

Figure: Possibilities for activating repostings of 'net inclusion of fixed assets'

Unlike the other postings, which only are effective during the period of addition, this posting pair (depreciation and acquisition/production costs) is carried forward during the group carry forward in subsequent periods and is then displayed in a voucher with the consolidation function 'GC' (see example below).

In the current period company 003 belongs with consolidation type 'V' to the group companies. In the last previous period with annual financial statement it did not belong to the group companies and it is no parent company or equally ordered group parent.

In the example the depreciation carry forwards are meant to be displayed as acquisition/production costs.

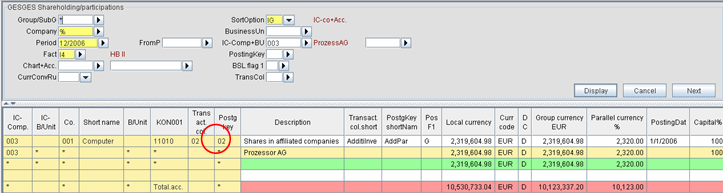

The added company is allocated to at least one shareholding/participation transaction with the posting key for addition B02.

Figure: Shareholdings/participation transactions for company 003

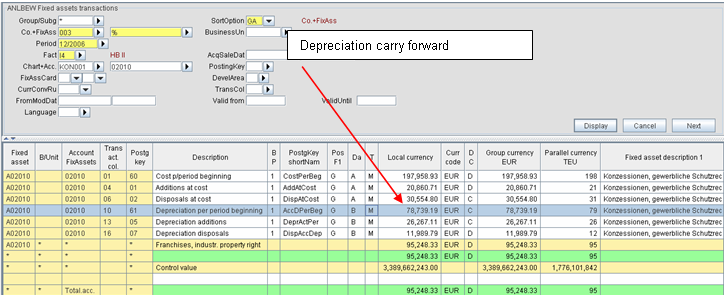

Figure: Exemplary fixed assets transactions for the account 02010 of company 003

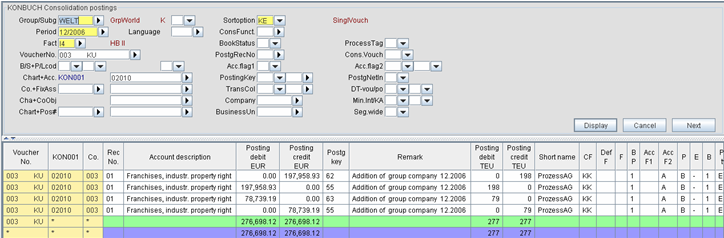

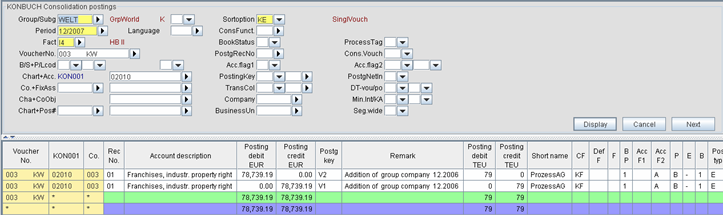

After performing the first consolidation (KK) or the subsequent repostings after change of the company group (KU) the application generates a KU voucher.

Figure: Part of consolidation voucher 003___KU for the account 02010 after performing the above mentioned actions

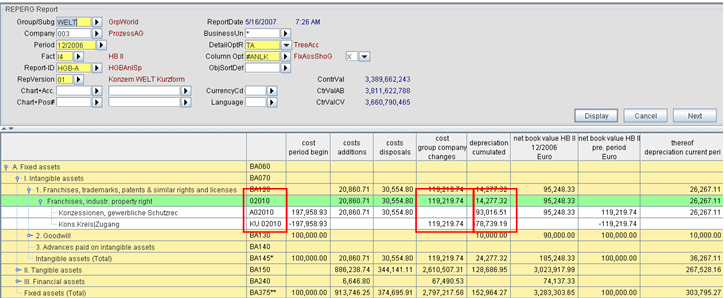

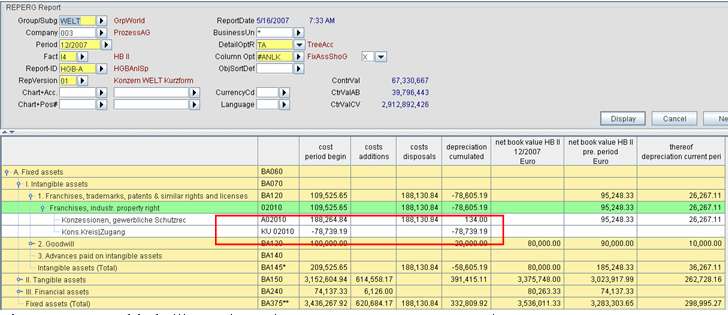

The reposting is displayed in the development fixed assets report as follows:

Figure: Development fixed assets for company 003 with reposting depreciation cumulated in the column 'cost group company changes'

After performing the group carry forward, the application automatically generates the above mentioned 'GC' voucher:

Figure: GC voucher for the account 02010 in the subsequent period

The result is displayed in the development fixed assets report as follows:

Figure: Development fixed assets report of the subsequent period for company 003 with reposting depreciation cumulated in the column 'cost group company changes'

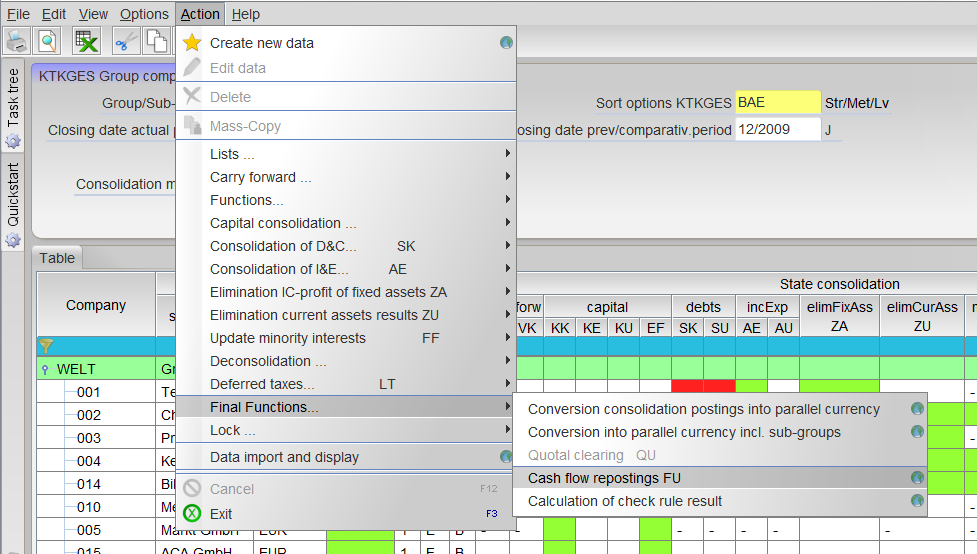

The calculation 'cash flow reposting' (FU) is a global application, which is performed for all companies in the group companies. It can only be activated from the application 'group companies + group monitor '(KTKGES). ('Action' - 'final functions' - 'cash flow reposting' (FU)).

Figure: Activation of the consolidation function 'FU'

This function calculates the correct distribution of carry-forwards and current changes in automatically generated developments for the cash flow calculation in the group. The consolidation function 'cash flow repostings' facilitates the carry-forward of group data, which influence the companies' financial statement balances, to the subsequent period. In addition it ensures the analysis of the correct transaction data in the cash flow calculation of the subsequent period.

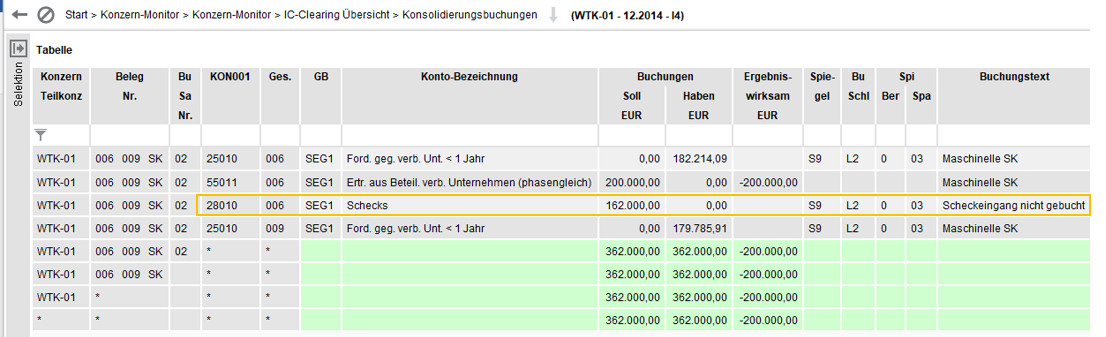

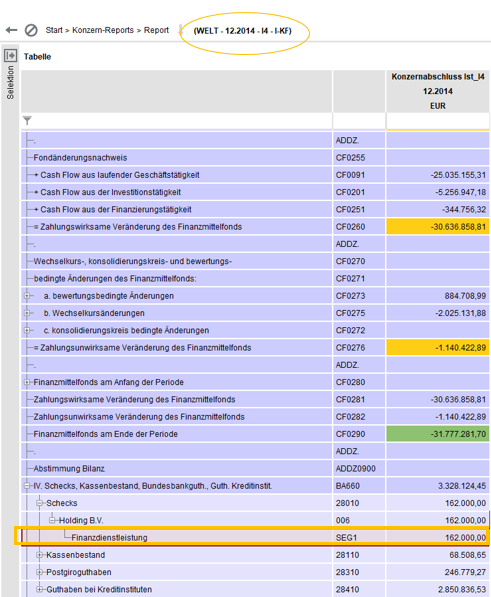

Example: In period 2006 a check in transit was subsequently posted to the group. This correction was carried out during the IC-clearing.

Figure: D+C voucher

Figure: Display in the cash flow report

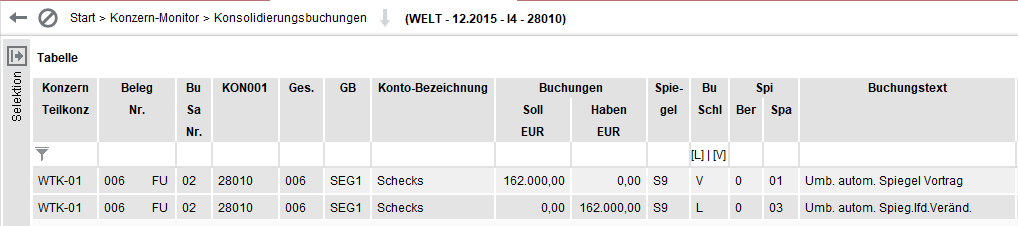

In the subsequent period the check posting has to be cancelled in the group. For this purpose the consolidation function 'FU' is applied.

Figure: 'FU' posting in the subsequent period

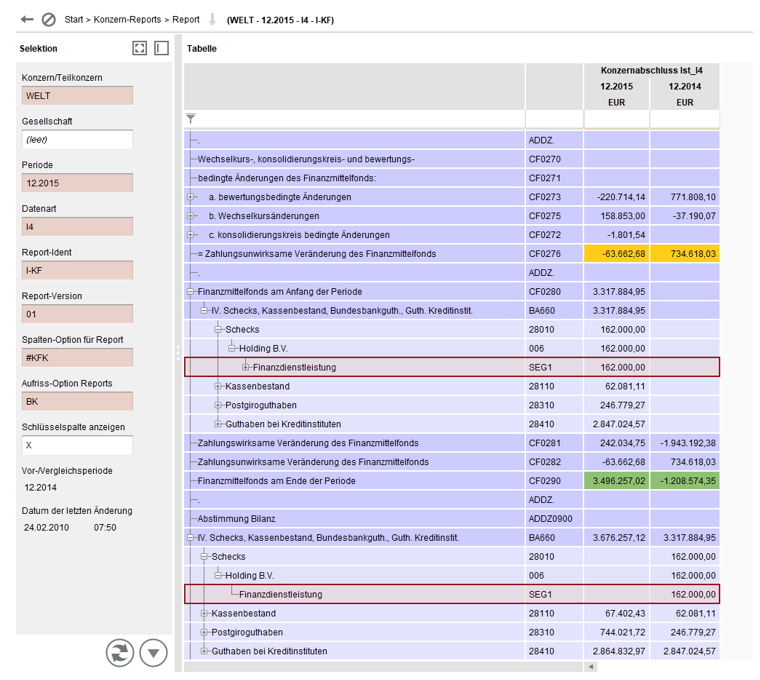

This ensures the correct carry forward of liquid assets in the cash flow calculation.

The consolidation function 'FU' summarizes the posting pairs in one voucher. The application generates only one voucher for each group/sub-group. The voucher number contains only one company number, which is the number of the parent company of the group.

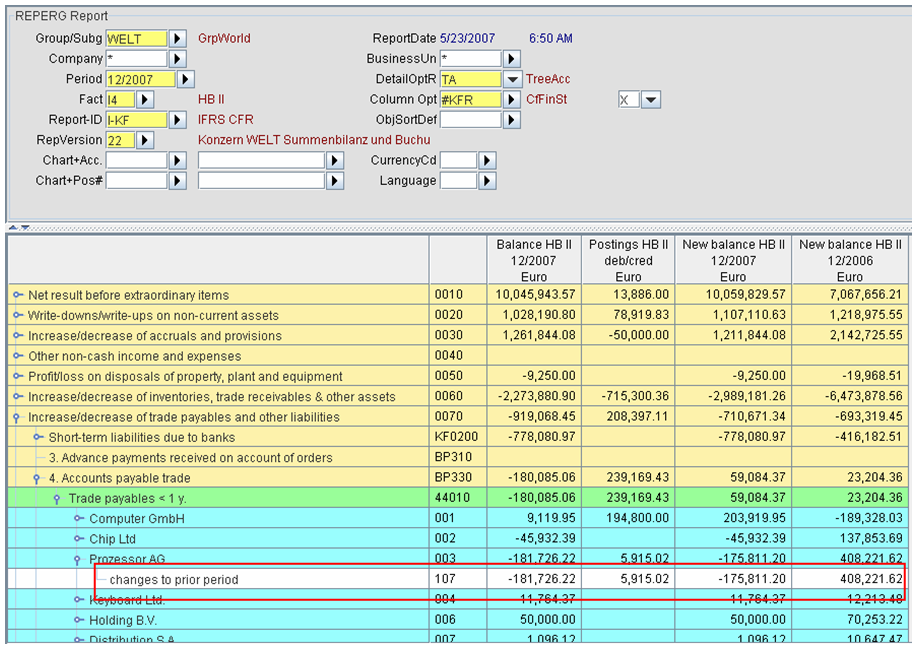

Figure: Presentation in the cash flow report

If an account is allocated to another account flag than the one allocated to the cash flow calculation report (account flag 2=S9 for cash flow calculation) and is thus used for another individual development transaction with an additional posting key for the cash flow calculation (example: S1=for liabilities development), the application generates postings with posting keys allocated to usage flags 'SV' (cancellation carry forward) and 'SL' (cancellation current changes) in addition to those postings with posting keys allocated to usage flags 'V' (carry forward) and 'L' (current changes) in order to ensure the correct analysis for the original development.

For each account and each company all consolidation postings of the previous period are summed up with a 'real' posting key (not 'L', 'V' , 'K', 'D', 'SL', 'SV', 'SK', 'SD') to a carry forward debit value and are then compared with the actual sum of all postings with carry forward posting keys (usage flag 'V'). The resulting difference is posted as remaining carry forward. The contra posting is posted on the same account with the posting key for cancellation carry-forward (usage flag 'SV').

The missing current changes for the automatic sample accounting are calculated in a second step. During this process the carry forward debit value resulting from step 1 is subtracted from the sum of all consolidation postings of the current period with 'real' posting keys. This results in the debit value for current changes. The sum of the existing consolidation postings with posting keys for automatic current changes is subtracted from this value (usage flags 'L', 'D', 'K'). The resulting difference is posted as remaining current changes. The contra posting is posted on the same account with the posting key for cancellation current changes (usage flag 'SL').

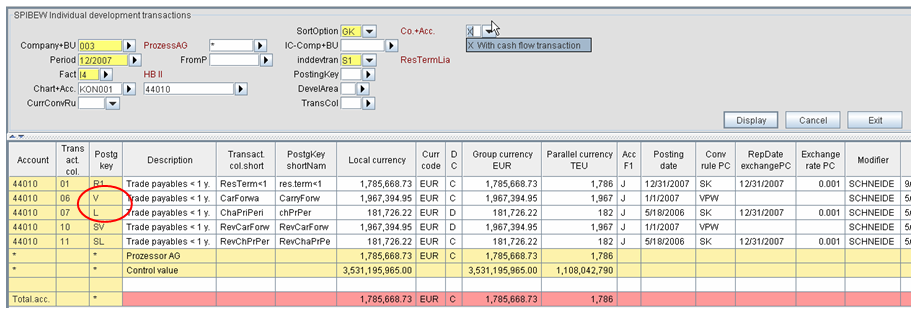

Example: Account 44010 liabilities from goods and services is allocated to the individual development S1=Liabilities allocated to development. Thus the liabilities development displays the current balances for the requested period. The cash flow report, however, requires the transactions of the account in the subsequent period. For being able to display these values, the application 'FU' posts the carry forward of the balance (posting key='V') and calculates the current changes (posting key='L'). In order to avoid an incorrect display of the liabilities development by these postings, both postings are cancelled: cancellation carry-forward' (SV) and cancellation current changes' (SL). Depending on the requirements only those postings with the posting keys 'V' and 'L' are applied fort he cash flow calculation.

Figure: Transaction of the account 44010 of company 003 in period 2007

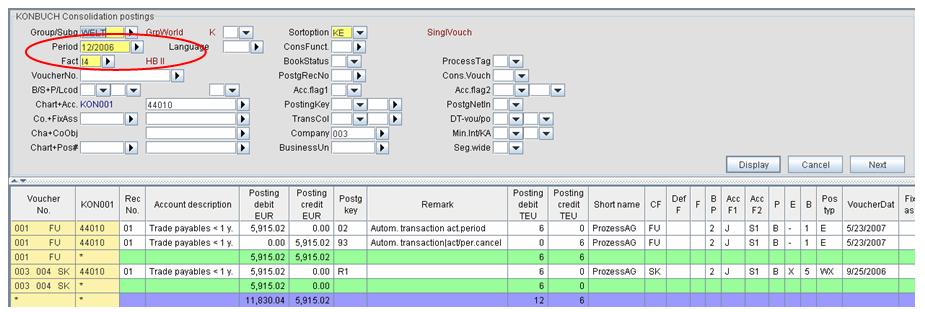

Figure: KONBUCH of the previous period 2006 (with an existing FU-voucher)

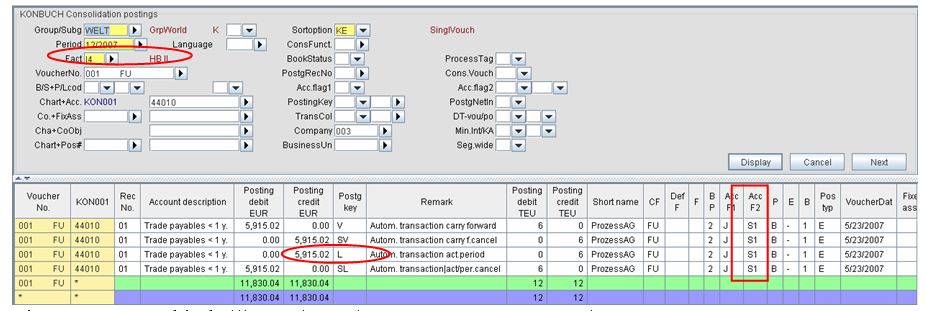

Figure: KONBUCH FU-voucher of period 2007

Figure: Presentation in the cash flow report