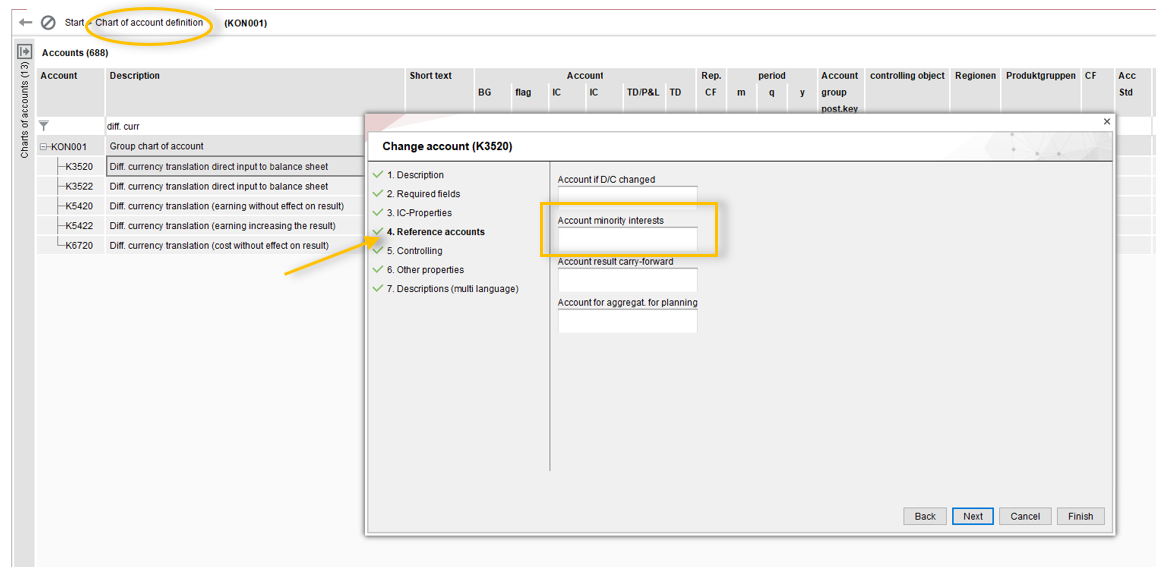

In order to be able to display minority interests per capital account there is an option, in the account master, to assign a separate minority interests account to each capital account. The pre-requisite is that an FK parameter has to have been created. When a minority interests account is directly assigned to the capital account, in the account master, this account will then be used for postings related to minority interests.

If the minority interests account is assigned a further minority interests account then the latter will be referenced to the first account.

This option applies not only for the calculation of direct minority interests but also for indirect minority interests.

Image: Entering an individual minority interests account per capital account

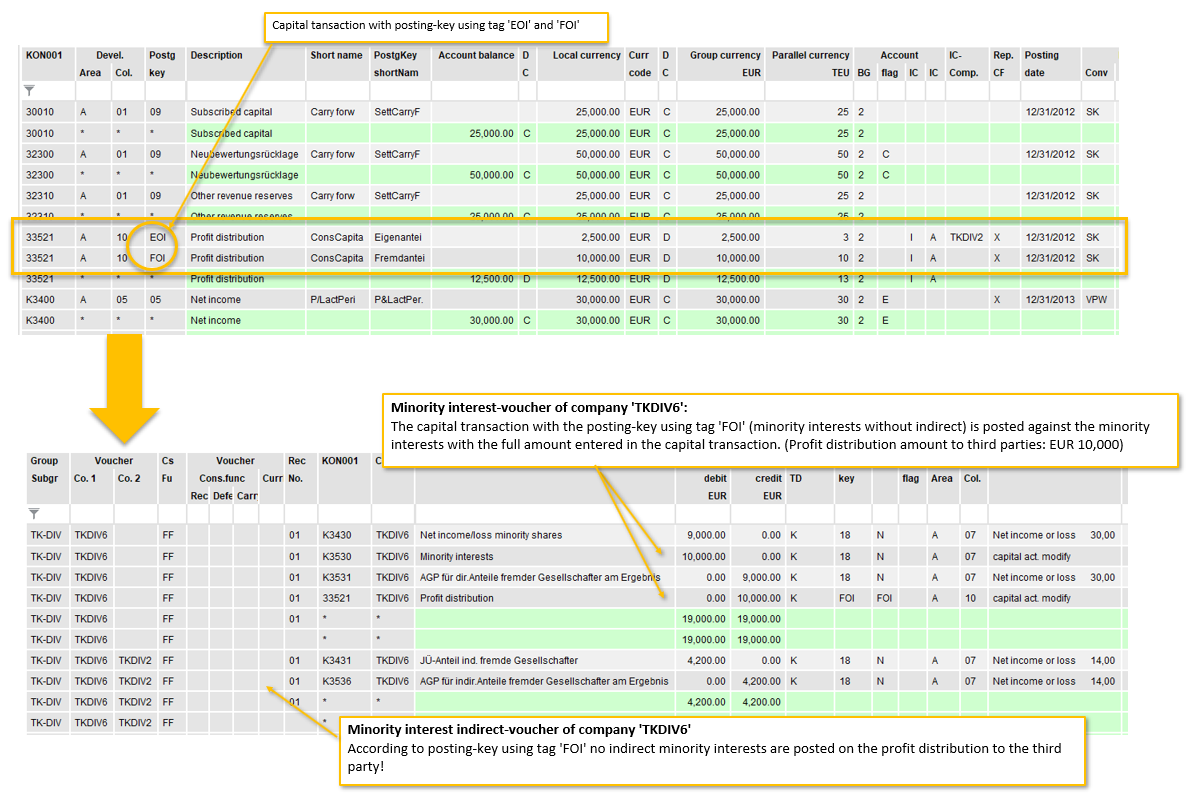

There is basically an option to control the calculation of minority interests via a posting key usage tag (BSL usage tag). The program will then deviate from automatic processing and will execute calculations on the basis of the posting key with the respective usage tag. The amounts that are posted will be those that have been updated in the capital transactions.

The following posting key usage tags can be used for this:

It makes sense to use this posting key where, e.g., dividends are distributed with different participation percentage rates, fixed dividend amounts are contractually agreed or, e.g., capital increases have to be allocated only to owners or external shareholders.

A parent company holds 70% of a subsidiary. It is agreed that the minority shareholders will receive a dividend in the amount of 80% of the net income for the year. If no action is taken in the system then the minority interests in the dividend would be calculated at 30% in accordance with the participation percentage rate. Now, in order to configure control of the dividend that is not subject to the participation percentage rate, you will have to use specific posting key usage tags that you can draw on to update capital transactions for the dividend payout procedures.

In the simplified example, a parent company holds 70% of a subsidiary and thus 30% is owned by minority shareholders. The subsidiary pays out a dividend of EUR 12,500. In this case, the parent should receive just 20% of the dividend (thus EUR 2,500) and the minority shareholders 80% (thus EUR10,000). The minority shareholders should not participate indirectly in the dividend payout. The dividend to the parent company is eliminated via the SD by entering the IC-GES in the KAPBEW for the dividend amount of EUR 2,500. You must ensure that the income from participations account to which the parent company makes postings is NOT included in the consolidation parameter FK.

The following posting key usage tags are available in such a case:

After updating the capital transactions and triggering the 'Update Minority Interests' action the following FF voucher is generated:

If the aim is to also post indirect minority interests to changes in equity in the following period then this can be achieved via the the posting key usage tag 'FF'. Capital transactions that are updated with this posting key are used in the 'Update Minority Interests' action for the calculation indirect minority interests. The counter posting is made to the respective minority interests account in the consolidation parameter 'FK'.

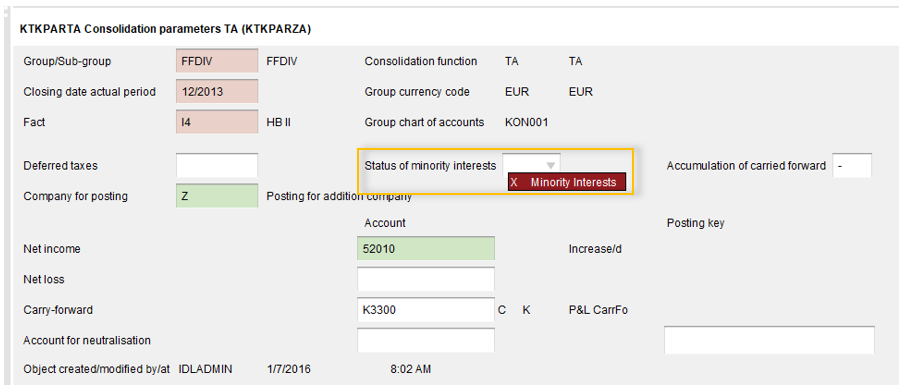

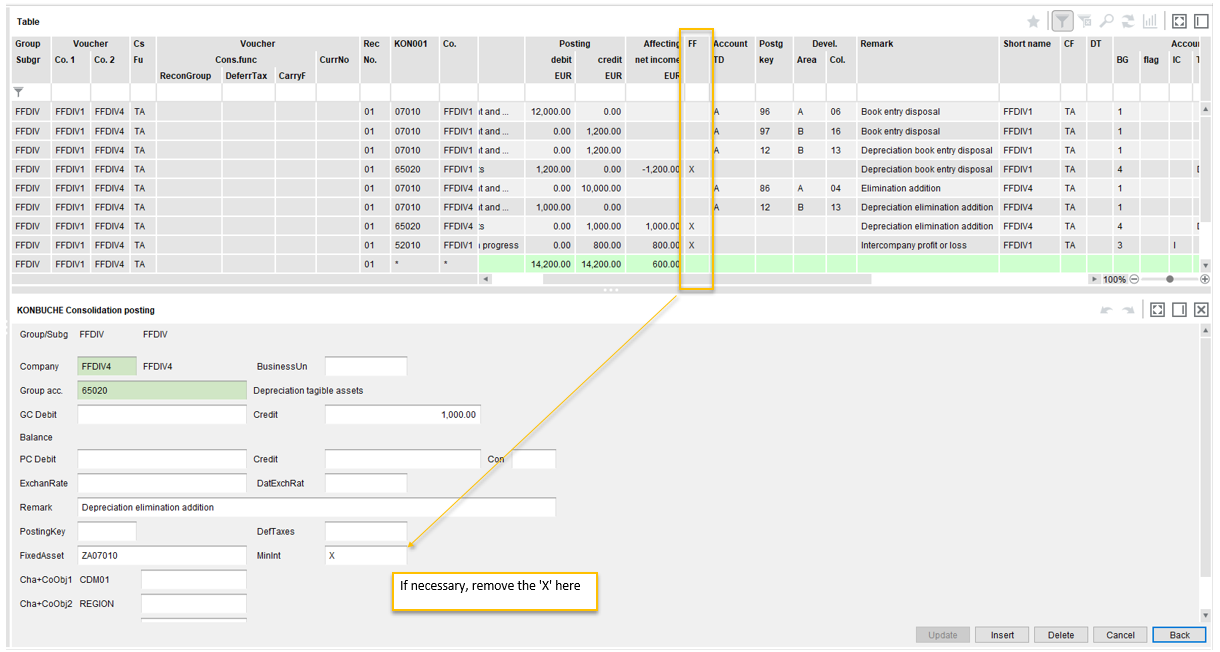

If the aim is to calculate minority interests in other income-affecting consolidation postings (TA, ZU, MB, LT, SK, AE postings) then this can be initiated via the respective consolidation parameter. An 'X' has to be placed there in the respective consolidation parameters in the 'Minority Interests' field.

Image: Example: Flag ZU parameter for the calculation of minority interests

IMPORTANT NOTE: Pre-requisite for posting within the minority interests: in the consolidation parameter 'FK', an account has to be entered in the 'Elimination of Net Income-Affecting Consolidation Postings, direct/indirect' field

NOTE: Disabling the calculation for individual posting rows: if the aim is not to use individual postings in a voucher for the calculation of minority interests then, via an individual record in the consolidation posting application (KONBUCHE), the 'FF' entry can be removed in the respective posting row.

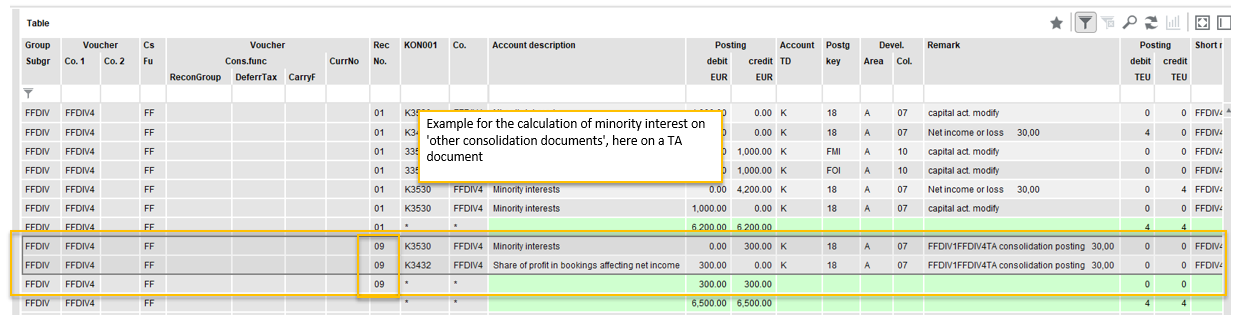

Postings under posting record number 09: If the calculation of minority interests is triggered according to the indicators on the vouchers then the minority interests voucher can be extended by postings with the posting record number 09.

The posting of a share of profit or loss that is attributable to external shareholders is made to the account specified, in the consolidation parameter 'FK', in the 'Elimination of Net Income-Affecting Postings' field. The counter posting for the direct and indirect minority interests is made either to the 'Minority Interests in Profit or Loss' account defined in the consolidation parameter 'KF', or, provided that no accounts have been defined there, to the mandatory account 'Minority Interests'. It is not possible to control the posting via the account master because this is an income account.

In contrast to postings to P/L accounts, with capital accounts the elimination takes place in the capital accounts themselves. The counter posting takes place either in the account master in the minority interests account defined in the capital account, or in the 'Minority Interests' account in the consolidation parameter 'FK'.

Currency conversion effects on these postings? : No currency conversion effects are taken into account for these consolidation postings because the original income-affecting consolidation postings were already available in the group currency.

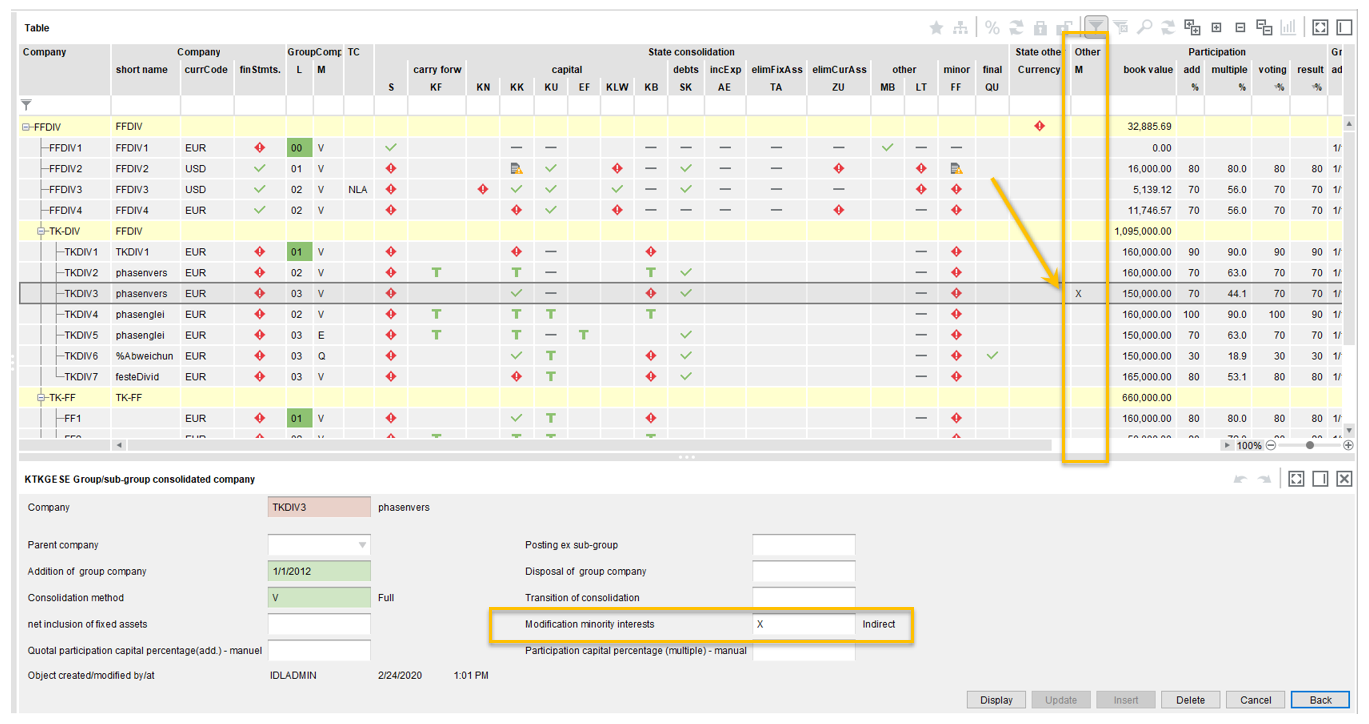

There is the option of disabling the calculation of indirect minority interests for each company. In the single record application 'KTKGESE' (or in the wizard for the application KTKDEF), by placing the indicator 'X' in the field 'No Indirect Minority Interests' it is possible to control whether or not indirect minority interests should be posted for a company. Following the placing of an 'X' in the above-mentioned field, an additional column becomes visible in the group companies + monitor. An 'X' will appear there for those companies for which the indirect minority interests calculation has been disabled.

There is the option of disabling the calculation of minority interests on the pro-rata annual profit or loss for a group or likewise just for one company. For this the following settings, which deviate from the standard ones, are required:

You can disable the calculation of minority interests in goodwill by removing the offsetting account specified for this in the consolidation parameter FK. This will then apply to all the companies in the group/sub-group.

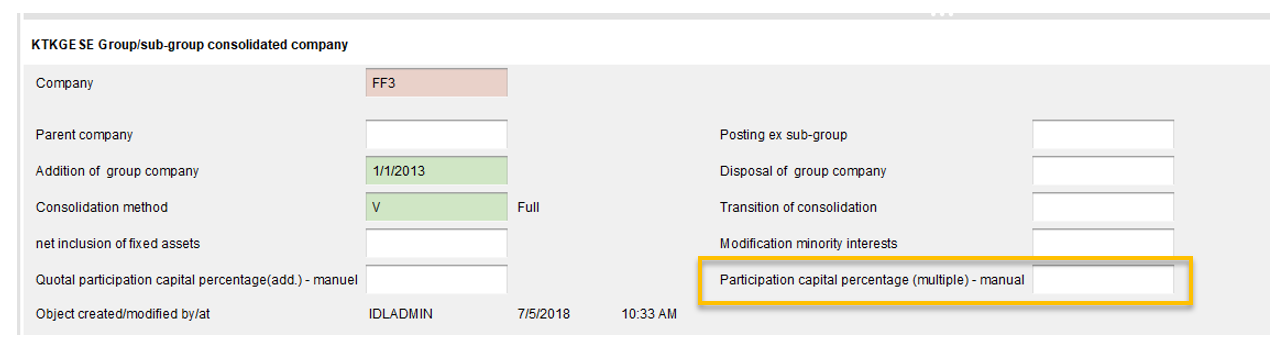

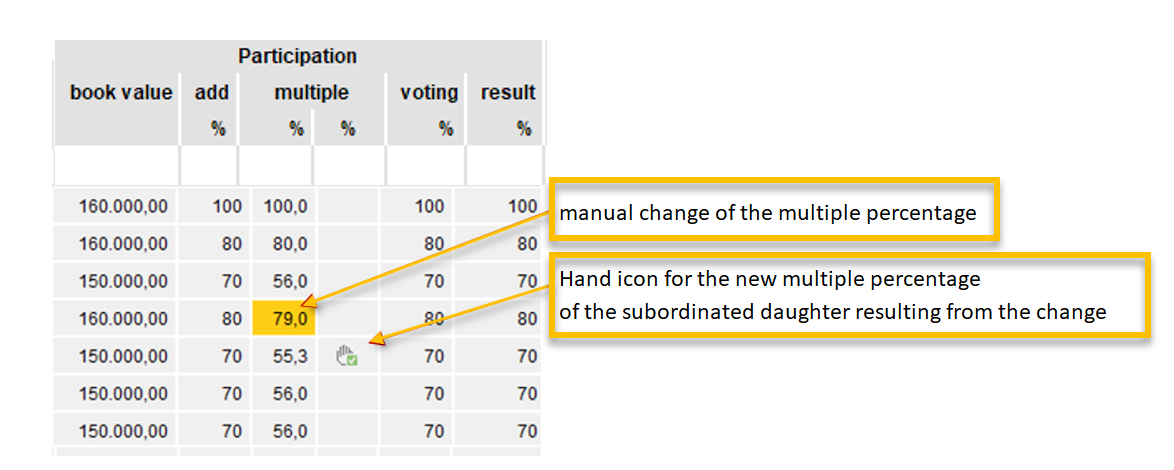

If there are recursive participation structures then the system will not display a value in the 'Multiple % Rate' field. The field is then highlighted in yellow. If, on account of recursive participation structures, or also other contractual situations, multiple participation percentage rates have to be calculated differently from the way that percentage rates are calculated automatically, by the system, then individual multiple percentage rates for each company can be defined via an individual record in the group companies + monitor or the wizard for the application KTKDEF. This is possible for all companies except for the parent company.

Image: Manual entry of multiple percentage rates in KTKGESE

Values that have been entered manually are primarily used for the calculated values. This applies for the calculation of minority interests (FF vouchers) as well as for determining the participation itself for the calculation of multiple shareholdings of dependent companies. A manually entered multiplicative percentage rate always has priority over one that has been calculated, i.e. for minor subsidiaries the calculation is done on the basis of the manually entered percentage rate of its parent company.

Following a manual change to a percentage rate, a new participation identification and status identification will happen automatically, in the background, in order to immediately determine the percentage changes for the dependent companies resulting from the change.

The manual changes are visualised by colour highlighting (yellow). The new multiple percentage participation rates of the dependent companies that result from the change are made visible by a hand icon in an extra column.

Image: Visualisation of manual change

The manually entered values are generally carried forward into the following period. Users are themselves responsible for adjustments in the case of any changes to participation relationships.

In the case of profit distributions by a company and income received from participations by another company it is possible to distinguish between two types of dividends and receipts that lead to different treatment of minority interests.

IDL.KONSIS supports the automatic inclusion of both types. The difference between the two types lies in the correct posting for the dividend.

In order for this function, the income from participations accounts used for the parent company have to be entered in the field "Dividend Income (same period)" and "Dividend Income (different period)" in the consolidation parameter FK. These income from participations accounts have to be maintained as follows:

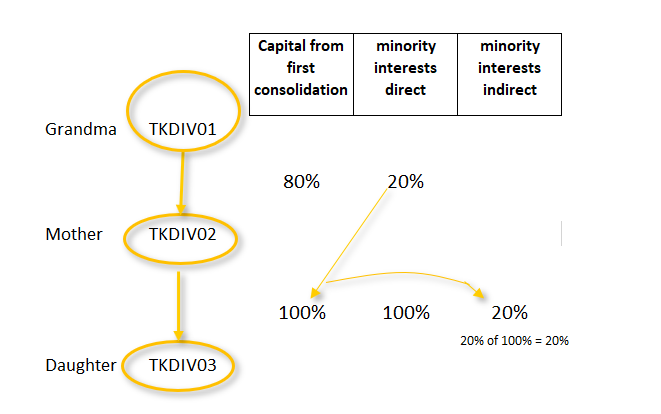

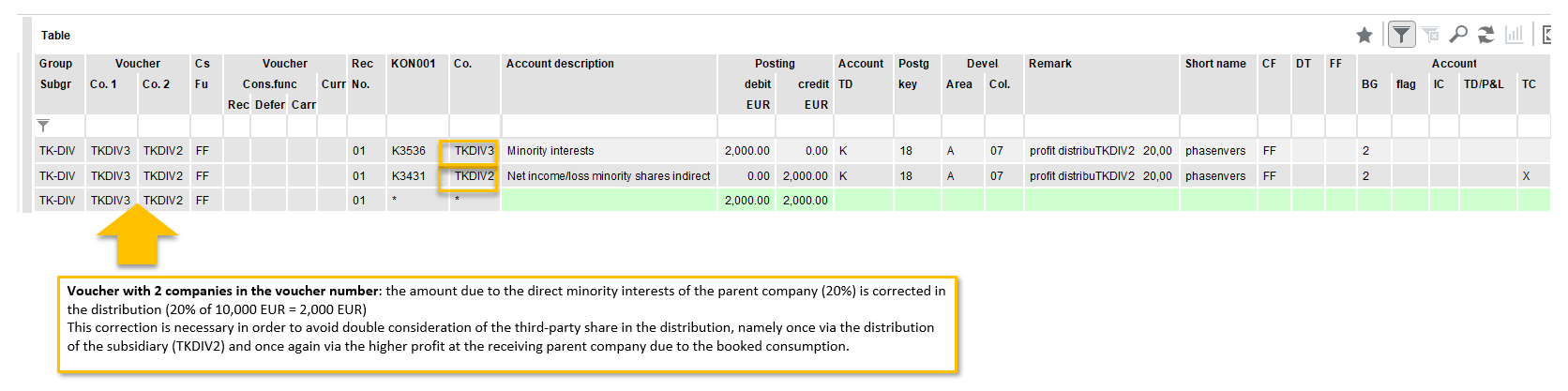

Case: In this simplified case, company TKDIV3 is 100% owned by company TKDIV2. CompanyTKDIV2 is only 80% owned in the group. Therefore, external shareholders indirectly hold 20% of company TKDIV3.

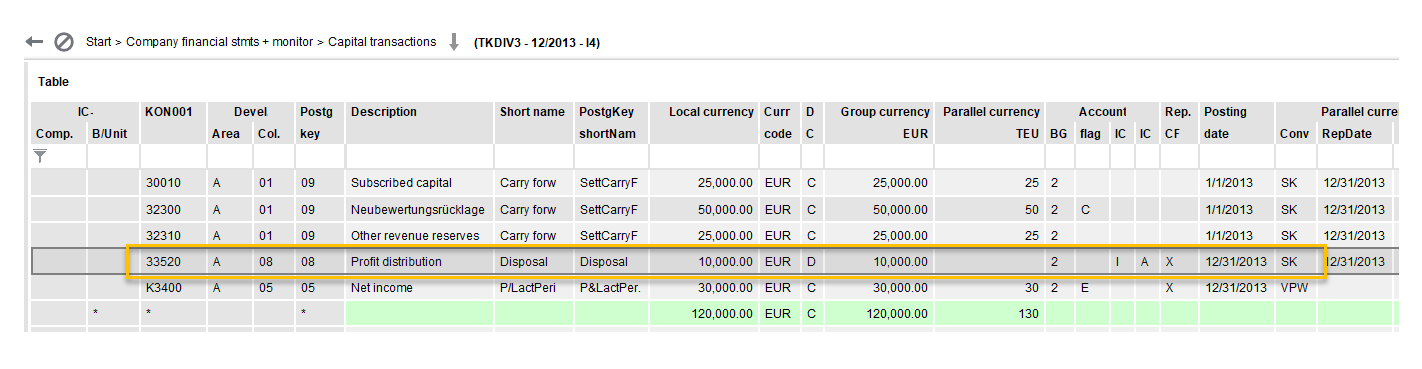

The subsidiary TKDIV3 has updated capital transactions by adding a dividend in the amount of EUR 10,000 with respect to company TKDIV2.

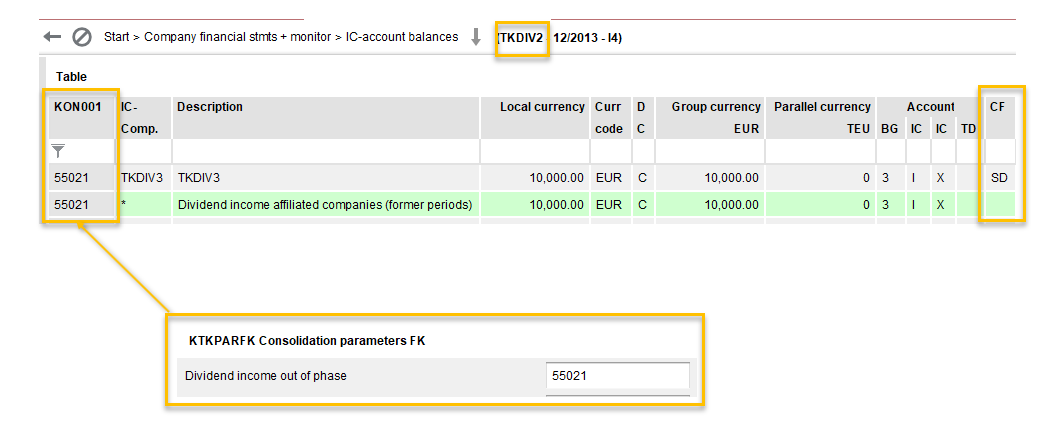

The parent company FFDIV2 has entered income from participations in the amount of EUR 10,000 into account 55021 with respect to the subsidiary TKDIV3 and in the IC account balances. (The calculation of minority interests is based on IC account balances that are run in these accounts with the consolidated company as an IC company)

After triggering the calculation of minority interests for company TKDIV3 the following voucher ensues:

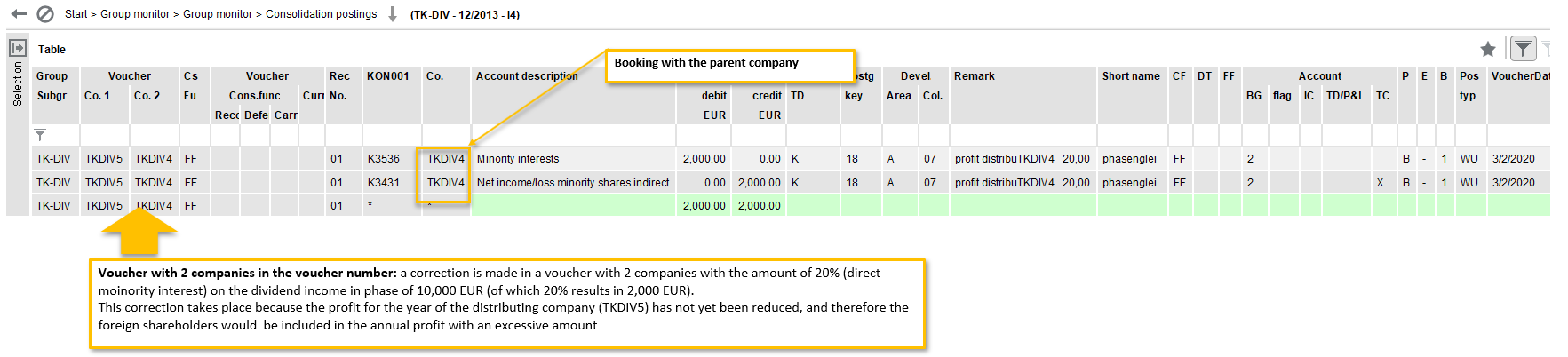

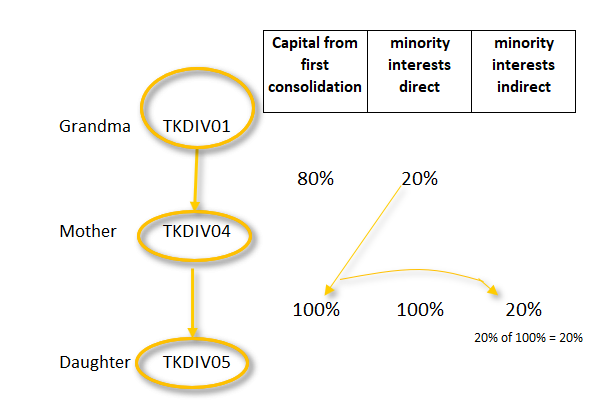

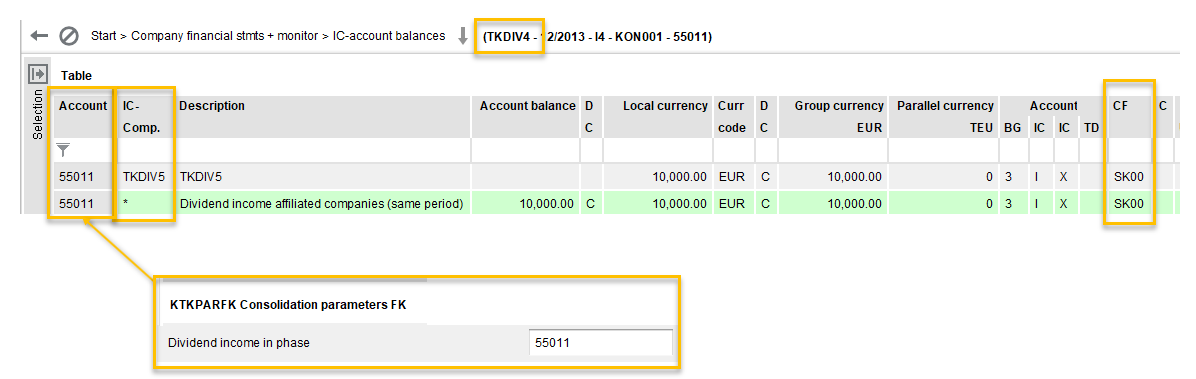

Case: Company TKDIV5 is 100% owned by company TKDIV4. CompanyTKDIV4 is only 80% owned in the group. Therefore there are indirect minority interests in company TKTIV5 via the minority interests of TKDIV4.

Company TKDIV04 has reported income from participations in the amount of €10,000 in account 55011 with respect to companyTKDIV05 whose parent company it is.

There are indirect minority interests in company TKDIV05 via the minority interests of TKDIV04. After triggering the calculation of minority interests for company TKDIV05 the following voucher is presented: