Depreciations on fixed assets can be posted automatically in both company financial statement postings (BUCH) and consolidation postings (KONBUCH), but also IC fixed asset transactions (ICANLBEW). This documentation describes what settings are possible and necessary in order for you to be able to do this.

To be able to generate depreciation postings automatically, the appropriate information must be stored in the fixed asset objects used. Separate fixed asset objects must be set up for both company financial statements and consolidation postings.

The fixed asset object must be set up for the company, the account and, if necessary, the group of the posting in the 'fixed asset objects' (ANLOBJ) application. If one of these parameters deviates from those in the posting, you will not be able to use this fixed asset object.

The purchase costs in the consolidation posting (KONBUCH) or company financial statement posting (BUCH) provide the basis for depreciations. This means there must always be a posting with a posting key from the transaction development area "purchase costs".

Basically, the depreciation posting will always be calculated in proportion to the current accounting period. This means that if the fiscal year ends on 12/31, only three months will be calculated and posted for the financial statement on 3/31 and only nine months on 9/30. The prerequisite for this, however, is that the period indicator must be entered properly in the -ABR+ application, due to the fact that the last period with a period indicator -Y+ will be taken into consideration as the annual financial statement.

If an depreciation posting type or other type of data that is of relevance to depreciation is changed, this will always have an effect on only the new postings that were generated using this setting. Previously generated depreciation postings will not change.

The following settings are available:

K = No automated depreciation: With this setting, no depreciation postings will be generated automatically

L = Straight-line depreciation Y: In this case, the purchase costs will be divided into unchanging amounts over the entire depreciation period (Y=year). The duration of the depreciation period can only be expressed in entire years.

M = Straight-line depreciation M: The system here is the same as with "L", however the depreciation period is to be entered in months (M), an aspect that indirectly makes it possible to enter half years.

SL = Straight-line depreciation Y with special depreciation: If an additional amount is to be depreciated for a period in addition to the current linear depreciation, the depreciation method must be changed from L to SL. Otherwise the linear depreciation will be suspended until the additional depreciation has been "used up".

SM = Straight-line depreciation M with special depreciation: Analogous to the SL setting, whereby the lifetime is to be entered in months

F = Fixed depreciation value:You must store the amount that is to be depreciated per business year. If the carrying amount is less than the depreciation amount stored at the end of the depreciation period, only this lesser amount will be generated. The fixed asset object will automatically be depreciated only up to its carrying amount = 0.00.

Basically, the depreciation postings will be generated automatically during recording of the basic postings. This does not require any other function to be performed.

If, however, the depreciation parameters in the fixed asset object are changed after the postings have been recorded, you will need to update the postings once again, otherwise the changes will not take effect. The applications BUCH, KONBUCH und ICANLBEW in the action menus can be used to carry out the action "Automatic generation of depreciation". To do this, the posting lines for the fixed asset objects for which the depreciation must be recalculated should be marked in advance.

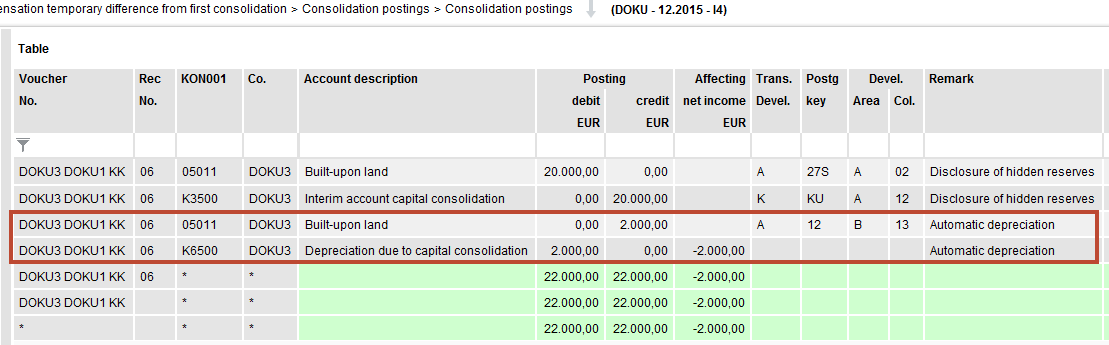

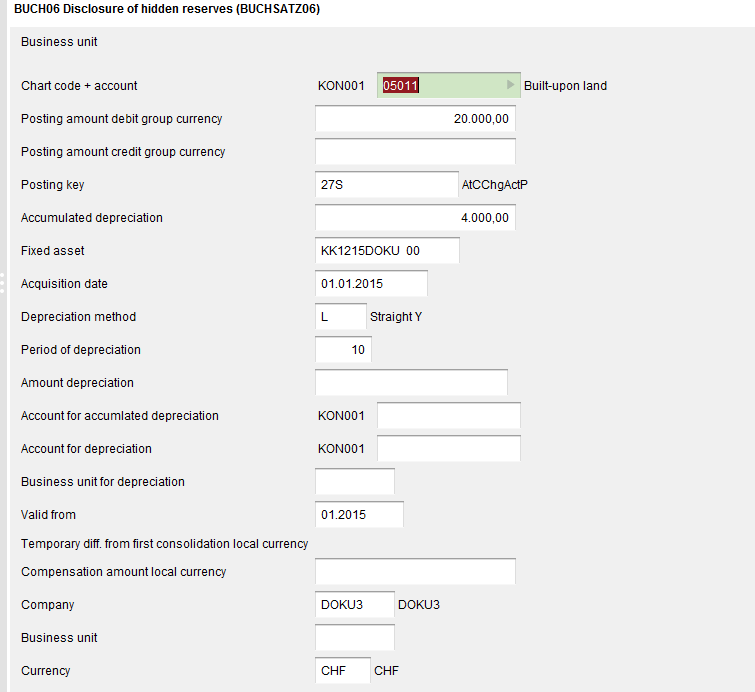

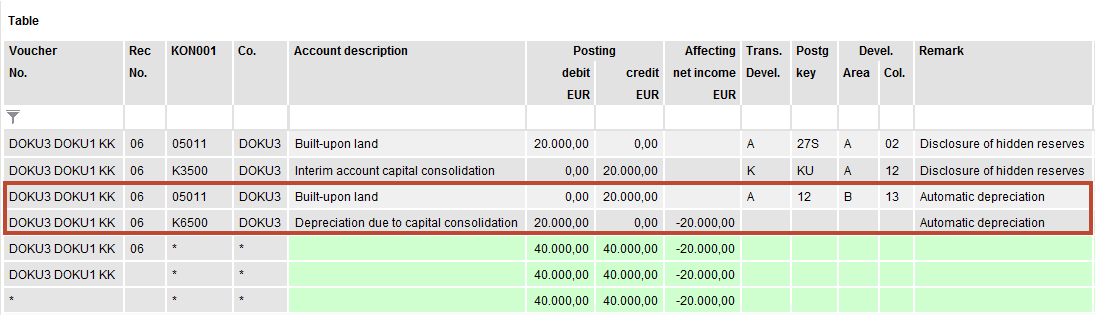

The basis for the examples 1 to 5: In the group -DOKU+, hidden reserves valued at 20,000 euros will be uncovered and activated during initial consolidation of the company -DOKU3+. These are to be written down. The examples are shown based on a consolidation voucher in KONBUCH, nevertheless, the way in which this works and the calculations are the same as with a company financial statement voucher in BUCH.

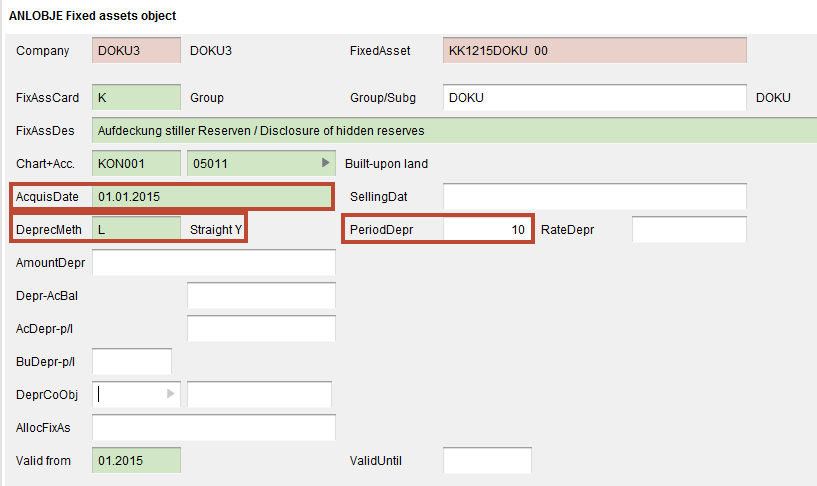

Straight-line depreciation over 10 years from the point of initial consolidation in 01/2022

In this case, 01/01/2022 is entered as the date of acquisition, the depreciation method is = L and the service life is 10 years

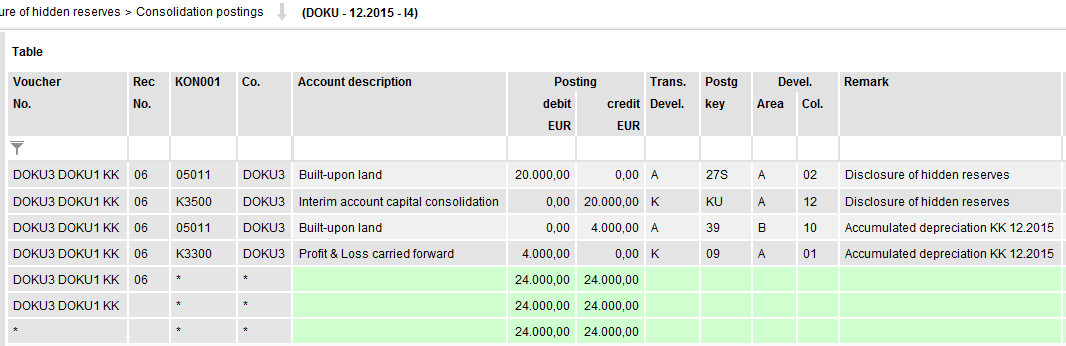

2,000 euros of depreciation are automatically posted to the consolidation voucher.

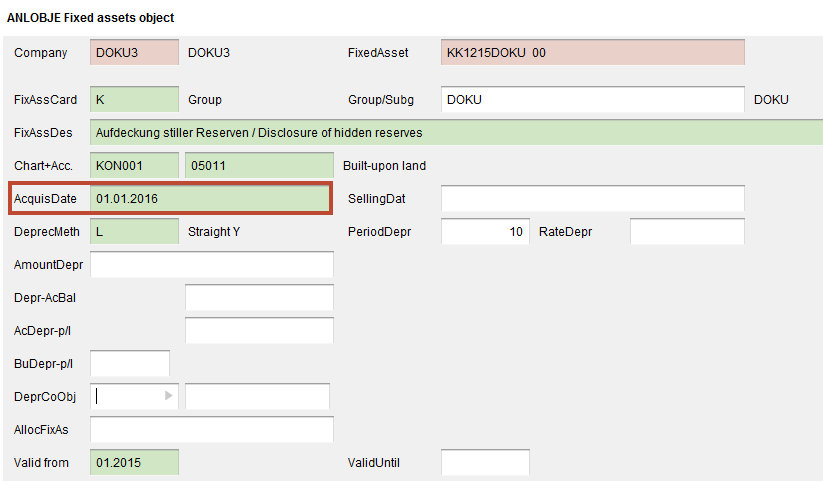

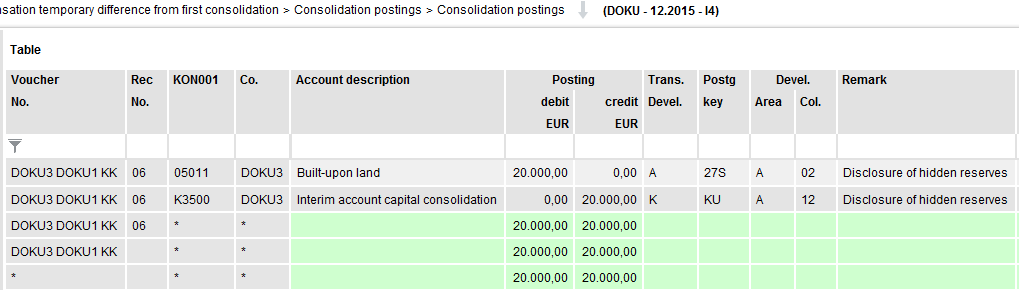

Depreciation is to continue to take place in a linear manner for 10 years, starting in 2023, however:

The fixed asset object only needs to be changed in one position: the date of acquisition should be changed to 01/01/2023.

No depreciation is posted in the consolidation voucher.

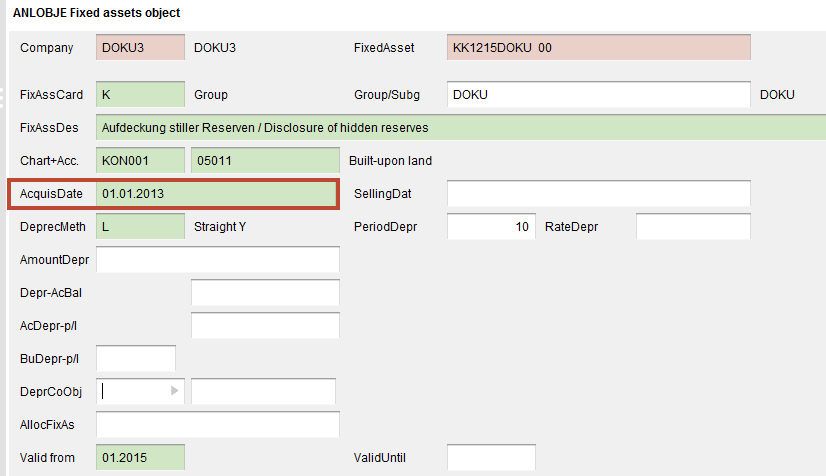

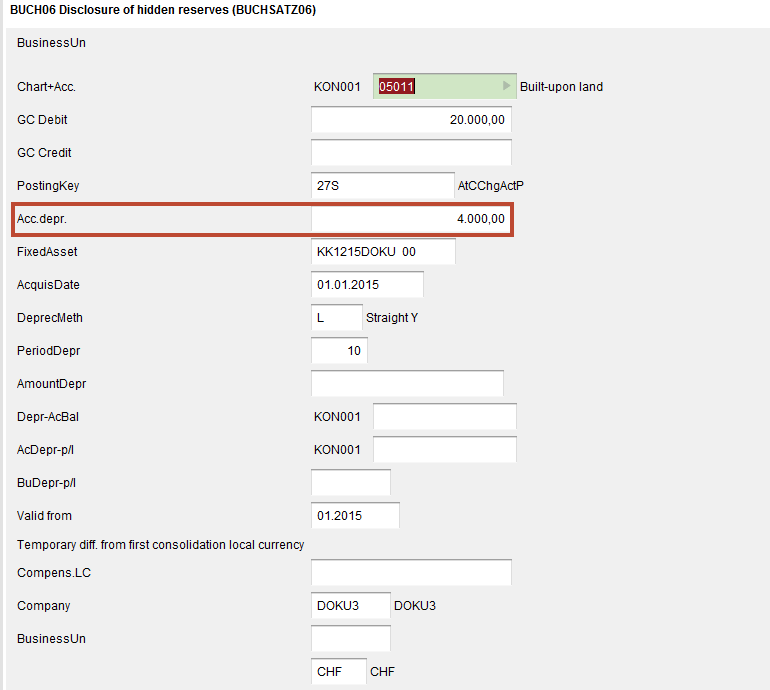

This represents a historic initial consolidation which means the company was added already in 2020, two years ago, nevertheless initial consolidation was performed in 2022 using IDL Konsis. The depreciation method is still linear and the lifetime is 10 years. For this reason, 4,000 euros of cumulative depreciation were already stored when the difference was reconciled.

Here, it is important that you select the correct date of the purchase. If you store the fixed asset object without intervening manually, then 01/01/2022 will be entered as the date. However, in this case, it would be impossible to post any current depreciation, as you can see here:

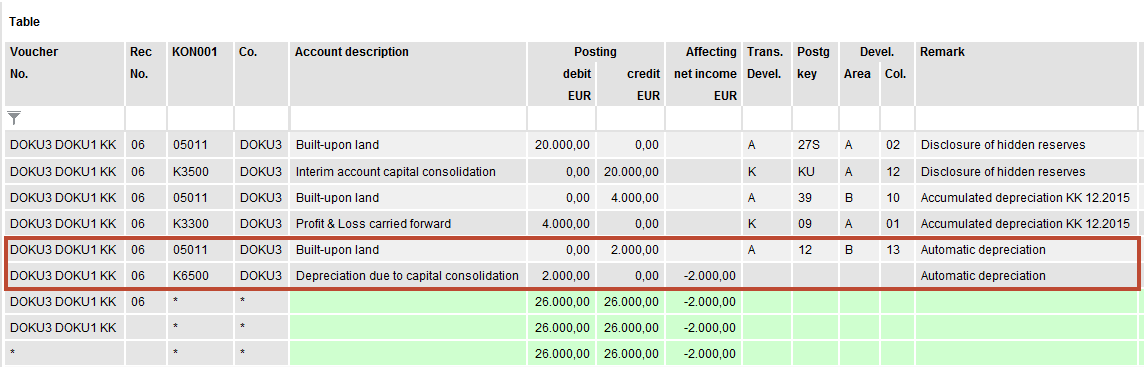

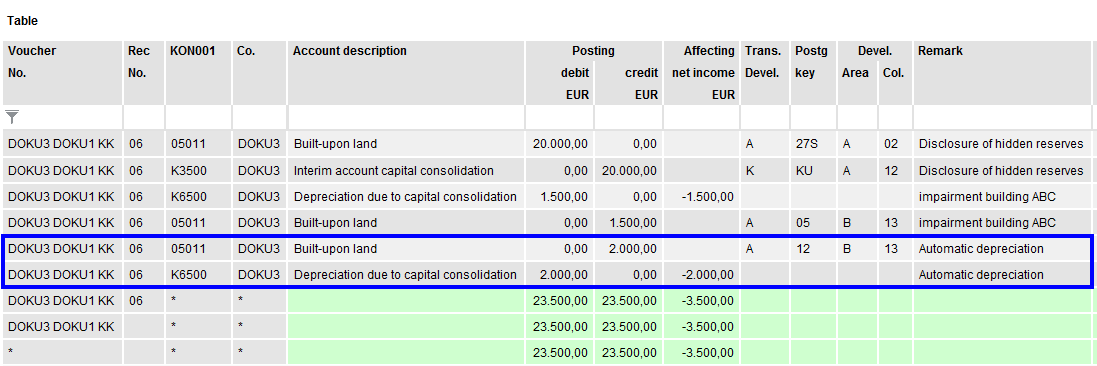

What has happened? With straight-line depreciation, the system calculates how much depreciation should be posted on the basis of the purchasing costs and the date of purchase. This is 2,000 euros with the settings selected in the fixed asset object. In the posting, however, 4,000 euros of cumulative depreciation have already been posted, in other words more than should have been. Now, the automated depreciation would cease to post any more depreciation until the excess amount has been used up.

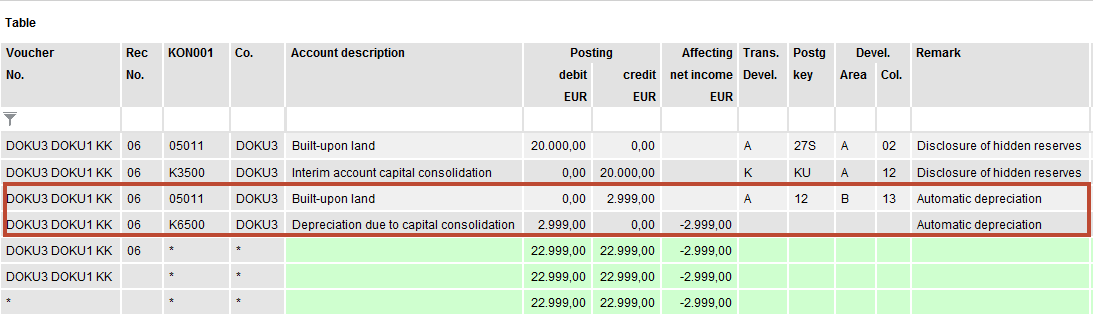

If the date of acquisition is changed to the correct date 01/01/2020, the ongoing depreciation will be calculated correctly:

The possibility of storing cumulative depreciation directly when a fixed asset object is created is only available in the application "allocate difference amount VUB". If cumulative depreciations are to be shown in a posting that has been generated manually, these must be recorded separately using the appropriate posting keys for depreciation carried forward.

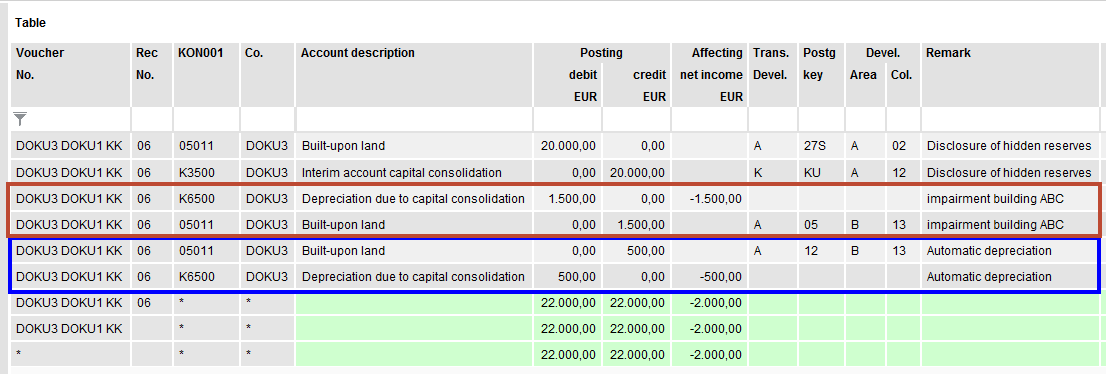

Straight-line depreciation over 10 years from the point of initial consolidation in 01/2022; in addition, special depreciation of 1,500 euros is to be performed in 2022.

With the consolidation postings that have already been generated in example 1, the special depreciation is added manually:

The current straight-line depreciation of 2,000 euros was changed to 500 euros due to the additional posting. In order to be able to come up with the entire annual depreciation of 2,000 euros IN ADDITION to the special depreciation, the depreciation method must be changed from L to SL in the fixed asset object:

If the depreciation postings have been regenerated using the context menu after this change has been made:

The full ongoing depreciation is posted automatically in addition to special depreciation.

The depreciation should amount to 2,999 euros per year. This annual amount is entered as fixed depreciation in the fixed asset object:

If, as in our example, this is a posting in an annual financial statement, then the entire amount will be posted. In interim financial statements, the proportionate amount will be calculated accordingly.

The fixed depreciation amount will only be posted until the value of the asset drops to 0.00. Depreciation does not result in negative asset values. As an example, 25,000 euros of annual depreciation have been entered in our fixed asset object:

In the posting, 20,000 euros have still been posted because, in this case, the full amount of the purchase costs would already be used up.

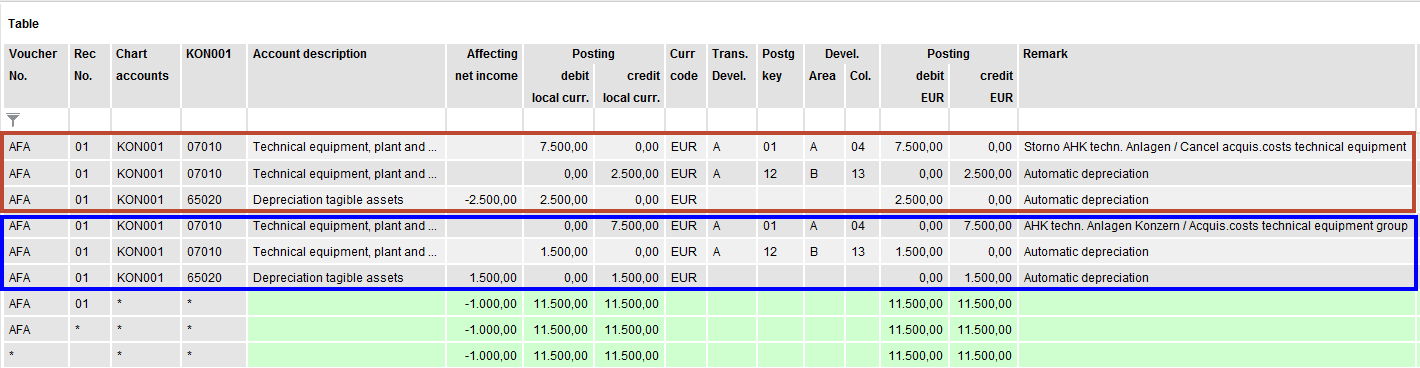

A position in the fixed asset is depreciated in the company financial statement over a period of 3 years. According to the group guidelines, this period should be 5 years. The acquisition costs amount to 7,500 euros and the ongoing depreciation based on the summarized financial statement 2,500 euros

In order to be able to present this information easily with the help of automatic postings in the company financial statement, two new fixed asset objects must be set up: one with a duration of 3 years and one with duration of 5 years:

A posting voucher is created in the application -BEL+. In this voucher, the fixed asset account will be posted twice in the value of the purchase costs of 7,500 euros: as a credit on the fixed asset object with the duration of the company (red edging), as a debit on the fixed asset object with the duration of the groups (blue edging). The depreciation postings are generated automatically for both fixed asset objects. In total, this results is the correction of the depreciation. In the periods that follow, the voucher will be carried forward and the depreciation will be generated automatically with the carry forward.

The amount calculated on the basis of automated depreciation mainly depends on four factors:

You should check these settings carefully if the automated depreciation postings do not result in the amount you were expecting.