The following document aims to present the conditions required to implement a cash flow statement in IDL Konsis. The key data are mostly based on the original standards for cash flow statements (GAS 2, IAS 7) and the corresponding commentaries (e.g., Schäfer-Pöschel IAS Commentary).

The value attached to cash flow statements has grown over the past few years. It is now a standard report used in external reporting even for companies not subject to mandatory publication requirements under HGB accounting. According to IAS, cash flow statements are compulsory for all companies and groups of companies that publish IAS/IFRS financial statements. The corresponding regulations are to be found in IAS 7, which was published in 1994. In 1995, the Main Specialist Committee (Hauptfachausschuss - HFA) of the Institut der Wirtschaftsprüfer (IDW - German Accounting Institute) dealt with this issue in cooperation with the Schmallenbachgesellschaft's (SG) "Financing Calculation" (Finanzierungsrechnung) working group. HFA 1/1995 "Die Kapitalflussrechnung" (The Cash Flow Statement) as a supplement to annual and consolidated financial statements was published. The cash flow statement became a mandatory component for companies geared to capital markets thanks to KonTraG (German Act on Control and Transparency in Business). The German Accounting Standards Committee (Deutsche Rechnungslegungs Standards Committee) presented the draft of GAS 2 "Cash Flow Statement" in 1999, which was announced in May 2000 by the Federal Ministry of Justice (BMJ - Bundesministerium der Justiz). The German accounting standards committee (Deutsche Standardisierungsrat - DSR) based its version heavily on IAS 7. Under TransPuG, the cash flow statement has become a component of the consolidated financial statements. Under BilReG, the cash flow statement has become a mandatory component of the consolidated financial statements for all groups of companies (section 297 of the HGB).

The aim of the cash flow statement is to provide information on cash flows for the past fiscal year for a company or group. It thus focuses on the origin and use of cash and cash equivalents.

This information is used to derive a company's ability to generate cash and cash equivalents in future. In addition, it aims to estimate future requirements for liquidity.

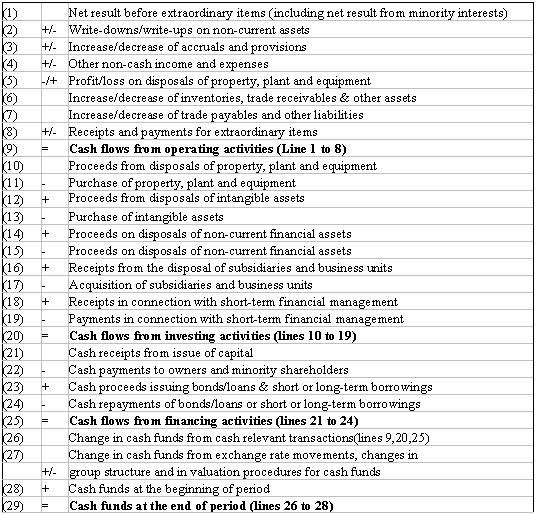

The changes in cash and cash equivalents are presented in three sections, broken down into cash flows from "operating activities", "investing activities" and "financing activities". As a result, GAS 2 includes a minimum classification structure, which is detailed below. As a rule, cash flows can be directly and indirectly derived. To derive these directly, it would be necessary to have access to actual original payments received and made. However, this information is not generally directly available in accounting systems, as a strict split between cash and non-cash transactions is often not included. This is why in practice almost 100% of cash flow statements are prepared to using the so-called indirect method. Here, the net income for the period forms a starting point when identifying the changes in cash and cash equivalents in the current period. Structure of the cash flow statement using the in direct method of presentation (GAS 2):

Figure: Structure all the cash flow statement using the indirect method of presentation

All of the following examples assume that the fiscal year is the calendar year.

Section A of the documentation describes setting up the cash flow statement in IDL Konsis.

Section B of the documentation describes how changes in the group of consolidated companies can be shown in IDL Konsis Release 2006.0, and which manual corrections still have to be made by the user.

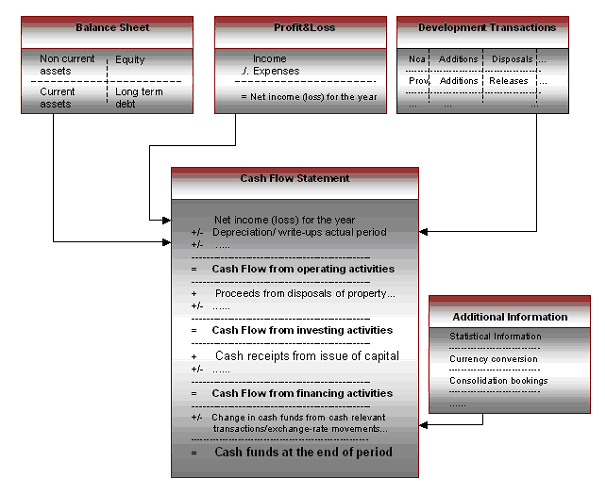

data from various sources of information are put together in a report to show the cash flow statement in IDL Konsis.

Figure: Sources of information for cash flow report

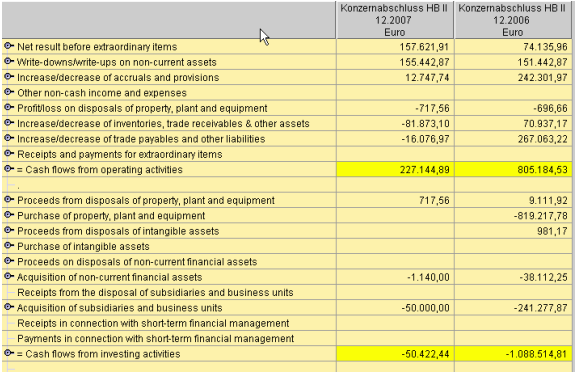

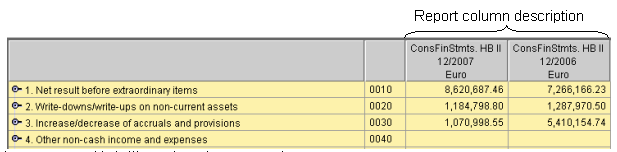

Figure: Sample extract from a cash flow report in IDL Konsis:

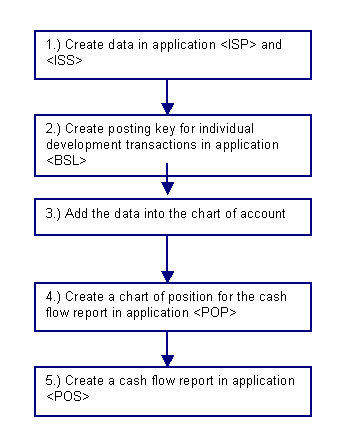

before a cash flow report can be created in IDL Konsis, the user must execute the steps described below:

Figure: 5 steps for setting up a CFR

The following to commission described setting up three different individual statements:

The differences in use and the respective functional areas of application are discussed below.

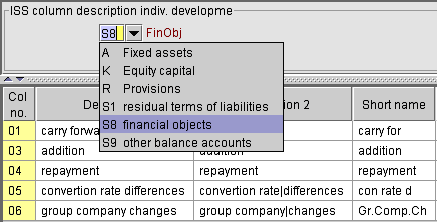

An individual statement is initially setup with the user deciding which of the nine individual statements (internally referred to as S1 to S9) that are available in IDL Konsis should be used (see above).

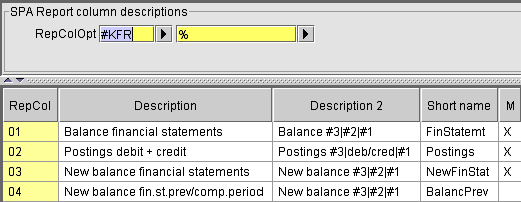

After defining which "statement numbers" should be used, user-defined text is allocated to these statements. Each individual statement in IDL Konsis has 50 usable statement columns. Which statement columns and how many statement columns are used is also controlled using user-defined text.

An "automated individual statement" has to be set up for a cash flow report. This statement automatically generates the statement transaction data that is needed for the cash flow statement for all of the balance sheet accounts to which no standard statement has been allocated (statement of changes in fixed assets, capital or provisions) .

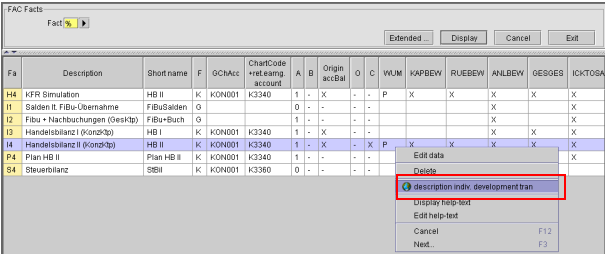

The application "text for individual statements" (ISP) is used to maintain the user-defined text that can be reached using a shortcut or via the menu tree or as a subsequent application from the "data types? overview. This overview shows the texts already input for individual statements. Here, the type of data used to input the text is of no importance. Fact I4 was selected in the following example.

Figure: Sample action 'Setting up texts for individual statements'

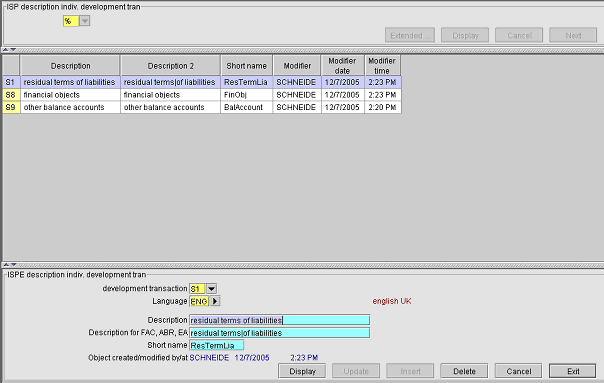

The associated individual record application "Texts for individual statements" (ISPE) can be used to record, change or even delete these texts. It is possible to input these in various languages. The key to be used to is the one previously used for individual statements (?S1? to ?S0?).

Figure: ISPE menu, texts for individual statements

The texts are broken down into short text and long text for prompt texts and presentation in selection lists as well as the "name for ABR, FAC, EA, etc" which is used as a table header. By using the "|" sign in the text you can control a multi-line table with this name field.

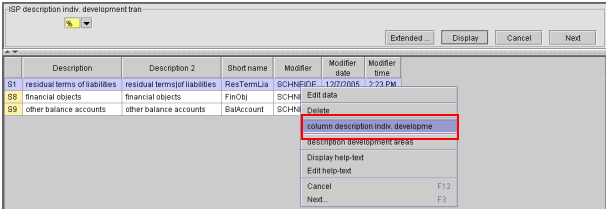

For each individual statement thus defined, branch off from ISP to the subsequent application "texts for individual statement columns" (ISS), in order to also define the possible statement columns there as well (report result values), and to add speaking texts. These texts are required to input the booking keys and to define the report column options. Without this definition of the statement headers, you will not be shown any values in the corresponding selection lists (applications BSL and FED).

Figure: Action 'Setting up texts for individual statement columns?

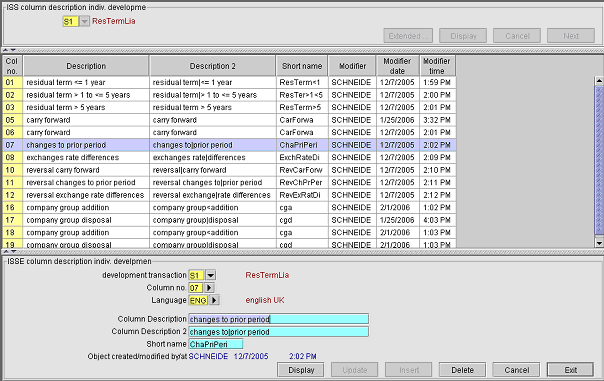

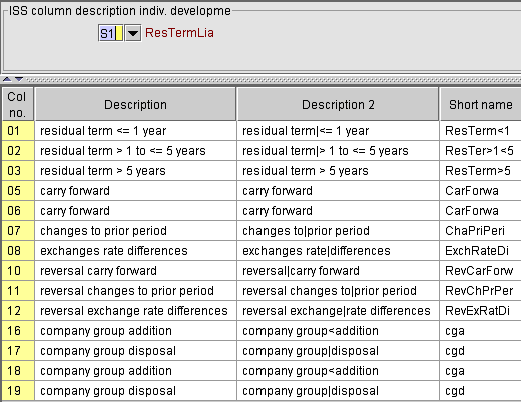

The associated individual record application "Tests for individual statement columns" includes the column number as a further key in addition to the key for the statement and the language. The column number is between '01' to '50'. Here too, a long text (up to 35 characters) and a short text (up to 10 characters) and a text for column headings (multi-line if the ?|? character is used) must be stated.

Figure: ISSE, texts for an individual statement column

In all IDL Konsis applications now only the user-defined texts are shown.

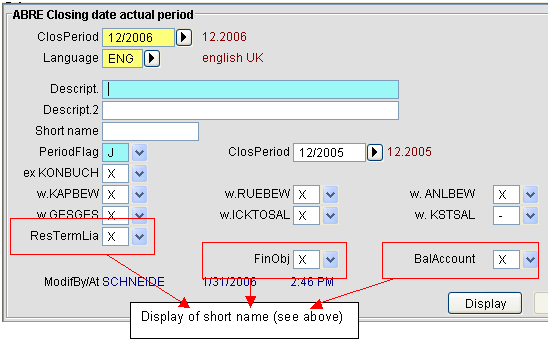

Example: "ABR" application

Figure: ABRE

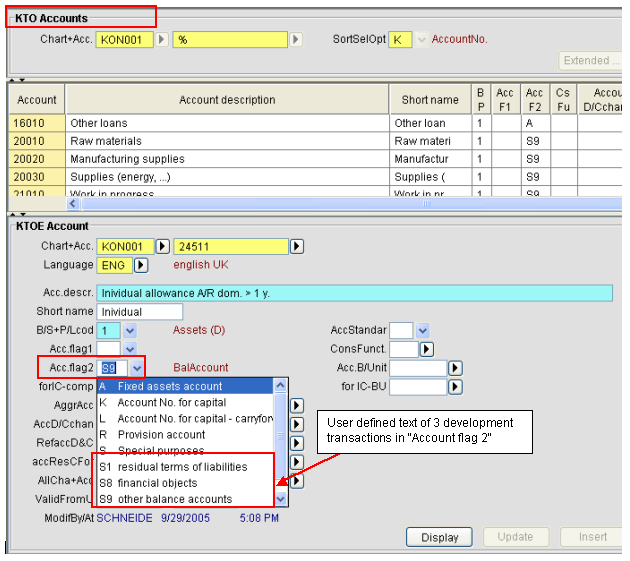

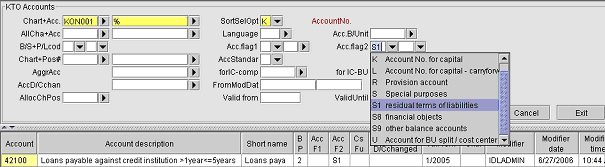

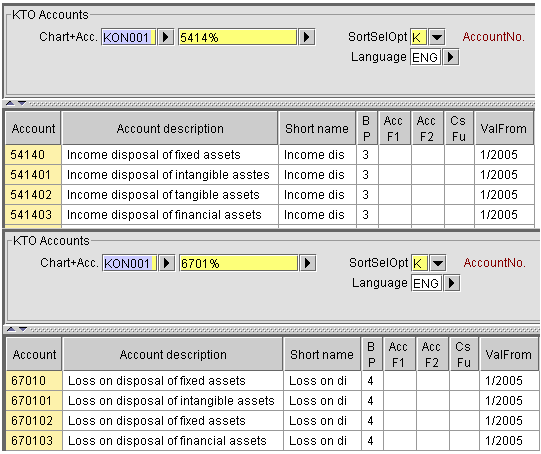

Example: "KTO" application for the group chart of accounts

Figure: KTOE

Note:The display is identical when a company chart of accounts is shown.

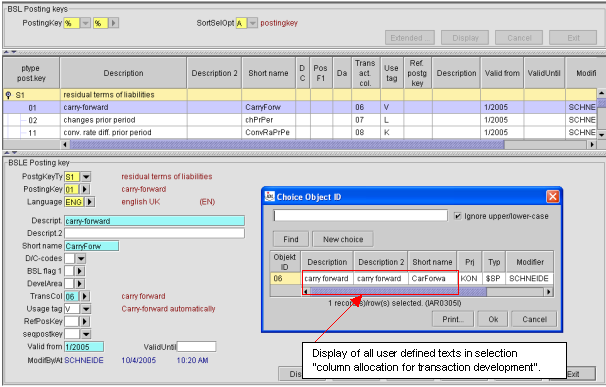

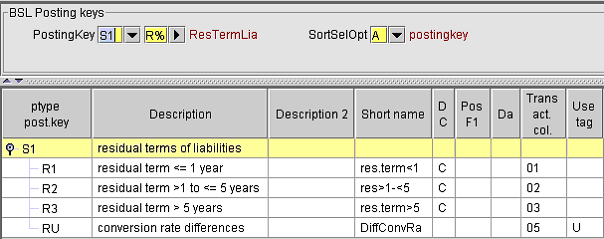

Example: "BSL" application

Figure: BSLE

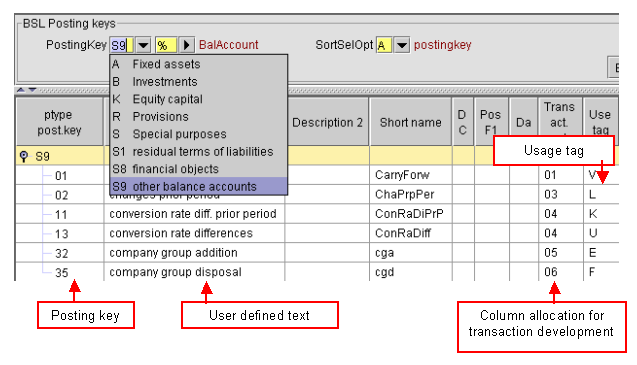

The user must set up booking keys in the "BSL" application with the following use codes for an "automated individual statement":

Figure: Example booking key "Automated individual statement"

The change in the account balance to the prior period is generated in local currency and added to the individual statement for the booking key with use code "L" (ongoing changes individual statement) via the test module in IDL Konsis. This means that for the purpose of the cash flow statement the ongoing changes and the carryforward from the previous year are available separately for the respective account. This allows a clear differentiation to be made for these accounts between exchange rate effects from the carryforward and exchange rate effects for ongoing changes in the current period.

The statement transactions for this account group are generated automatically. The period carryforward at company level generates a carryforward in local currency. This is also the case when the statement is used for the first time. Of course, this means that prior period data (account balances) must be available.

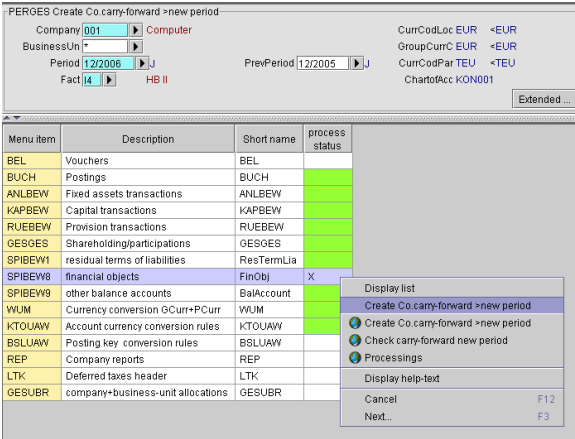

Figure: Example: PERGES initiating carry forward per individual transaction development separately

The ongoing changes are automatically and constantly generated via the test module for account balances. This ensures that the changes are always up to date, both during imports as well as during online input.

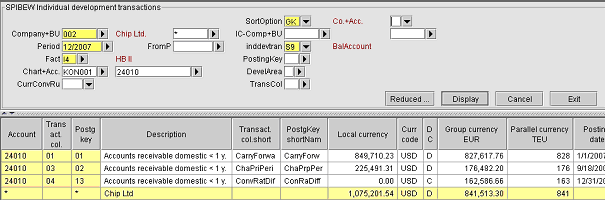

Example: Automatically generated transaction data (selection in the "SPIBEW" application, account=24010), disclosure carryforward, ongoing changes and exchange rates effects on the carryforward.

Figure: Example: Automatically generated transaction data (selection in the "SPIBEW" application, account=24010), disclosure carryforward, ongoing changes and exchange rates effects on the carryforward.

Note:

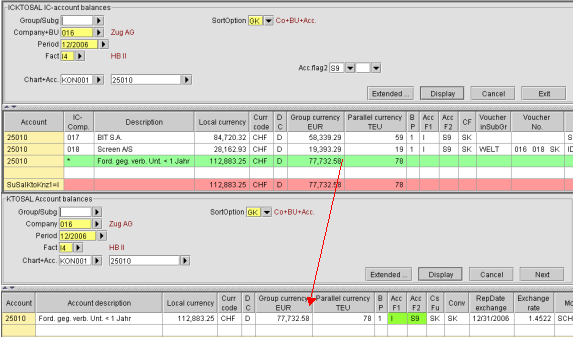

As of release 2006.0 IC transactions data are also generated for "IC balances". For the individual development transaction S9 these are formed based on the "IC balances" in the context of the carry forward. The regular changes are kept current ongoingly according to this logic based on the "IC-blances" per "IC-company".

Figure:IC-balances and account balances

This statement is not mandatory for the correct presentation of the cash flow statement.

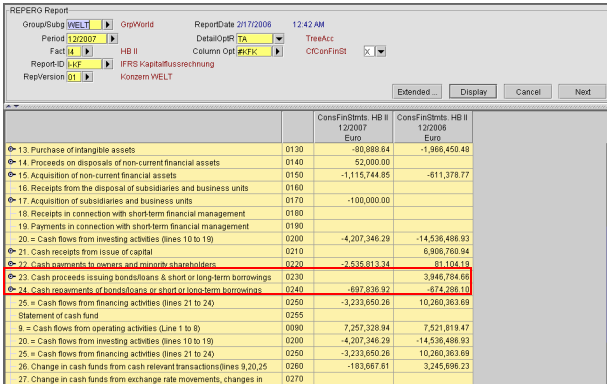

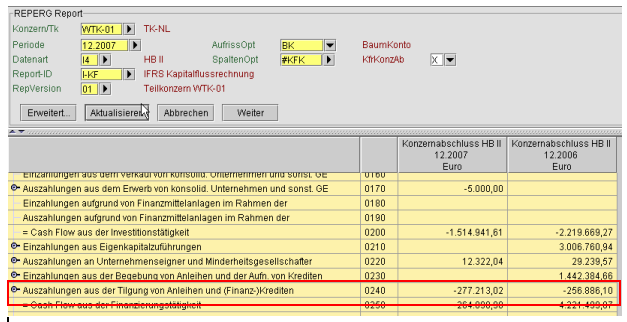

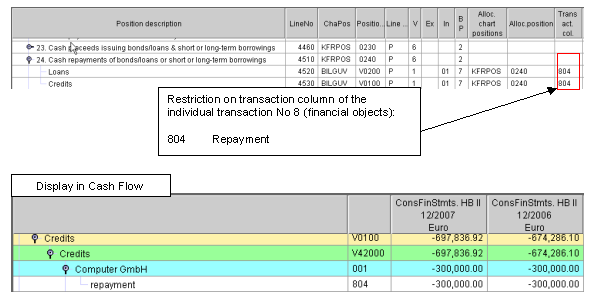

Within the cash flow statement, taking out and repaying long-term liabilities most be disclosed separately (see cash flow statement structure)

Figure: Display of payments received and made in the CFS

However, as this information is often netted within the accounts, in these cases users must set up an additional individual statement.

However, if the assumption and repayment of long-term liabilities are kept in separate accounts, this information may also be directly evaluated via the transaction data for the corresponding accounts in the cash flow structure.

The following comments assume that this data is not separately available.

In this individual statement, the ongoing changes (repayments, additions of loans) is input manually, as is the case for the standard statements. As a result, no booking key with the use code = "L" is to be input for this statement.

Another reason for setting up this individual statement is that, as a rule, a statement of maturities is kept for liabilities accounts, and that the corresponding account code 2 for the <KTO> application is thus used for another purpose.

Figure: Show allocation KTO 42100 to statement S1 (acc. code.2=S1)

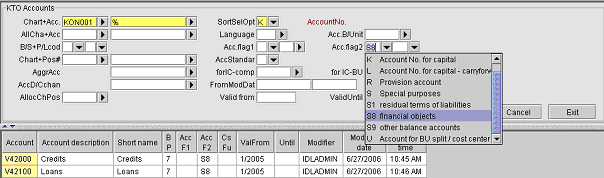

In order to be able to evaluate the necessary transaction data within the cash flow statement, it we recommend that you record the transaction outlines using statistical accounts. These accounts can then be allocated to separate items, which can then be evaluated within the cash flow report.

Figure: Show allocation statistical accounts to statement S8

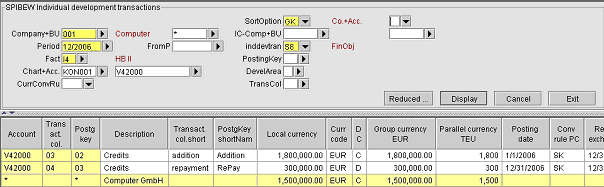

Figure: Example: Transaction outline for statistical accounts

The comments made above apply to setting up user-defined text for this statement type and to setting up user-defined text for statement columns.

Figure: Example for a user-defined statement "Financial Assets":

A particular characteristic of this type of statement is that ongoing changes or the addition of new long-term funds have to be recorded manually. IDL Konsis only generates the corresponding carryforward transactions as part of the "PERGES" application.

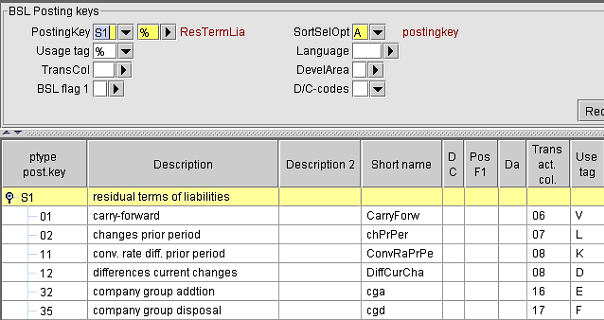

Booking keys are required for the items that have to be recorded manually for this type of statement. These booking keys are set up without any use code:

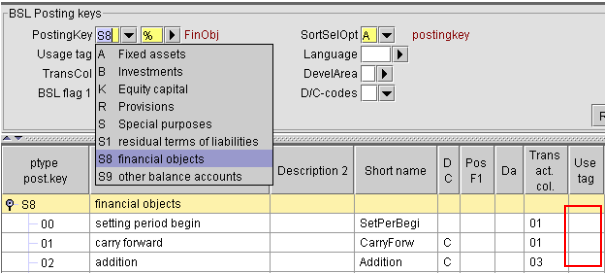

Figure: BSL of the BSL group S8 without use code for manual items

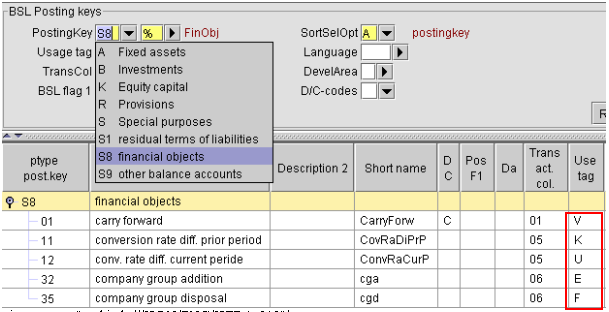

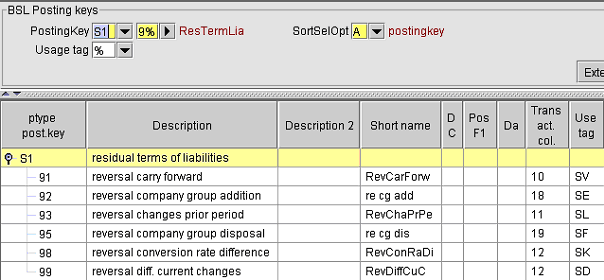

When calculating the respective exchange rate effects on the carryforward and the exchange rate translation effects of the ongoing change to the previous year, in addition to the carryforward account, the booking key itself must also be defined using the use codes "V", "K", "U", "E" and "F".

Figure: BSL of the BSL group S8 with use code for manual items

This allows a clear differentiation to also be made for these accounts between exchange rate effects from the carryforward and exchange rate effects for ongoing changes in the current period.

The ongoing changes have to be input manually.

This statement is not mandatory for the correct presentation of the cash flow statement. However, if this statement has been set up in IDL Konsis, the supplements and special features described below must be observed.

The comments made above apply to setting up user-defined text for the "statement of changes in liabilities" and to setting up user-defined text for statement columns.

Example of a user-defined statement of changes in liabilities:

Figure: user-defined statement of changes in liabilities

A particular characteristic of this type of statement is that no carryforward data can be generated for the remaining term. The booking key for the remaining terms are defined without a use code.

However, for statements with no carryforwards, changes between the current and previous period must also be identified. In addition, here too exchange rate effects must also be calculated in order to be able to differentiate between exchange rate effects on the carryforward and exchange rate effects from ongoing changes.

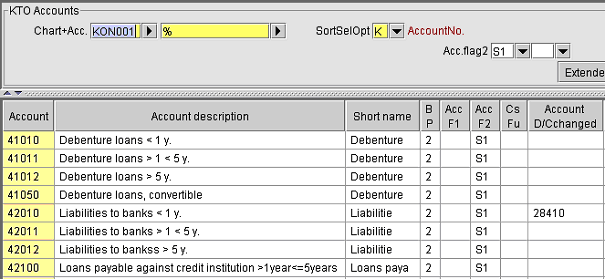

The account is set up as a statement account for remaining maturities using the account code 2 in the application <KTO>. This means that no further individual statements can be allocated to these accounts for the statement of changes within the meaning of the cash flow statement.

Figure: Allocation of accounts to AccCode2=S1

Booking key for a statement of changes in liabilities:

Figure: BSL group S1 with various BSLs

The change and the respective exchange rate effects have to be calculated in an incidental calculation for these accounts. The results of this incidental calculation are filed in line with the booking key described further above. Booking keys with the usage codes "V", "L", "D", "K", "E" and "F" must also be defined for statements without the formation of carryforwards. In contrast to statements with the formation of carryforwards, in the case of individual statements without the formation of carryforwards the usage code "D" must be used instead of a booking key with the usage code "U", as the usage code "U" is already used for the translation effects based on the remaining maturities.

Figure: BSL with various usage codes

As the test module in IDL Konsis tests the outline statement data against the respective account balance, corresponding cancellation booking keys with the usage codes "SV", "SL", "SD", "SK", "SE", and "SF" have to be set up in order to fulfill the plausibilities between the final balance, detailed presentation in the statement and account balance for the six booking keys "V", "L", "K", "U", "E", and "F". The values of these have a counter effect on the amounts calculated in the statement of changes.

This allows a clear differentiation to also be made for these accounts between exchange rate effects from the carryforward and exchange rate effects for ongoing changes in the current period.

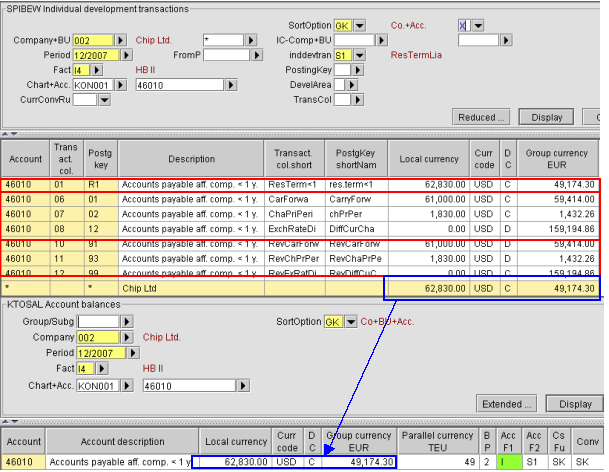

The statement transactions for this account group are generated automatically. The period carryforward at company level generates a carryforward in local currency. This is also the case when the statement is used for the first time. Of course, this means that prior period data (account balances) must be available.

Example: automatically generated transaction data (Selection in the application <SPIBEW> in account =46010)

Figure: Automatically generated transaction data

The cancellation booking key ensures that the total transaction outline corresponds to the account balance.

In order for it to be possible to generate the corresponding transaction data for the individual statements, users have to input an individual statement type into the balance sheet accounts to which no account code 2 has been allocated in the <KTO> application, in line with the determining statement application.

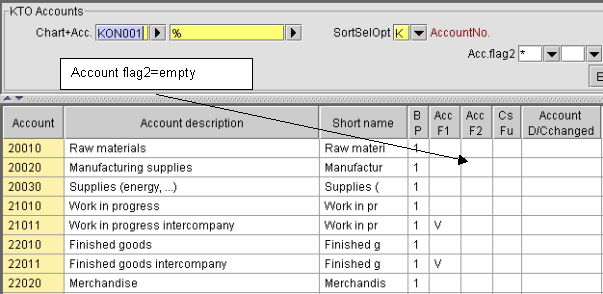

In the following examples, all accounts on the assets side which are not asset accounts are allocated the statement type S9 (automated statement).

Figure: Asset-side accounts without allocation in AccCode2

This can be performed by selecting the corresponding accounts and the function change quantities in a single step. Below, all balance sheet accounts (BilP+L-code=1) with the account code2=empty (Account-code2=*) are selected.

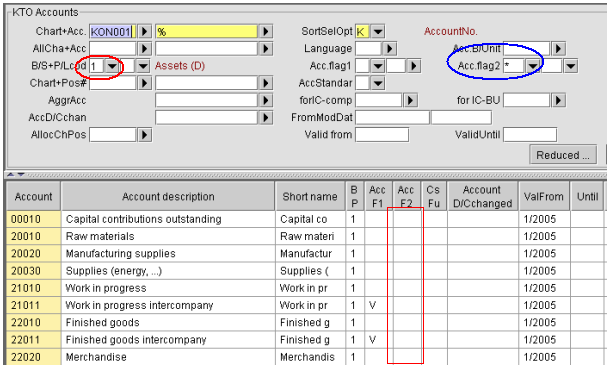

Figure: Selection of asset-side accounts without allocation in AccCode2

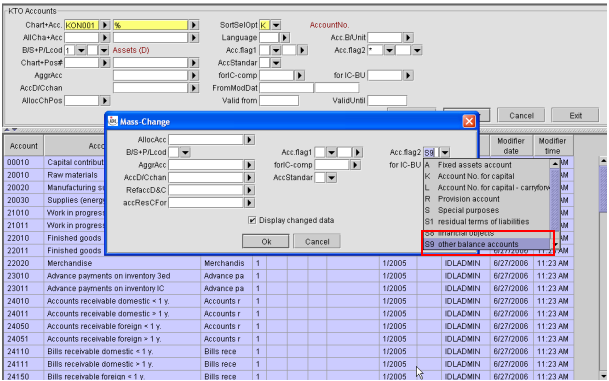

Mark records and, for example, allocate these to the individual statement S9 using the function change quantities from the action menu. The consolidated chart of accounts must be entered in this step.

Figure: Allocation AccCode2=S9 using quantities

IDL Konsis also automatically inputs the AccCode2 into the allocated company charts of accounts for the corresponding accounts.

Figure: Report panel for automatically jointly input company charts of accounts

It is not mandatory to set up a separate chart of accounts for the cash flow statement. The accounts for the cash flow statement classification can also be input into an existing chart of accounts, which, for example, includes the balance sheet and profit and loss statement classification. In order to improve the overview, it is, however, recommended to store the accounts for the cash flow statement in a separate chart of accounts. This is assumed in the sections below.

In addition, we would like to point out again that no accounts have to be allocated to the account line plan. Accounts from an existing balance sheet chart of accounts are allocated to the account lines in the cash flow classification. Any exceptions to this principle are discussed further below.

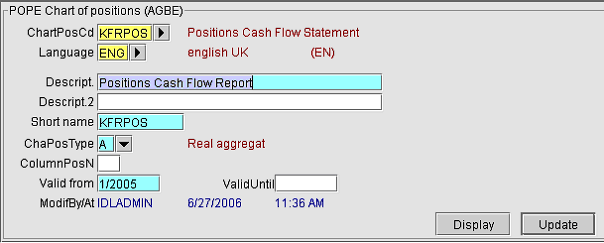

Prior to setting up the account lines for the cash flow statement, users must first define a chart of accounts. The name of the chart of accounts is stored in the chart of accounts application <POP>. In the following example, the chart of accounts for the cash flow statement is called: <KFRPOS>

Figure: Log sample chart of accounts

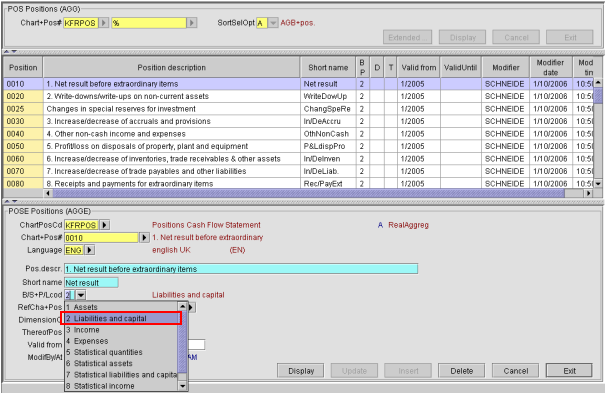

The accounts for the chart of accounts <KFRPOS> are logged in the application <POS>.

Figure: Log accounts for chart of accounts

The items logged here are not allocated to any accounts. The items are only used to describe the report to portray the cash flow statement. Figures for the cash flow statement are allocated or generated within the report line description. Setting up the report line description is described further below.

All of the items of the cash flow classification are set up as liabilities accounts. This ensures that net cash used (NCU-) and net cash obtained (NCO+) are shown with the correct signs.

Net cash used is shown in the cash flow statement with a minus sign, and net cash obtained is shown with a plus sign.

Figure: Example of net cash used Investments in property, plant and equipment

Figure: Example of net cash used Repayment of loans

Figure: Example of net cash obtainedRaising noncurrent loans

Figure: Example of net cash obtained Increase in other equity and liabilities

Figure: Example of net cash obtainedNet income for the period

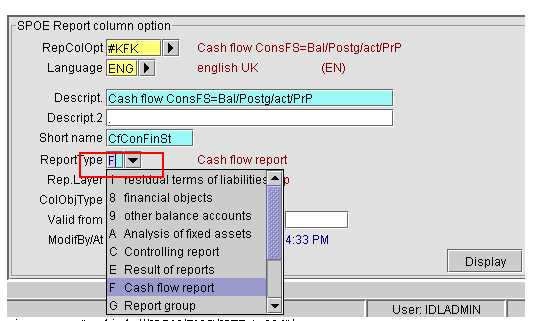

A new report type for cash flow statements has been defined in IDL Konsis. In addition, the standard scope of delivery includes so-called column options with the associated column structure and column names.

Figure: Sample report column option <SPO> with report type "F" provided as standard

Delivery also includes the columns deposited with reference to the column option described above. This means that the column structure and the column headers are defined.

Figure: Example of column options supplied #KFR

Figure: Example of report view of the column options #KFR

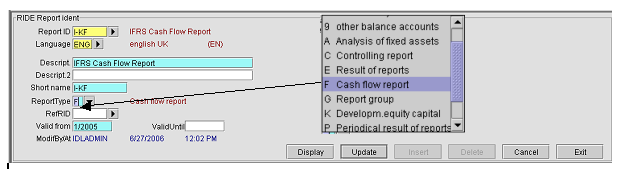

Users must define a report name in the application <Report Ident>. This report is to be allocated the report type "F" = cash flow report:

Figure: RIDE allocation of report type

A report structure must then be defined for the report ID that has been set up in the application Report Line Description <REPZEI>.

In so doing, report add-ons specially developed for describing the cash flow statement can be used.

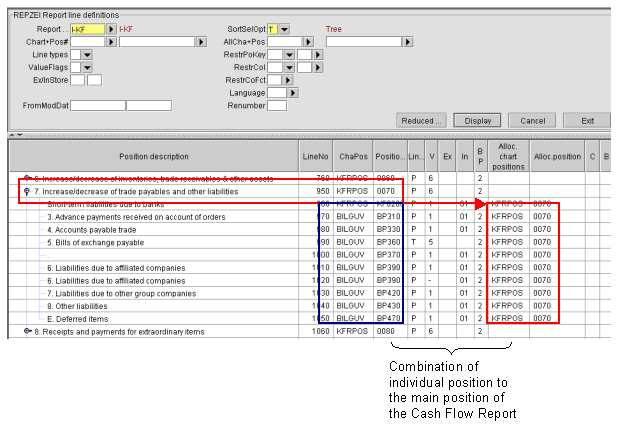

For example, it is possible to allocate accounts to accounts. Until now, specific values could only be controlled in reporting using account/account allocations. The connection between account and account is controlled using the allocated chart of accounts and allocated account field in REPZEI. In the report view in reporting, there is a consistent top-down approach, and as a result only the key account is initially shown as the top node point with the associated value. The allocated accounts can be viewed by opening the respective node.

Figure: "top-down-approach" in the report view

The cash flow statement is generated based on an already existing chart of accounts with the associated allocations account/account. Users do not have to allocate all of the accounts again to the cash flow statement chart of accounts. Data for the cash flow statement is evaluated in the report line description by linking the individual items with the main item for the cash flow statement.

Figure: Linking the individual items with the main item

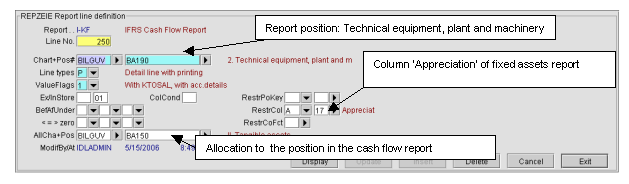

In addition to values from the table of account balances, information from the statements or the consolidation bookings can also be included. To describe these issues, we have included condition controls for restrictions to specific

Figure: REPZEIE and the meaning of the settings

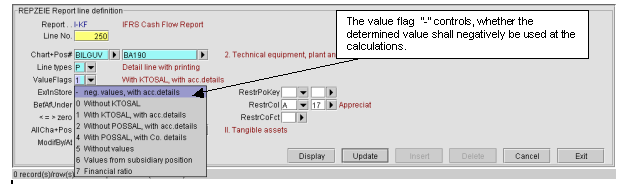

Figure: REPZEIE negative calculation

IDL Konsis deliver as of release 2006.0 default in the list ...\idl/batch/Autom_CF-Report/ the following files:

The index includes files with definitions for an automatic development transaction, as it is necessary for accounts without development transactions in a cash-flow report. The key 'S9' is used for individual development transaction. please check before import of data that the individual development transaction 'S9' is not used already for other purposes.

The definitions can be taken into the database with the help of the IMPORT-application.

You copy the two files KPDISXXX.TXT and KPBSLXXX.TXT into the list...\idl/batch/Automa_CF-report on your local computer . You then call in IDL Konsis the application "IMPORT" by choice from the menu tree or short word petition, open there the branch "import master data" by mouse click on the '+' symbol, mark the lines for "transaction definitions" and "posting keys" and start per right mouse click the action "insert import-file". If you have capitalized per option the file dialog, you must confirm only the suggested files if you have copied the files into the list given there.

The definitions imported with that can be seen and when required also modified about the applications "description for individual transaction development" (ISP), "column description for individual development transaction" (ISS) and "posting keys" (BSL). The use characteristics may not be changed in BSL since otherwise the automatic construction of the development transaction data is endangered.

For the capitalization of the automatic development transaction construction you still must set now in in the applications "data types" (FAC) and "periods" (ABR) the flag for the "cash flow report" on 'X' for the periods and data types in which you need this development transactions. For initialization of the carry forwards in the first period you have to carry out the 'create carry forward new period' for this period in application 'PERGES' (i.e. if necessary also repeat). As of release 2006.0 the initiation of carryforwards can be initiated in the <PERGES> application per individual development transaction separately. The regular changes are then updated respectively automatically.

The techniques shown above to generate a cash flow report in IDL Konsis are used at a company or group level in various manners. In the sections below, it has been assumed that the cash flow statement is created using the final fact.

IDL Konsis generates the cash flow statement at a company level based on the company statement transactions (statement of changes in assets, capital, provisions and individual statements) and based on the accounts in the current balance sheet chart of accounts.

At a group level, IDL Konsis evaluates the consolidation bookings recorded at a group/sub-group level as well as the transaction data at a company level.

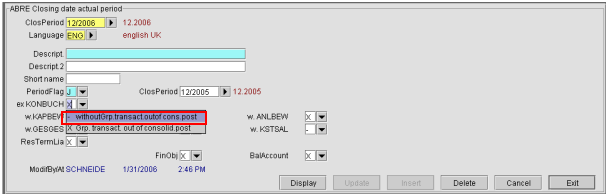

It must be noted that IDL Konsis does not evaluate any group transactions at a group level. The exKonBuch button in the <ABR> application is not evaluated. This means that users must ensure that booking keys are recorded for all booking slips with balance sheet accounts.

Figure: ABRE, ?ex-KonBuch? button

This setting means that when booking slips are recorded, the test module in IDL Konsis tests whether a booking key has been recorded and if this booking key is valid for this account in line with accountcode2.

Figure: Example of wrong booking key

Figure: Example of missing booking key

In the case of individual statements which have a booking key with the use code = "L", IDL Konsis automatically enters the booking key with the use code = "L" if no booking key is recorded during booking. This approach ensures that no slips have to be entered after the fact.

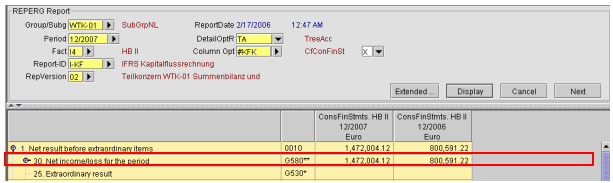

The starting point of cash flow statements prepared using the indirect method is the earnings for the period of the individual company or the consolidated net income. These figures are to be adjusted for extraordinary items.

The new function "Net earnings group" (action menu in KTKGES) gives access to annual earnings after consolidation bookings in the capital transactions. This allows IDL Konsis "E" account to be selected directly as the starting point for the consolidate cash flow statement.

If the earnings for the period are selected before extraordinary items or before taxes as the starting point for the cash flow statement, the selected annual earnings are to be adjusted by corrections for the respective items.

Figure: Portrayal of the annual earnings with the cash flow statement

Here, the basis is formed by the amortization/depreciation according to the income statement or statement of changes in fixed assets. In addition, the write-ups from the income statement or statement of changes in fixed assets are to be taken into account.

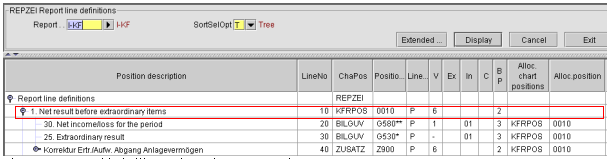

The section below describes selection of the write-ups and write-downs from the statement of changes in fixed assets. The statement columns write-ups and write-downs are stored in the report line description for the relevant items of the fixed assets in each case:

Figure: Description of the selection of the write-ups and write-downs from the statement of changes in fixed assets.

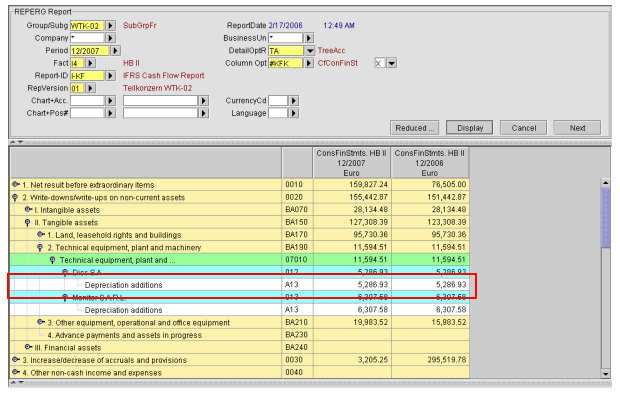

In this area of the report, this allows verification to be maintained in the cash flow statement through to the statement column.

Figure: Verification of write-ups and write-downs from the statement of changes in fixed assets in the cash flow statement

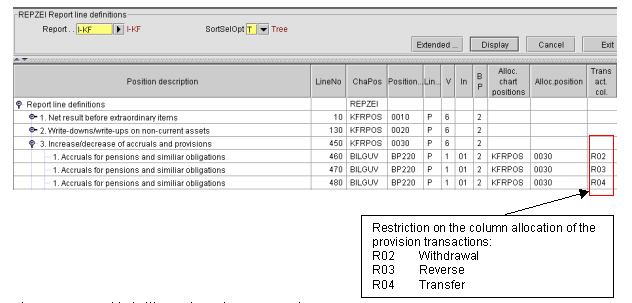

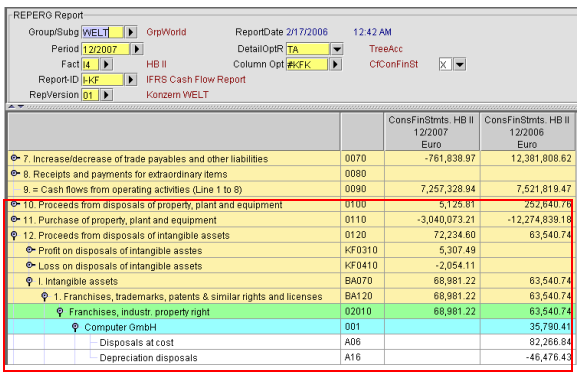

Comparing provisions from the current period with the prior period allows the change in provisions to be identified indirectly. Using information that is prepared via the statement of changes in provisions itself offers a further opportunity. If the chart of accounts has a suitable classification, the size of the changes can be read directly from the account balances.

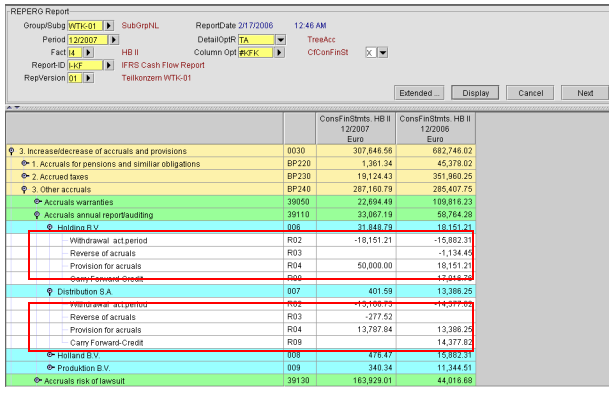

Example 1:Change in provisions is identified from the statement columns: take-up, reversal and additions

Figure: Restriction to statement columns from the statement of changes in provisions

Figure: Presentation in cash flow report

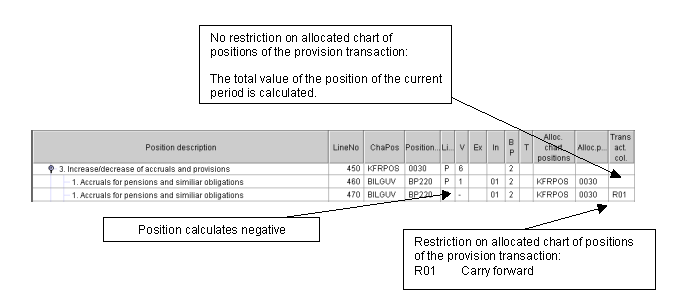

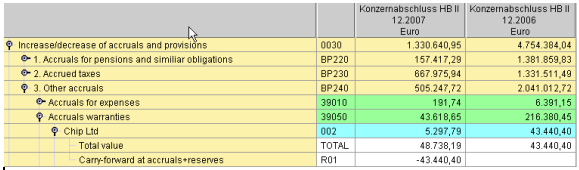

Figure: No restriction to statement columns from the statement of changes in provisions:

Figure: Presentation in cash flow report

Entries from additions to deferred tax assets are to be deducted, as are reversals of deferred tax provisions recognized in income.

Reversals of deferred tax assets are to be added, as are additions to provisions for deferred taxation.

NOTE: We recommend presentation in example 1

Information on other non-cash income and expense can often only be gained via additional information. This must be provided on an account basis. These can be "real" or statistical accounts.

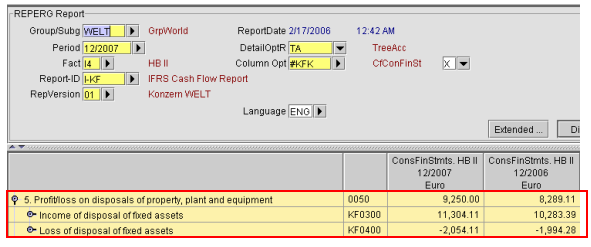

The gains/losses are to be kept in separate accounts, i.e., a separate account should be set up for the profits and also for the losses from the disposal of noncurrent assets per item of the noncurrent assets. These are the also available, with differentiation, for instance, to indirectly calculate the payments received from the sale of assets under "cash flow from investing activities".

Figure: Sample application <KTO>

These accounts can then be allocated to special accounts in order to portray the necessary information in the cash flow report. It is possible to deviate from the principle that no accounts are to be allocated to a cash flow line system for an existing chart of accounts if issues are to be portrayed within the cash flow report for which there is no account balance information or if the existing chart of accounts does not serve the account which is to be shown in the cash flow report.

Figure: Sample allocation of the accounts detailed above to an existing balance sheet chart of accounts

Figure: Allocation of these accounts to a separate line within the cash flow structure

Figure: Portrayal of the separate cash flow accounts within the cash flow report

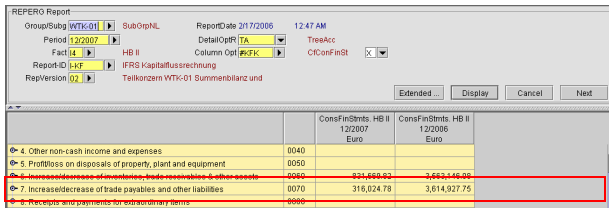

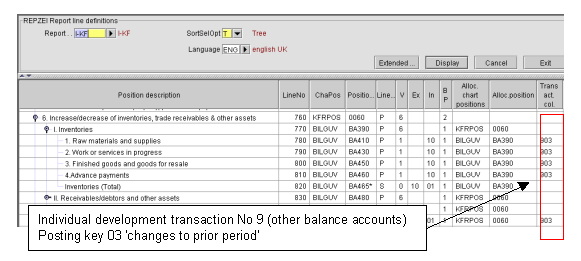

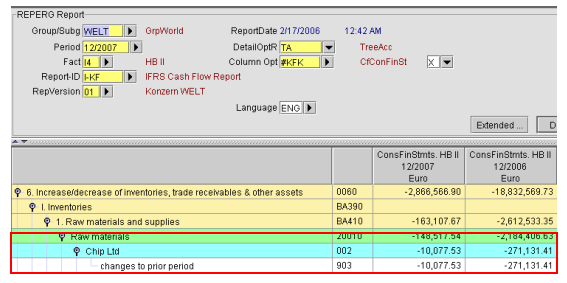

In terms of content, this item includes inventories, trade receivables, other assets, marketable securities and deferred tax assets. Values are identified by comparing current values with those of the prior period, and the total difference is to be broken down into transaction-related and exchange rate-related changes.

If we transfer these items to the German balance sheet structure as set out in section 266 (2) B of the Handelsgesetzbuch (HGB - German Commercial Code), these are changes to the following asset items:

To the extent that these figures are not included in the statement, IDL Konsis automatically generates the relevant transaction data in an incidental calculation.

Figure: Storing the respective asset items in the report line description:

Figure: Presentation in cash flow report

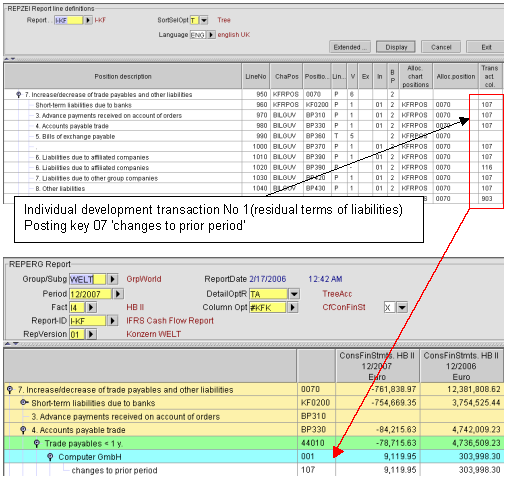

Values are identified by comparing current values with those of the prior period, and the total difference is to be broken down into transaction-related and exchange rate-related changes.

If we transfer these items to the German balance sheet structure as set out in section 266 (2) C and D of the Handelsgesetzbuch (HGB - German Commercial Code), these are changes to the following asset items:

Figure: Storing the respective liabilities items in the report line description

If these items are not booked separately as cash and non-cash extraordinary items in financial accounting, this information can be shown in IDL Konsis using statistical accounts.

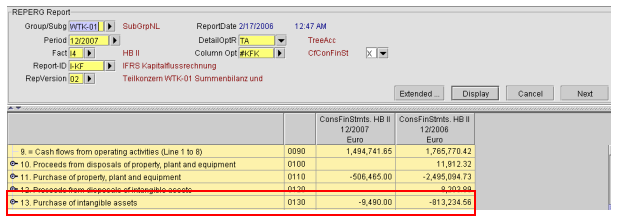

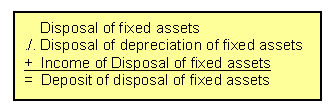

In general, proceeds from the disposal of assets cannot be seen directly from the statement of changes in fixed assets. In order to make it possible to break down the payments received for property, plant and equipment, the income and expenses from the disposal of assets must be recorded separately according using the individual fixed asset categories.

Figure: Deriving the figures indirectly

Figure: Presentation in cash flow report

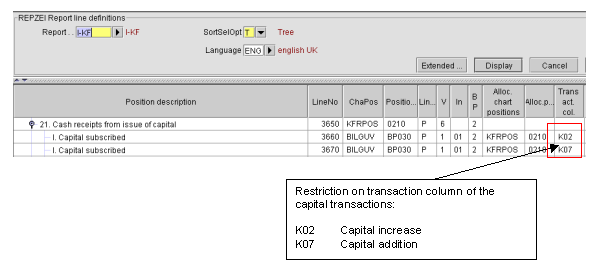

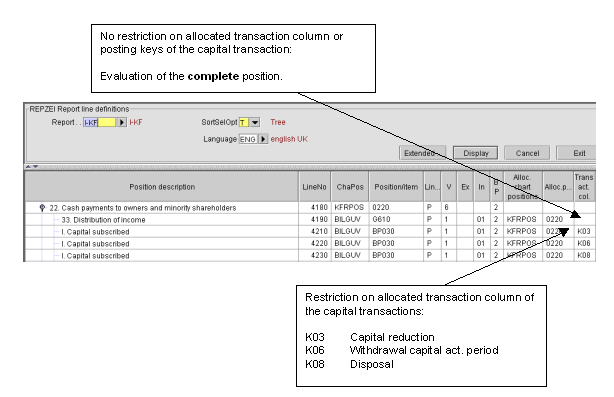

This information can be shown directly in IDL Konsis from the statement of changes in shareholders? equity in the cash flow statement.

Figure: Restriction to statement columns from the statement of changes in shareholders? equity

This information can be shown directly in IDL Konsis from the statement of changes in shareholders? equity in the cash flow statement.

Figure: Presentation in cash flow report

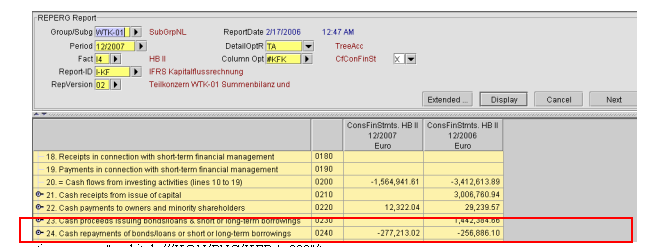

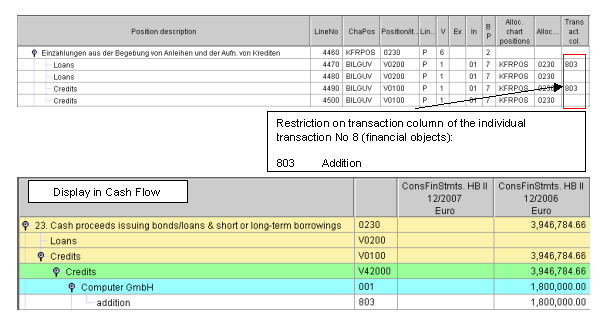

Example: Income from issuing bonds and taking out (financial) loans

Figure: Presentation of payments in report line structure

Example: Payouts from issuing bonds and taking out (financial) loans

Figure: Presentation of payments in report line structure

In order to ensure unquestionable charging or for necessary corrections to certain items in the cash flow report, it is necessary to call up or provide the information with the desired level of detail via the chart of accounts even when the data is being collected. The following accounts are not complete as IDL Konsis already includes certain accounts/transactions (accounts for exchange rate differences or exchange rate difference keys) as a result of the technical system, that are also of importance for the cash flow statement:

The above information is to be maintained using corresponding statistical accounts, so that these can then be shown in IDL Konsis in the cash flow statement.

This list is not exhaustive.

Extensive details for the presentation of change to the group of consolidated companies are shown in Section B of the documentation on the cash flow statement.

IAS 7.40 demands, over and above the cash flow statement, certain additional information, examples of which are discussed in IAS 7 Appendix A Note A:

Figure: Additional information according to IAS 7 Appendix A Note A discussed by way of example

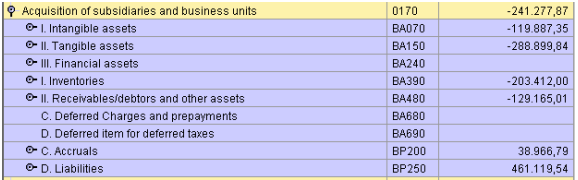

Within the cash flow statement, the payment of the total price is shown as an investment.

Figure: Presentation in cash flow report

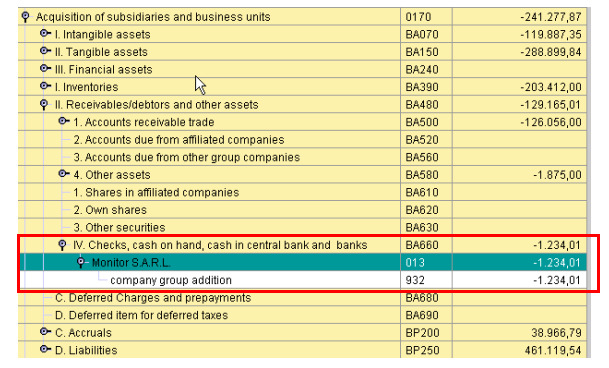

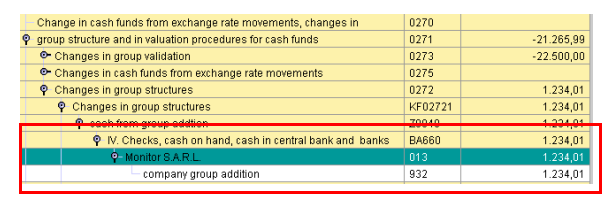

The cash and cash equivalents included in the purchase price are disclosed separately in the cash flow statement. The cash and cash equivalents acquired may not be disclosed under cash and cash equivalents for the current period. They are disclosed separately as cash and cash equivalents acquired from additions to the group of consolidated companies.

Figure: Sample disclosure of purchase price payment

Figure: Sample disclosure of acquired cash and cash equivalents

In this regard, please see Section B of the documentation. This deals with technical realization of additions to the group of consolidated companies in detail.

Relevance of the date of acquisition

It is mandatory to identify the date of initial consolidation. From the perspective of the cash flow statement, it is not sufficient to only know the year of acquisition. It is important to know whether initial consolidation was on January 1, during the year or on December 31. These specifications can be stored in KTKGES, however these are not currently evaluated.

For the automatic generation of the acquisition payment and the acquired cash and cash equivalents, IDL Konsis needs financial statements for the date of acquisition.

This consolidation process is not yet fully implemented in Release 5.4.1. The consolidation processing currently implemented in IDL Konsis, <KS>, only cancels the receipts from the capital carryforward. Full identification of the impact of deconsolidation is included in the development for the next version of IDL Konsis.

The impact of deconsolidation can currently only be shown with the aid of statistical additional information in the cash flow statement.