§ 304 HGB applies to eliminating intermediate results. If an asset was sold between the companies involved at a price that is either higher or lower than the acquisition/production price entered in the group view and this asset is still in the possession of the receiving group company, then the balance sheet value will show either a profit or a loss (intermediate result). Nevertheless, profits or losses should only be taken into consideration in the balance sheet after they have actually been realized from outside parties. Profit or losses based on inner group supply and service relationships are to be corrected at full value in the stock values and annual profits and losses.

The following processing steps are to be performed in IDL Konsis:

The various steps are explained in the chapters that follow.

In order for you to be able to use the application 'Elimination of IC profit from fixed assets' (ZA), you will have to set up the consolidation parameter 'ZA' first. Please refer to the following description to learn more about what the various fields mean:

[Group /sub-group ]: Entry of group /sub-group. Each group /sub-group can set up its own parameters. The parameters for 'ZA' are carried forward as part of forming carry forwards for the group (PERKTK).

[Period]: Entry of the period for which the parameter is to apply.

[Fact]: Entry of the fact with which the consolidation function is to be performed.

[Carry forward postings summary]:When you activate this field by placing an 'X,' the data from the 'ZA-voucher' with the group carry forward will be collected and carried forward to a 'VX-voucher'. Here, posting lines that have the same account number, same posting key and same posting record number will be combined. The standard setting here is '-'.

[Company for posting]: mandatory entry. By selecting the characteristic 'Z' = posting for addition company or 'A' = posting for disposal company, you determine which company the postings are to be made with. If you select the characteristic 'A,' the system will post the A/P cost disposals and accruing depreciation with the disposal company as in the past. If you select 'Z,' a re-posting of the postings with the disposal company will take place with the receiving company. IC profit always remains with the disposal company. In the results, the asset will then be shown together with the customer that uses that asset. This variant takes the fact into account that it makes more sense to have the company that has sold an asset to another company no longer bear the burden of depreciation for this asset.

[Account IC profit from fixed assets]: mandatory entry of an account that IC profit is to be posted to when the consolidation function is activated.

[Account IC loss from fixed assets]: optional entry of an account that an IC loss should be posted to when the consolidation function is activated. If no account is entered here, losses will be posted to the account entered in the mandatory field 'account IC profit from fixed assets.'

[Carry forward]: optional entry. If no account has been entered in the field entitled 'carry forward', the posting of the carry forward will take place with the carry forward account stored in KTKPAR_KK.

[Neutralization account]:optional entry. If a neutralization account has been entered here, then additional postings will be automatically generated in the neutralization account in the ZA consolidation vouchers. These postings neutralize shifts in balance sheet and / or profit+loss results between the two companies mentioned in the voucher. By taking this account into consideration in the group report, you can arrange for the company details of the results to match the company financial statement results perfectly. If no account is entered here, then no neutralization postings will be entered for the ZA vouchers.

If the characteristic 'Z' = posting for addition company has been selected in the 'company for postings' field, posting keys with the usage tag 'XZA' must be set up for proper postings by column (column 're-posting'). Once posting keys for A/P cost and depreciation have been set up with the usage tag 'XZA,' all of the postings will be issued with the respective stored posting keys when the consolidation function 'ZA' is activated. If no special posting keys have been set up despite selecting the characteristic 'Z,' the posting keys for the fixed asset transactions will be missing in the consolidation vouchers.

If you work with the continued standard transaction developments of IDL Konsis, these transaction development enhancements are contained in the import files in the supply batch file and will already exist when these files are imported on a regular basis.

In order to be able to completely process the data for the consolidation function 'Elimination of IC profit from fixed assets ' (ZA) (e.g. status display in the company financial statement monitor, carry forward, currency conversion), a switch for controlling IC fixed asset transactions (ICANLBEW) must be activated in the master tables for periods (ABR) and facts (FAC).

By activating ICANLBEW in 'FAC' and 'ABR,' a status column on IC fixed asset transactions will be displayed in the company financial statement monitor. A double click onto this column allows you to branch off into the overview "IC fixed asset transactions" (ICANLBEW) by using the sort option 'GA.'

The status display is based on entries that have been made in the processing control on 'ICANLBEW'. These entries will be updated each time that data changes. Due to the fact that no reconciliation takes place between IC fixed asset transactions and account balances, the checkpoint 'ICANLBEW' usually will not display any error messages. Furthermore, checksums will be calculated for the database and stored in the processing control file.

The carry forward of IC fixed asset transactions depends on whether the control of IC fixed asset transactions (ICANLBEW) has been activated for both the previous and the current period (ABR) and for the respective fact (FAC).

For the disposal of a fixed asset good with the company that is doing the selling and the addition of a fixed asset good with the company that is making the purchase , an IC fixed asset object must be set up for both sides. This is done by branching off into the application 'ICANLOBJ'.

After entering in a company number and a ?%? sign in the second field, all of the existing IC fixed asset objects for this particular company will appear. Select either ?Action,? ?Create new data? or the star in the toolbar to set up a new IC fixed asset object. Then, the single IC fixed asset object file that the data for the IC fixed asset object (ICANLOBJ) can be entered in will open up.

The various fields have the following meanings:

[Company]:company number of the selling (disposal) or acquiring (receiving) company

[Fixed asset object]: Any 14-digit term for the new IC fixed asset object that still needs to be set up

[IC fixed asset card type]: Here, the determination is made as to what card type the ICANLOBJ should be: A= disposal of IC fixed asset object (for the selling company), Z= addition of IC fixed asset object (for the acquiring company)

[Fixed asset object description]: Term for the IC fixed asset object

[Chart of accounts+ account]: Entry of the chart of accounts and fixed asset account which the IC fixed asset object has been assigned to

[Acquisition date]: Entry of the date of purchase of the fixed asset object. With the disposal ICANLOBJ this is the original date of purchase. With the addition ICANLOBJ it is the exact date of the addition.

[Disposal of group companies date]: A date should not be entered in this field until after the fixed asset object has been sold to a third-party, in other words, an organization that does not belong to the group.

[Depreciation method]: Various types of depreciation are available to choose from. For further information, please refer to the documentation'Automatic Depreciation'

[Period of depreciation]: if the depreciation type=L has been entered here, then the period of depreciation can be entered in years. The costs of acquisition will then be depreciated in equal amounts for the specified period of depreciation. For more details concerning the period of depreciation and its effects, please refer to the documentationAutomatic Depreciation

[Depreciation rate]: If depreciation type=GD is selected, the rate for depreciation can be entered. Otherwise this field should remain empty.

[Amount depreciation]: The amount that is to be depreciated each business year should be stored. If the posting value is lower than the depreciation amount stored at the end of the depreciation period, only this lower amount will be generated. The fixed asset object will be automatically depreciated down to the posting value = 0.00. Further information on this is available in the documentation Automatic Depreciation.

[Account for accumulated depreciation]: Optional entry of a balance sheet account to which the offsetting entry of depreciation should be made. If this field is left empty, the balance sheet account of the IC fixed asset object (ICANLOBJ) will be used.

[Account for depreciation]: Entry of a depreciation account (Acc.Flag=D) to which depreciation is to be posted. Any account may be chosen if depreciation type 'F' has been selected,.

[Depreciation controlling object1]: Assignment of a controlling object to the account for depreciation is possible.

[Allocated fixed asset object]: If an IC fixed asset object (ICANLOBJ) is already listed at the company level (other fact or chart of accounts) and the entries of the IC fixed asset object are intended to refer to the company fixed asset object, a distinction can be made by entering the company fixed asset object that pertains to it.

[Addition company]: Entry of a company that has been sold to (with (IC fixed asset type=A)). When setting up the additional ICANLOBJ, this field should remain empty (IC fixed asset type=Z).

[Company No. of origin card]: Entry of the company that was purchased from (with IC fixed asset type=Z). When setting up the disposal ICANLOBJ (IC fixed asset type=A), this field should be left empty.

[Fixed asset of origin card]: Entry of the fixed asset object of the company that is doing the selling. When setting up the disposal ICANLOBJ (IC fixed asset type=A), no entry is necessary. A voucher will be generated automatically once the data has been saved. When setting up the addition ICANLOBJ (IC fixed asset type=Z), the ICANLOBJ of the selling company (IC fixed asset type=A) mustbe entered here.

[IC Account for income]: Entry of an income and expense account that income and expenses can be posted to at the company level. With IC fixed asset type=Z, this field should be left empty.

[Disposal controlling object]: Entry of a controlling object in the ?disposal of earnings account? is possible.

[Valid from / until]:Entry of the starting date/ ending date as of which the ICANLOBJ is valid/ validation ended.

GES011 sells a machine to GES013 for EUR 75,000. The original A/P cost was EUR 80,000 EUR, the date of purchase was 01/01/2007, the depreciation type is linear with a period of depreciation of 8 years in total. In other words, 3 years have already been depreciated. The current net book value is therefore 80,000-30,000=50,000 EUR. The return from the disposal of the fixed asset is thus EUR 25,000.

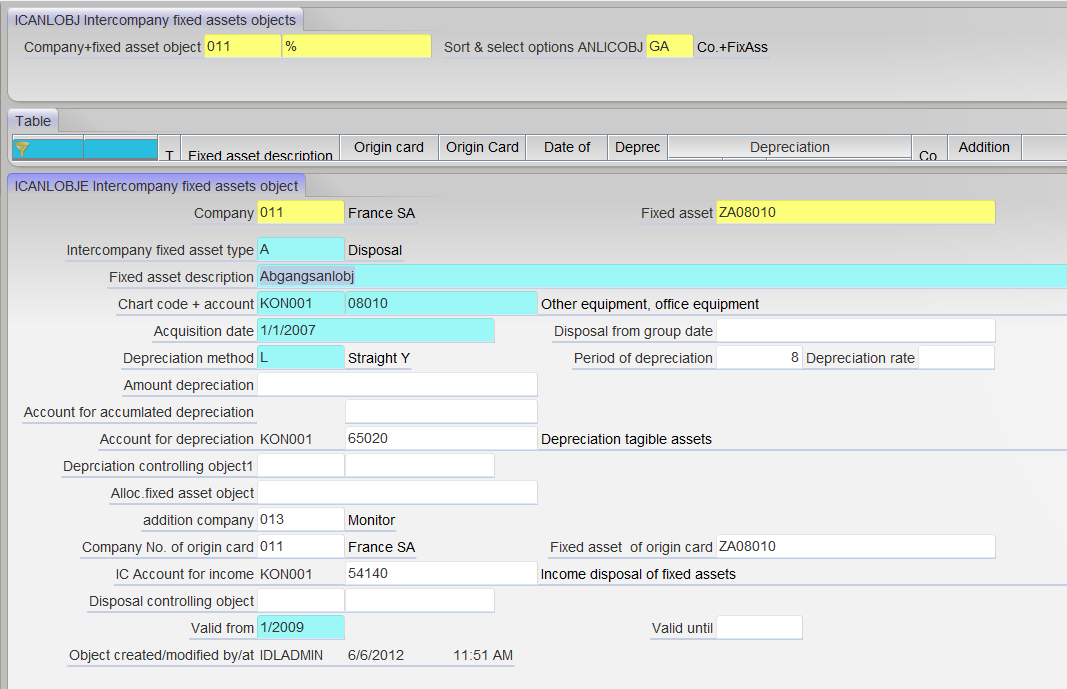

Disposal of an IC fixed asset object:

Figure: Disposal of the ICANLOBJ of the selling company GES011

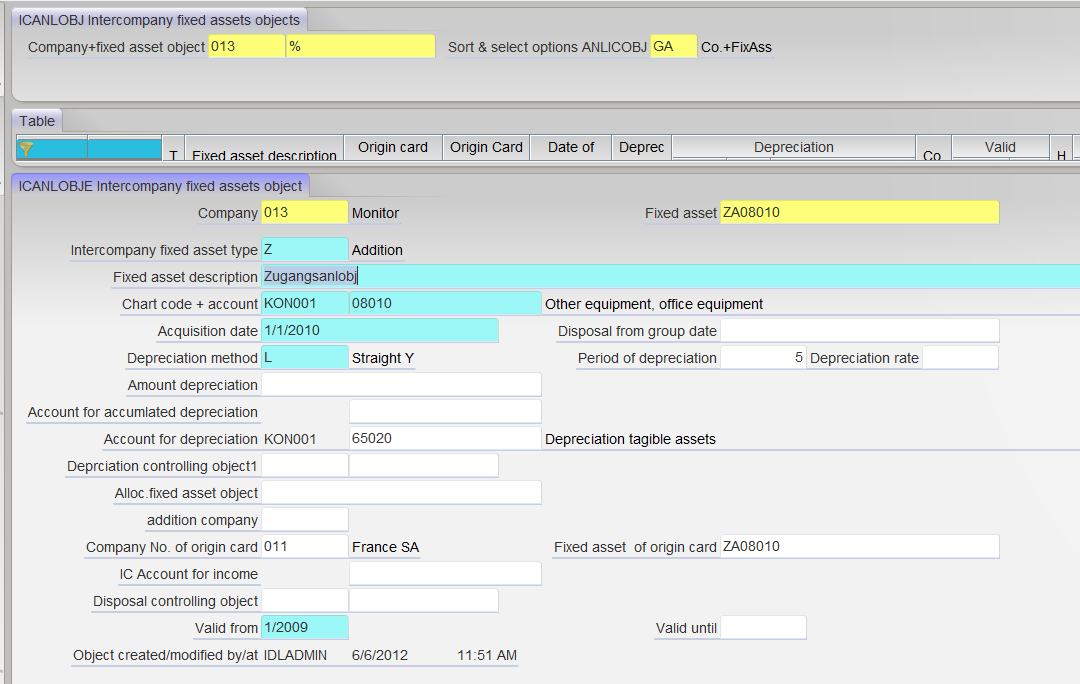

Additional IC fixed asset object

Figure: Addition of the selling company GES013

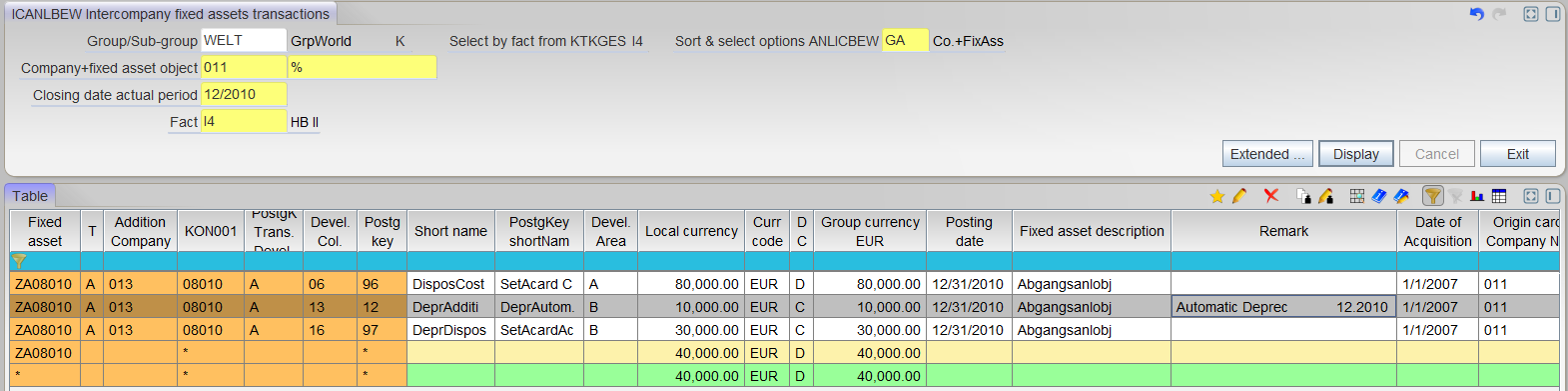

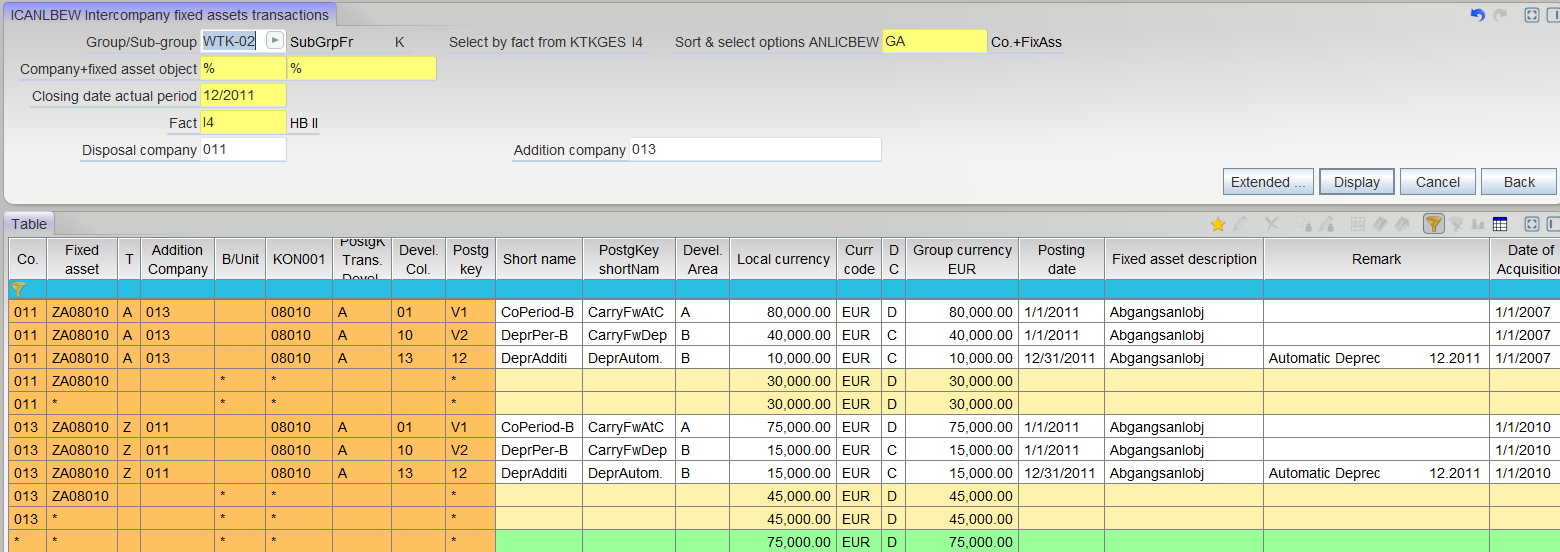

The fixed asset transactions for the group fixed asset object are maintained in the 'ICANLBEW' that cancels the disposal and addition of the machine inside the group. Certain posting keys must be set up in order to be able to do so.

The disposal of the machine will be canceled with the selling company by using the posting key 96 'A/P cost Einstellung Vortr.Disposal card' to reverse the A/P that has been disposed of. By using the posting key 97 'Set cum. depreciation disposal card' the depreciation can be reversed.

If, according to the IC fixed asset object, depreciation postings still need to be determined for the current period, these will be determined and entered a u t o m a t i c a l l y as soon as the transaction changes. Depreciation will also be recalculated automatically every time there is a change in IC fixed asset transactions (manual entry, import, carry forward).

Figure: Maintenance of fixed asset transactions at the group level on the seller?s side including automatic calculation of depreciation (dark gray line)

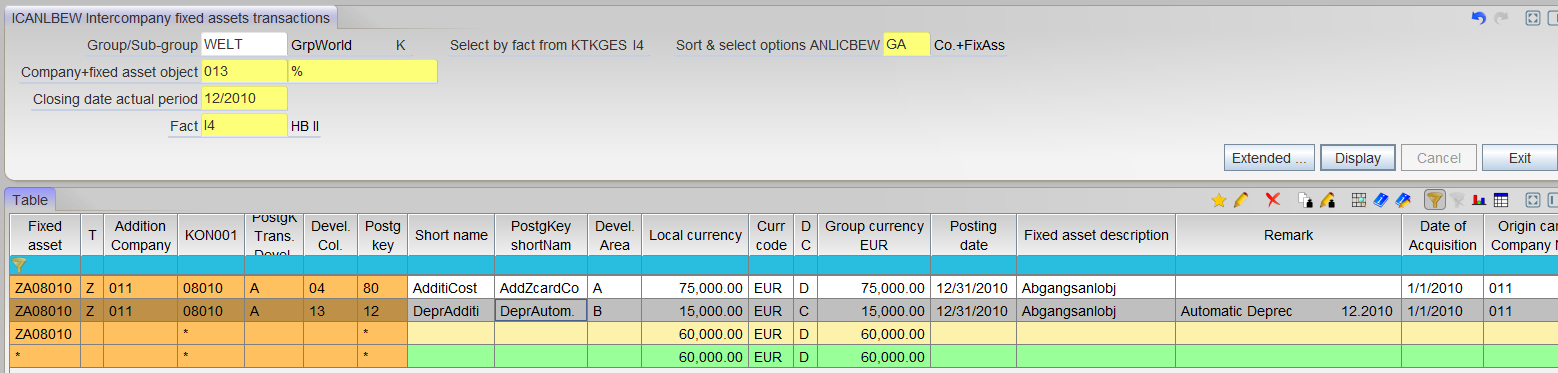

The addition of the machine will be canceled at the group fixed asset object level of the purchasing company by reversing the depreciation with the posting key 80 'A/P cost addition Addition card.' Here, too, depreciations will be generated automatically for the current period, if foreseen according to ICANLOBJ.

Figure: fixed asset transactions at the group level on the buyer?s side with depreciation calculated automatically (dark grey line)

To calculate currency conversion effects from the transactions, it is mandatory that you keep track of the respective transactions in the local currency.

With foreign currency companies, you should make sure you always perform currency conversion in the company financial statement after processing IC fixed asset transactions.The IC fixed asset transactions will be validated, therefore the 'WUM' status in the company financial statement will change if currency conversion has not been performed. The status of 'IC ANLBEW' will remain unchanged, however.

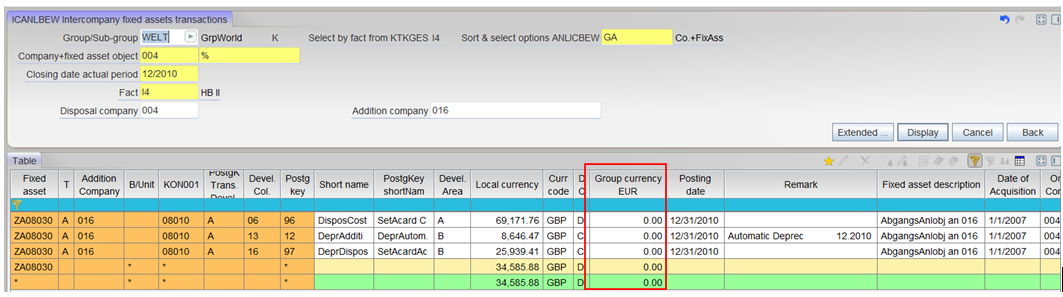

Example: ICANLBEW for a foreign currency company:

The column 'Group currency' will be empty before currency conversion is performed.

Figure: IC ANLBEW before currency conversion

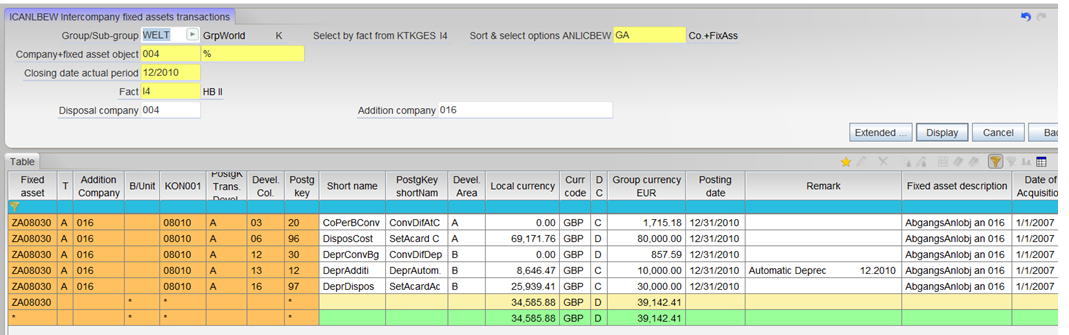

Group currency values will not be shown, nor will the currency conversion effect be calculated until after currency conversion has been performed.

Figure: Group currency values after currency conversion has been performed

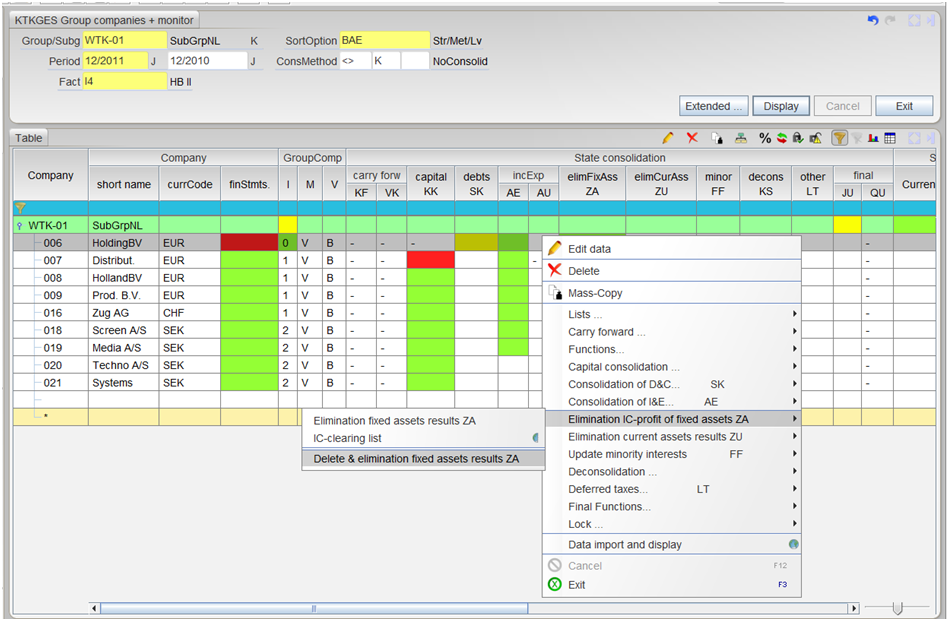

The menu item 'Action' - 'Elimination of IC profit of fixed assets ZA' should be used to calculate and make a posting. There are 2 versions:

Figure: Trigger 'ZA' in 'KTKGES'

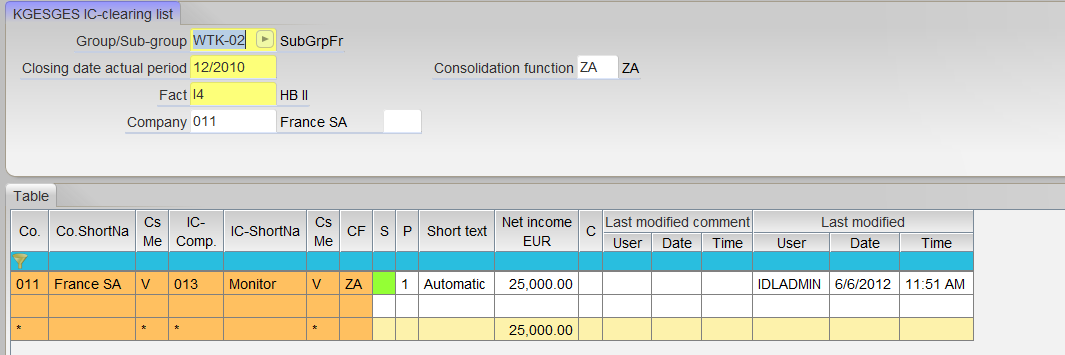

Double-clicking onto the 'ZA' status field or the 'ZA' menu will take you to the IC clearing list (KGESGES). All of the disposal relationships of the respective company will be displayed in the IC clearing list (KGESGES).

From the IC clearing list you can branch off directly into various applications after marking the respective line and pressing the 'right mouse button' or via 'Action' in the toolbar. For the 'ZA,' these are branching possibilities off into the company financial statement monitor (EA), consolidation vouchers (KONBUCH) or IC fixed asset transactions (ICANLBEW) for the respective company. All the other applications (IC subaccount balance, repeat IC clearing...) are only available for 'SK/AE.' They are displayed here for technical reasons, however.

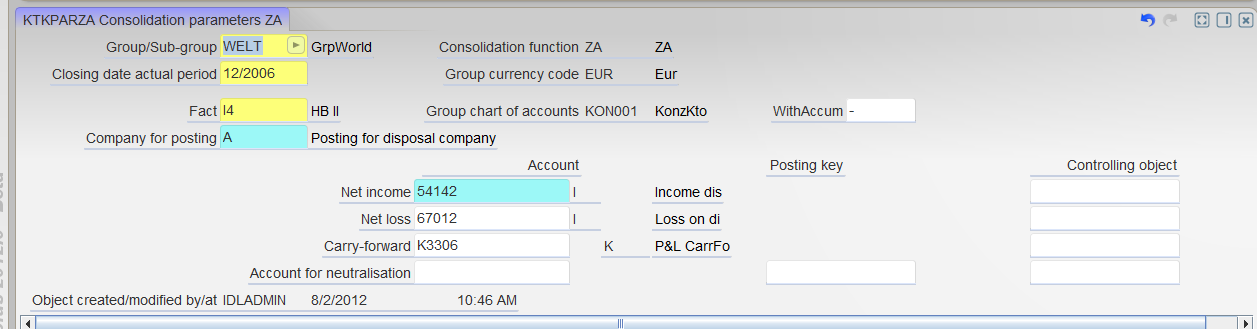

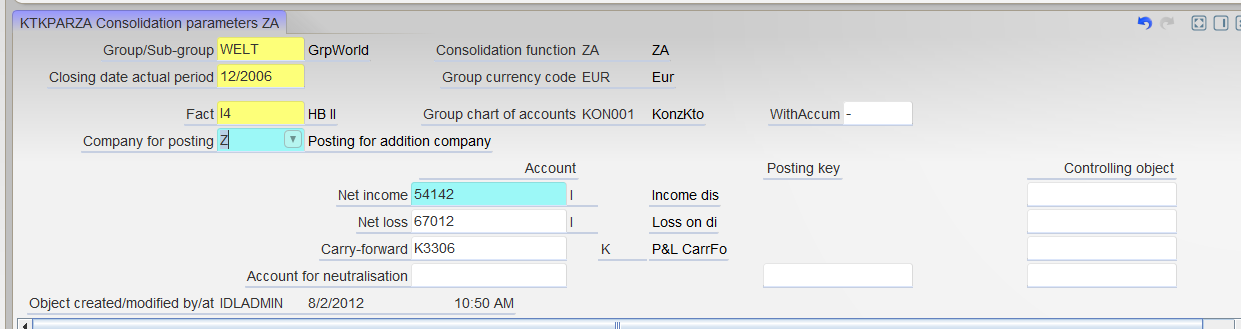

An 'A' is entered in 'company for posting' field in the consolidation parameter 'ZA' for a posting for a disposal company.

Figure: KTKPAR-ZA with the characterization 'A' for a posting for disposal company

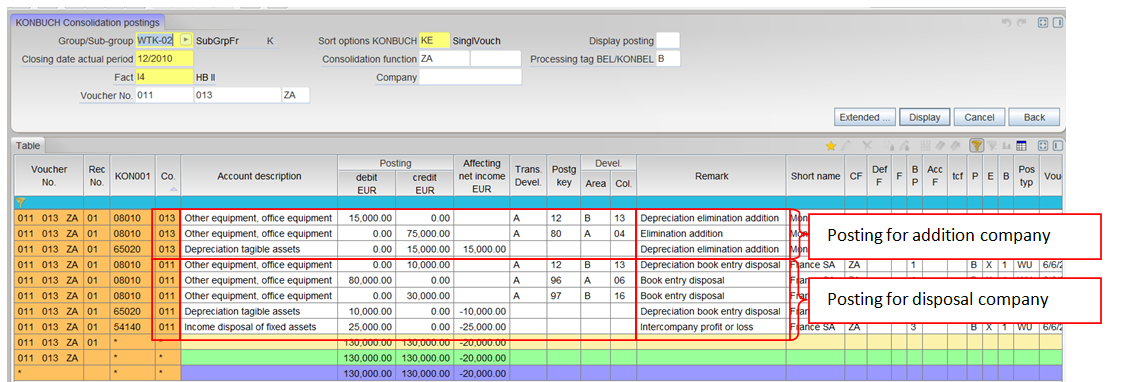

After updating IC asset transactions (as described above) and performing the consolidation function 'ZA,' the following voucher will be generated:

Figure: Posting voucher on elimination of IC profit with a posting for a addition company

Once a carry forward for a period for the company financial statement (PERGES) has taken place, the IC fixed asset transactions will be carried forward as follows:

Figure: IC fixed asset transactions during the following period

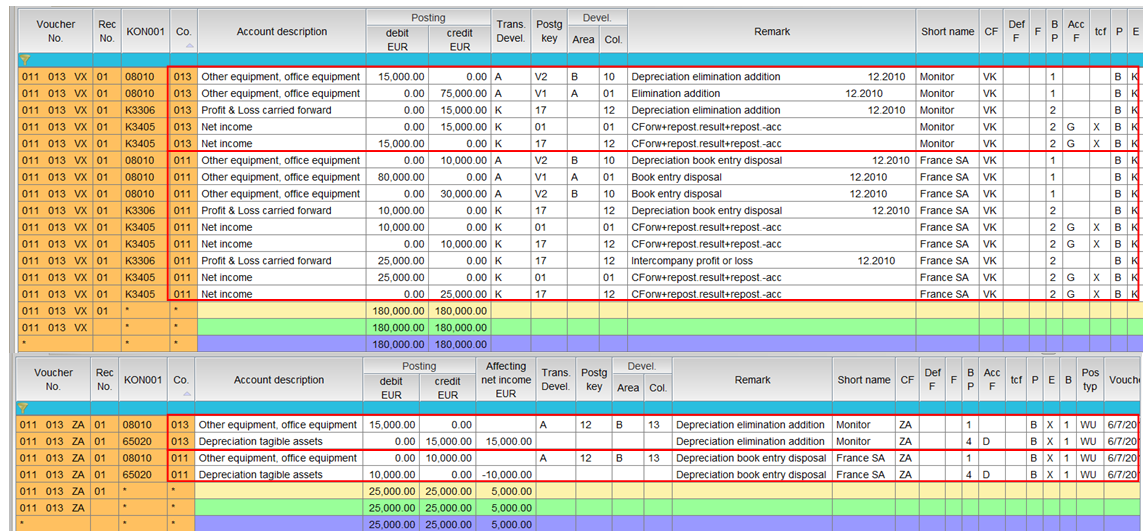

The depreciation for the following period will be entered automatically and forms the basis for the 'ZA' voucher for the following period. With the group carry forward (PERKTK), the 'ZA' voucher for the previous period will be converted into a VX voucher. All of the elements recognized in profit and losses will be posted to the retained earnings account. However, 'ZA' processing must be performed to ensure that the depreciation for the following period is eliminated again. A new 'ZA' voucher will be generated in which the depreciation for the following period will be reversed again.

Figure: Consolidation vouchers in the following period

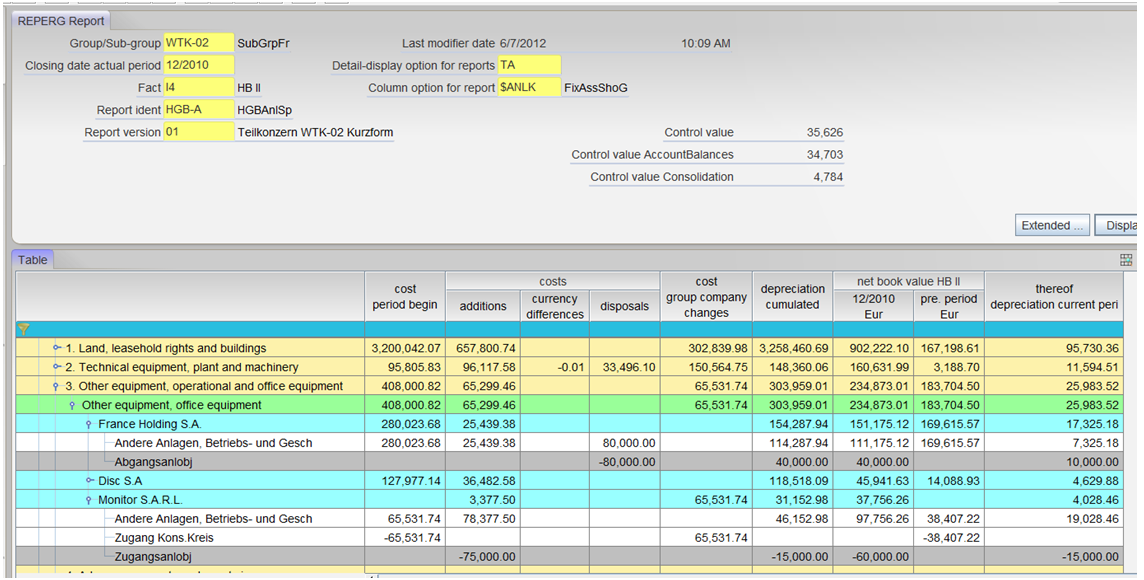

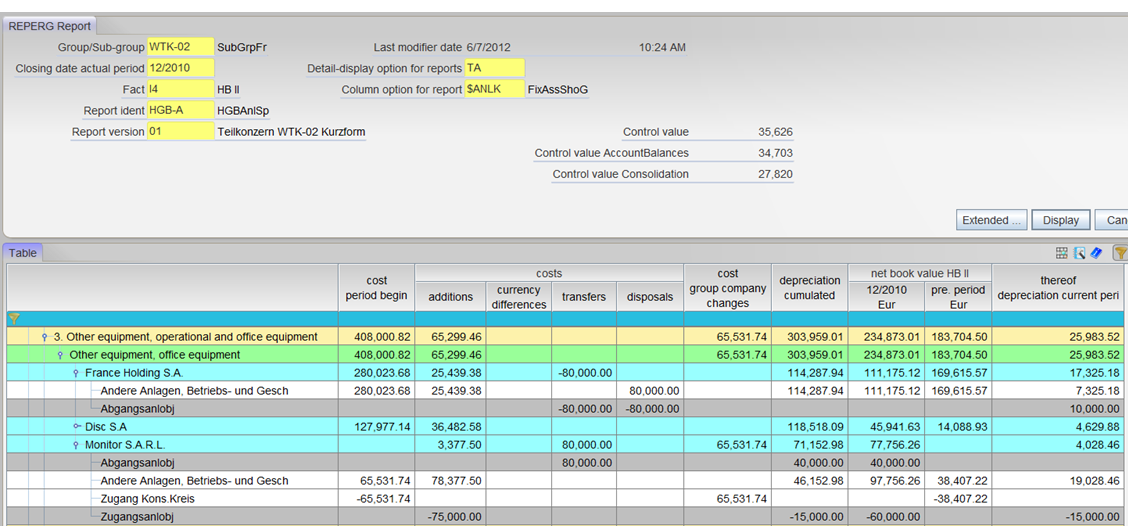

Elimination of IC profit will appear as follows in the group asset report:

Figure: Elimination of IC profit, presentation in the asset report (column option ANLK)

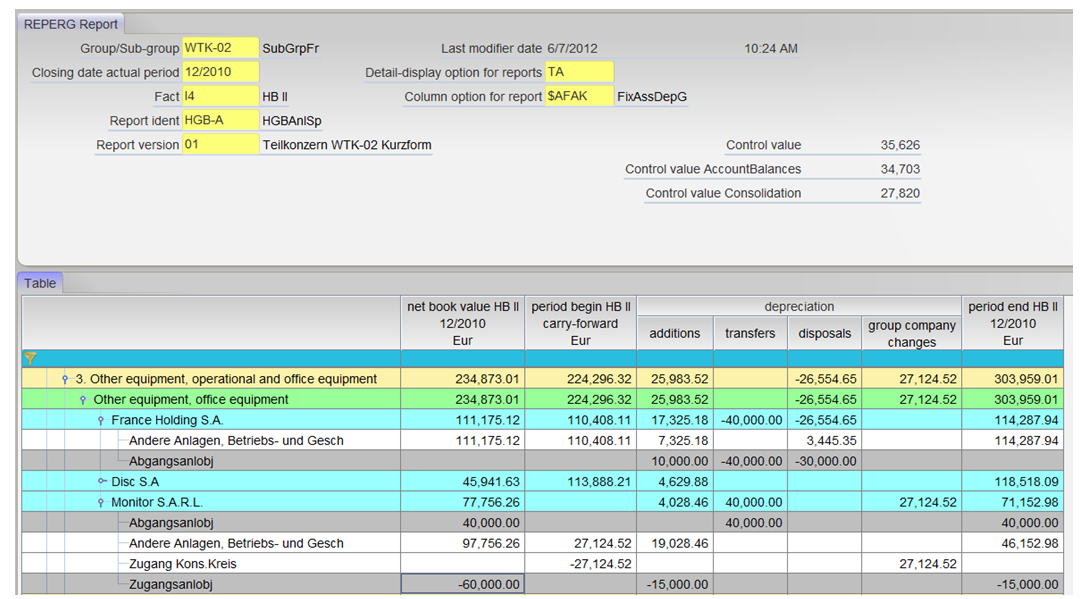

Figure: Elimination of IC profit, presentation in the asset report (column option AFAK)

A 'Z' is entered in 'company for posting' field in the consolidation parameter 'ZA' for a posting for an additon company.

Figure: KTKPAR-ZA with the characterization 'Z' for a posting for addition company

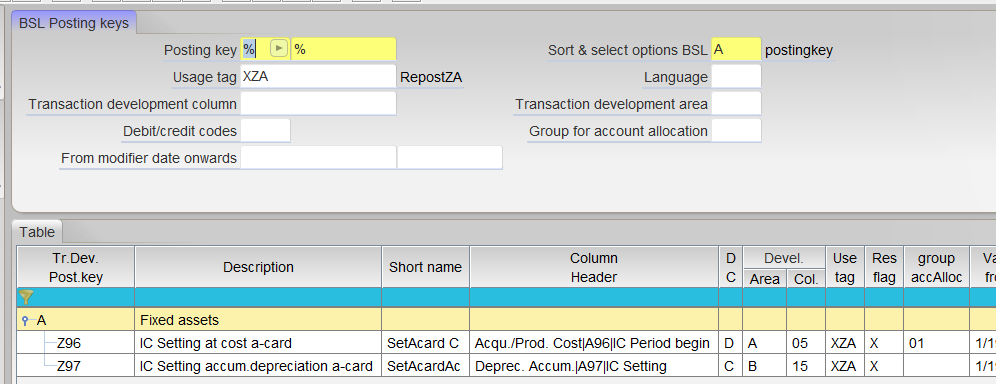

Posting keys with the usage tag 'XLA' should be generated to ensure that the re-postings that have been made are assigned to the proper transaction development column.

Figure: Posting key with the usage tag 'XZA'

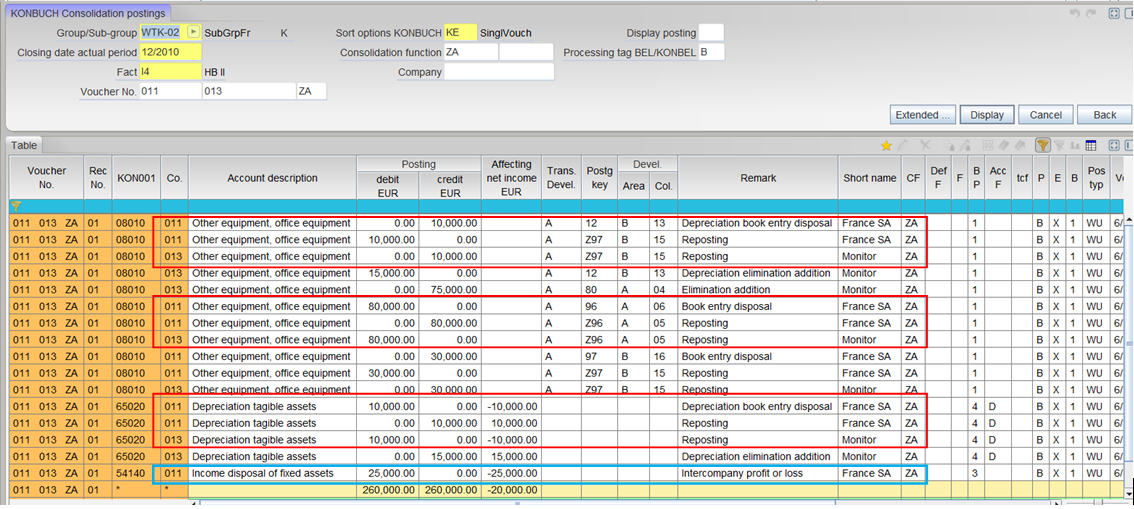

The following voucher will be generated after IC asset transactions have been entered (as described above) and the consolidation function 'ZA' has been performed:

Figure: Consolidation voucher with the characterization 'Z' = Posting for addition company

The voucher shows that all of the postings that pertain to the disposal company have been reposted to the receiving company (red borders). Only the intermediate result will remain with the disposal company (blue borders). This ensures that the fixed asset object is shown for the buyer that actually uses this asset.

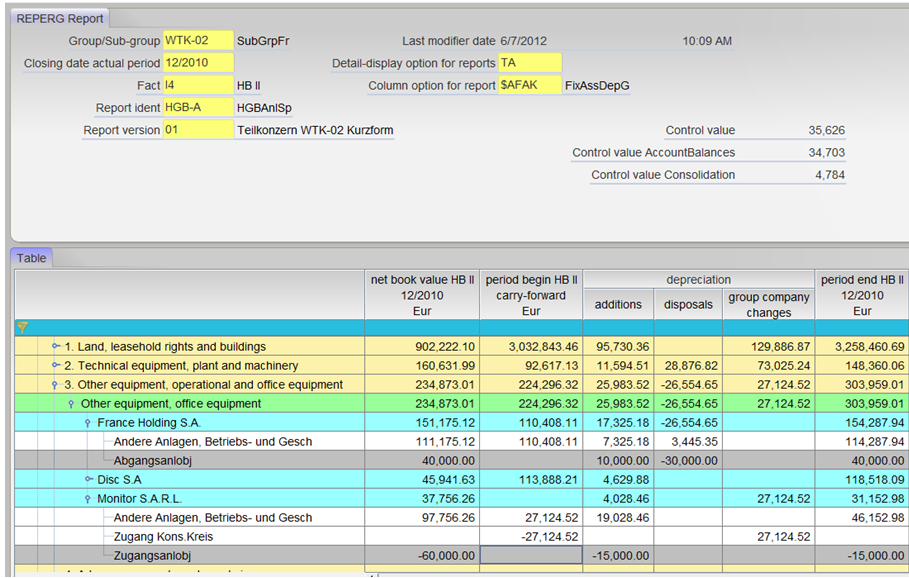

Elimination of IC profit is displayed as follows in the group asset report:

Figure: Elimination of IC profit, presentation in the asset report (column option ANLK)

Figure: Elimination of IC profit, presentation in the asset report (column option AFAK)