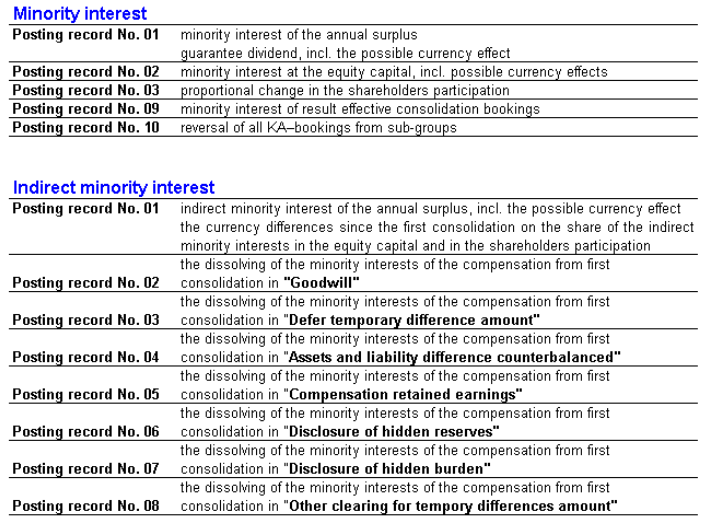

The statutory provisions governing the treatment of other shareholders are laid down in § 307 HGB :

If other external shareholders are involved in an included subsidiary, an 'adjustment item for shares held by other shareholders' must be created within the group balance sheet in the corresponding amount. This must be included in equity as a separate item. The basis of its calculation will vary depending on the choice of initial consolidation model (book value method, revaluation method).

The adjustment item need only be shown in respect of shares in subsidiaries which are included in the group annual accounts, and which do not belong to the parent company. If subsidiaries which are not included in the group annual accounts hold shares in a company which is included, such shares will be treated as shares held by third party shareholders.

The calculation should be based on the equity items as specified in § 266 Paragraph 3 A. of the German Commercial Code:

The valuation base of these items in the commercial balance sheet II / revaluation balance sheet on the computation date are multiplied by the relevant share quota of the other shareholders. If the book value method is chosen for the initial consolidation, the adjustment item will not include any passive reserves / passive charcompany However, if the revaluation method is chosen, the adjustment item will include passive reserves / passive charcompany

In respect of the subsequent consolidations, the adjustment item should be recalculated as of the closing date on the basis of the commercial balance sheet II or the continued re-evaluation balance sheet. This ensures that all equity changes are automatically reflected in the adjustment item.

When calculating the minority holdings, a pro-rata consideration of consolidation processes is not required by law. Commentators are currently not agreed on this issue. Küting/Weber and Ordelheide have stated a fundamental preference for the pro-rata consideration of consolidation measures (see Küting/Weber, § 307 Circular 11).

If the effort involved in ascertaining the share of the other consolidation methods with an impact on earnings attributable to the other shareholders is disproportionate to the information gained thereby, this procedure need not be considered when determining the minority interests.

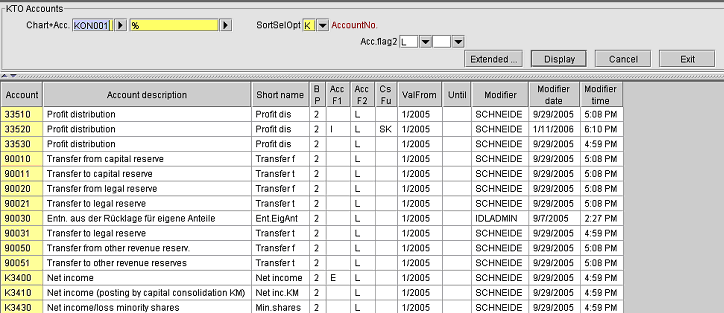

The correct calculation of minority interests requires the following settings in the master data:

All appropriation accounts and the annual surplus account must be stored using the account key 2 equals "L".

Screenshot Appropriation accounts with the account key 2 = L

The result-carried-forward account must be stored using the account key 1 = "X" (see screenshot). All L accounts are carried forward onto this account. If no X account is available, the L accounts are carried forward onto the 'ErgVorKto' stored in the FAC menu in respect of the consolidation data method.

Screenshot: result-carried-forward account

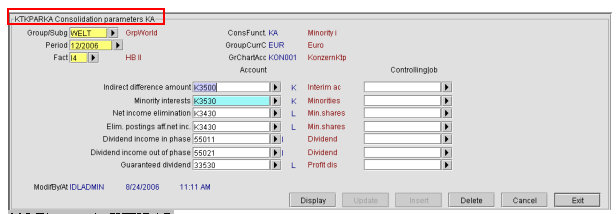

Screenshot: Inputs for determining the minority interest in the "KA" KTKPAR data set

When determining direct minority interests, two bases can be used to determine the minority interests in IDL Konsis:

Combined forms are not possible.

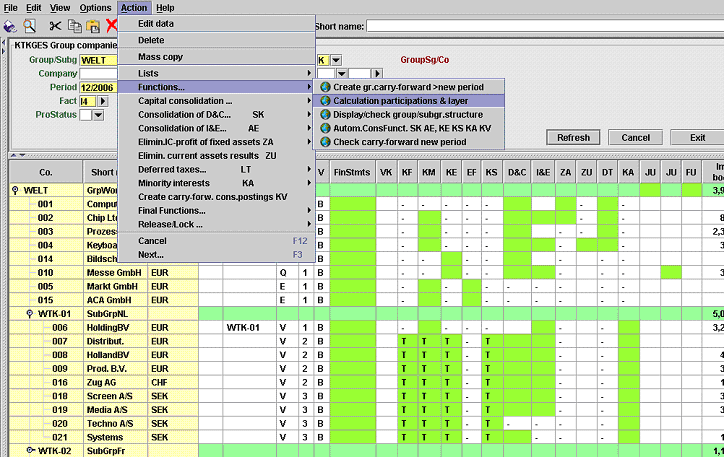

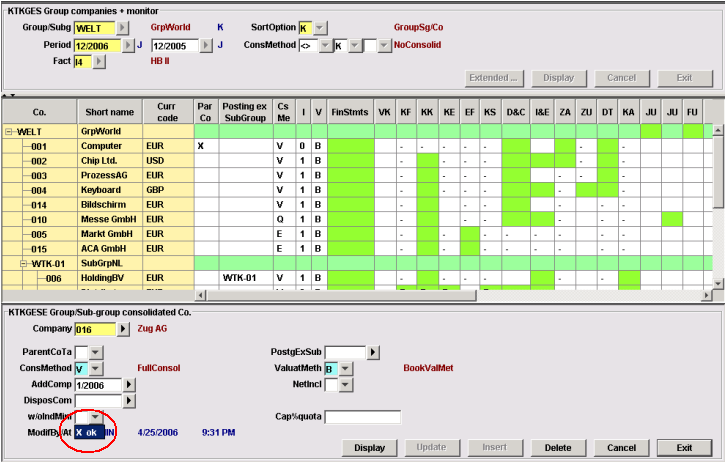

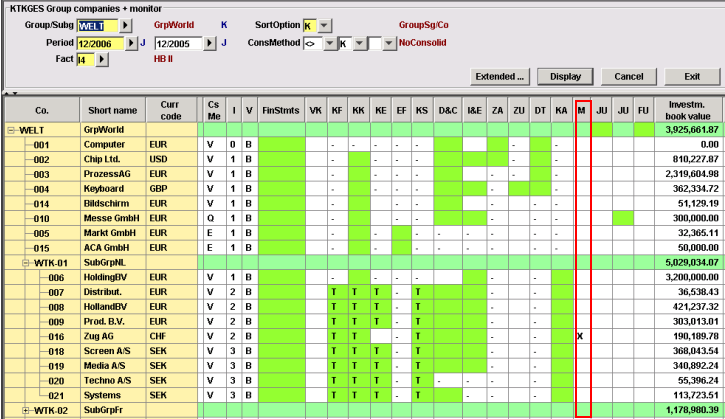

Through this process, shareholding movements (GESGES) are scanned to determine the level of the direct and/or indirect share held by minority interest shareholders. The resulting % share is indicated additively and multiplicatively next to the book value of interests in the KTKGES. The application can be run for all companies within the group which are not designated by a "K" (no inclusion) in the consolidation method field. However, the company in question must not be the group parent company, or equivalent thereto.

Screenshot: Triggering the "Participation and status calculation"

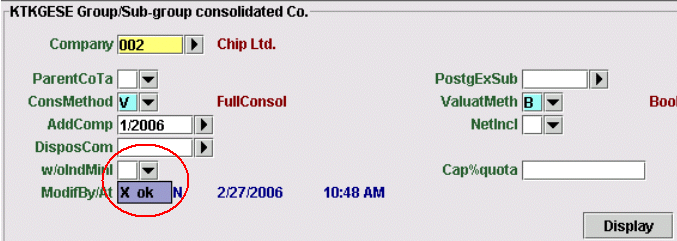

If, in a superordinate group, no indirect minority interests are to be calculated on principle, this can be controlled using the key in the KTKGESE individual data set application.

Screenshot: KTKGESE without calculation of indirect minority interests

The minority interests are calculated in the KTKGES

Screenshot: Triggering the automatic calculation of minority interests

Note on deleting existing KA entries:

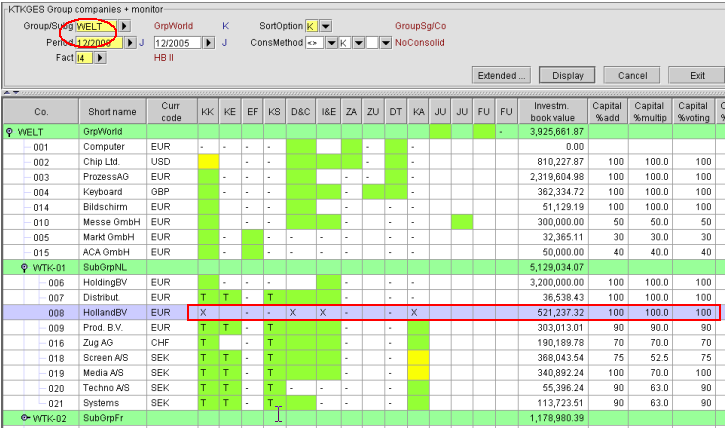

Direct minority interests within a group are deemed to be present if, in respect of a fully consolidated company, there is a direct shareholding of less than 100%.

In the KTKGES, in the appropriate company line, the direct share (see screenshot) in the company is displayed if the shareholding movements have been updated accordingly in the GESGES application.

Screenshot: KTKGES, depiction of direct minority interests

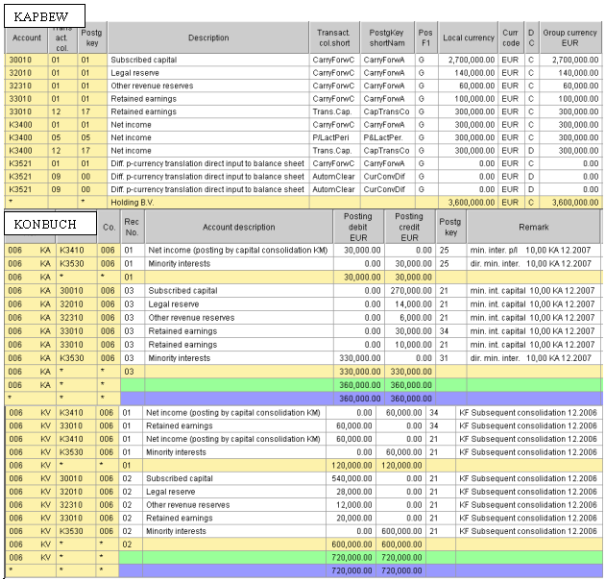

using the example of a minority interest calculation with capital movement.

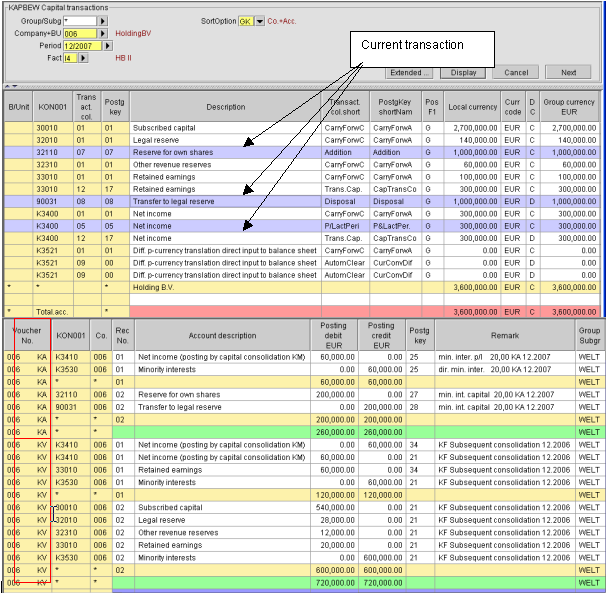

This presupposes that movements in respect of capital have been updated (KAPBEW applications). Advantage: The consolidation entries thus generated under Capital are booked using the correct column format, i.e. they are booked in the equity ageing report with the correct booking code for the column in question.

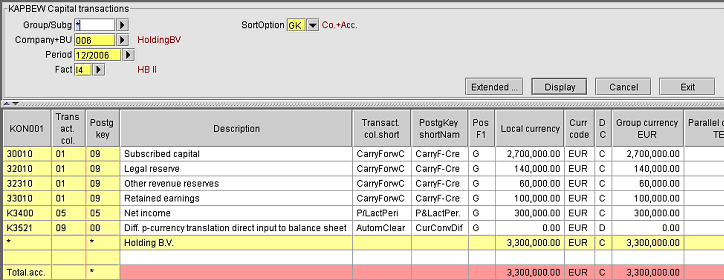

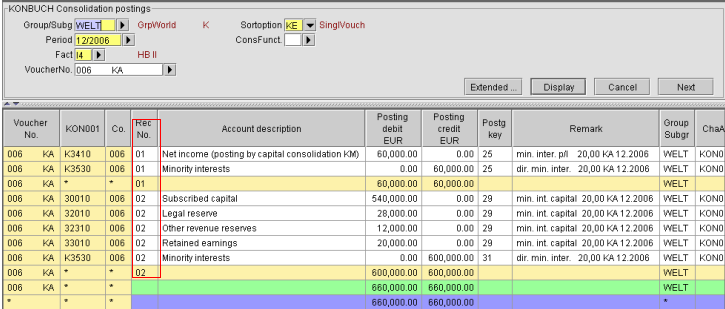

For the purpose of clarification, here is a view of current capital movements in Company 006, for which the minority interest calculation must now be carried out:

Screenshot: KAPBEW for Company 006

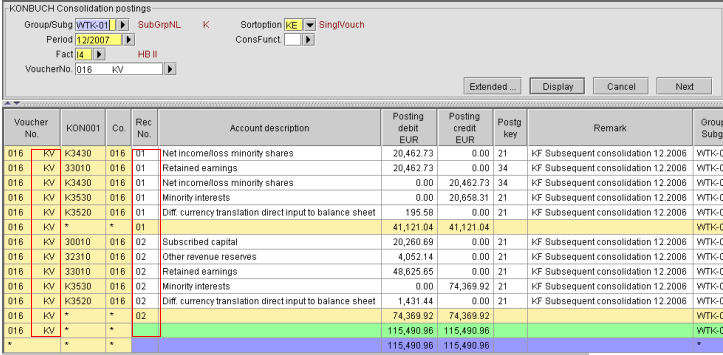

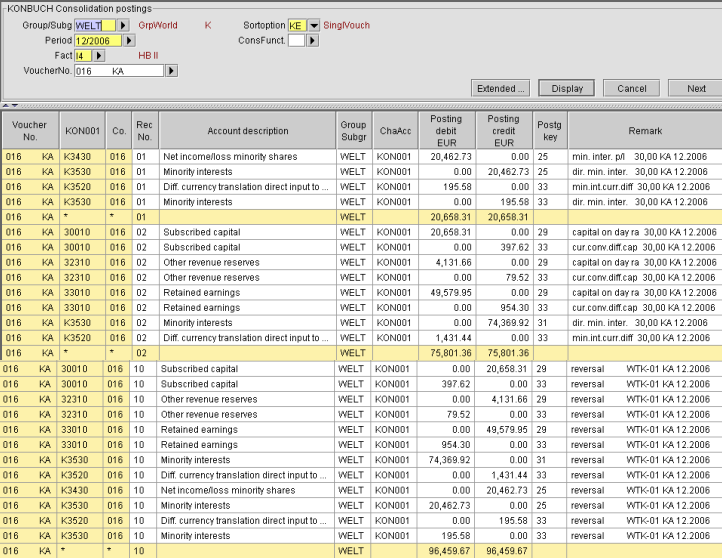

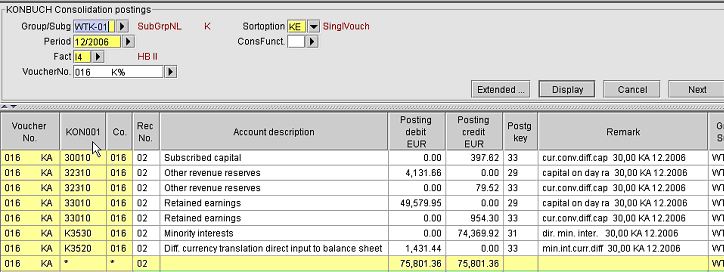

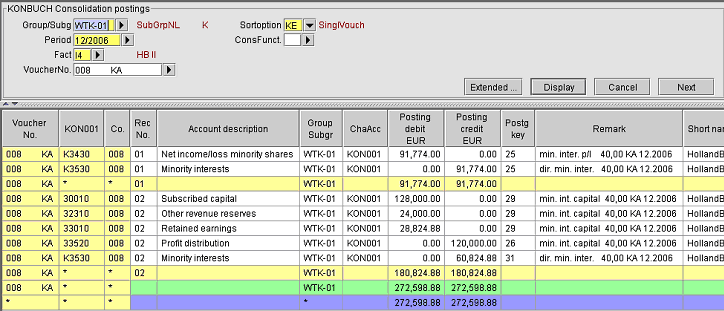

After triggering the "KA" application in the KTKGES, the following entry for the direct minority interests is made:

Screen shot: KONBUCH, entries for direct minority interests

The statement deals with two sets of facts:

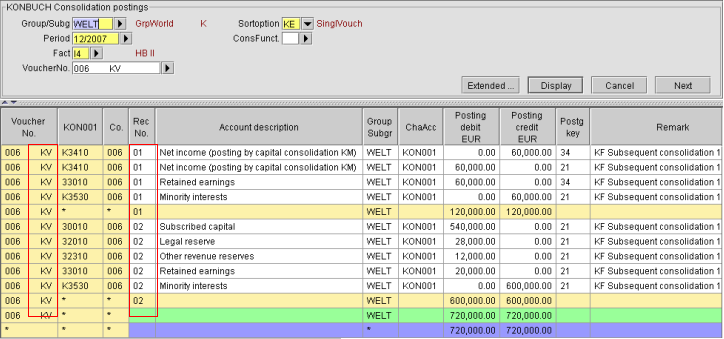

Using the example of company 006: The minority interest statements are carried forward on statement "006___KV". The annual surplus and capital are carried forward using separate accounting record numbers. In this regard, a balance is always struck in respect of one accounting record number per account.

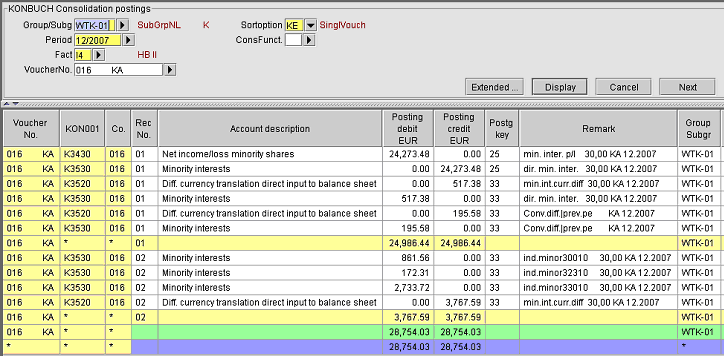

Screenshot: Direct minority interests in the follow-on period.

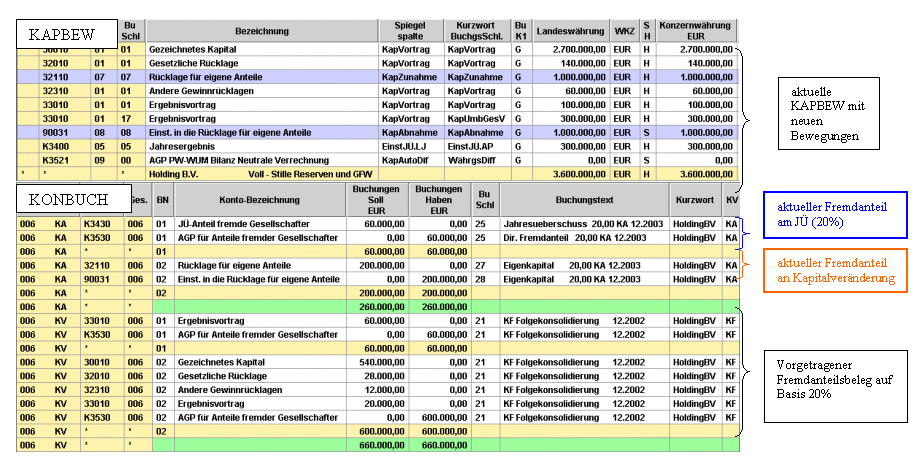

So: what does the minority interest statement for the current period look like now?

Here too, the calculation and identification of minority interests during the current period is carried out on the basis of capital movements. The minority interest is only calculated in respect of current capital movements (BSL 05,07,08). The other movements have already been included in the KV statement (XXX___KV). When calculating the minority interests, the capital movements with booking codes 01 (carried forward by computer) or 17 (capital book transfer company carried forward) are not included again.

The example of a minority interest calculation with capital movements is used as an example here.

This presupposes that the capital movements (KAPBEW applications) and the account conversion instruction (KTOUAW) have been updated. Advantage: The consolidation entries thus generated under Capital are booked using the correct column format, i.e. they are booked in the equity ageing report with the correct booking code for the column in question. .

The booking statement looks like this:

Screenshot: KONBUCH, entries for the direct minority interests in respect of a foreign currency company

Here too, the structure utilises accounting record numbers, similar to the statement above. In addition, the pro-rata exchange rate effect (historic value versus computation date value) is determined in respect of each capital account. The conversion difference is booked separately on the capital account using BSL33 (elimination of currency conversion effects). The offsetting entry is made in the "Conversion difference, cumulative balance" from the currency conversion header of the consolidated company (see also WUME application).

Thus, only the value converted using the exchange rate on the computation date is posted to the "Minority interest - adjustment items" account.

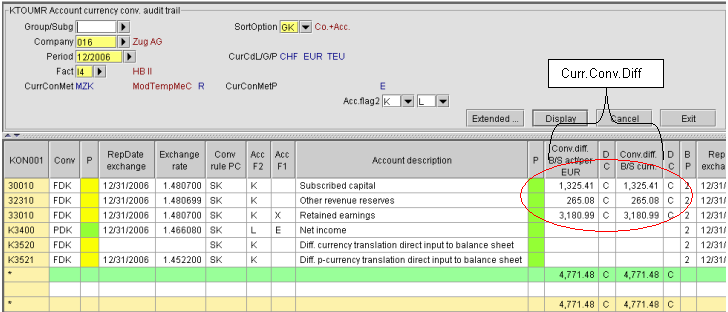

The calculation of the currency differences is based on the WUM application (in this regard, see also the relevant documentation). In order to verify the specific currency conversion effects on each account, we also recommend reconciliation with the account conversion verification in the application KTOUMR (see next screenshot). The system scans the individual currency differences from this application.

Screenshot: Account conversion verification

Example using the capital account "Subscribed capital":

Screenshot: Direct minority interests in the follow-on period in the case of a foreign currency company

The carrying-forward procedure for a foreign currency company is identical to that of company 006, with one exception:

And what does the minority interest statement for the current period now look like?

Screenshot: Calculation of the direct minority interest during the current period (foreign currency company)

Once again, the statement is divided into two sections:

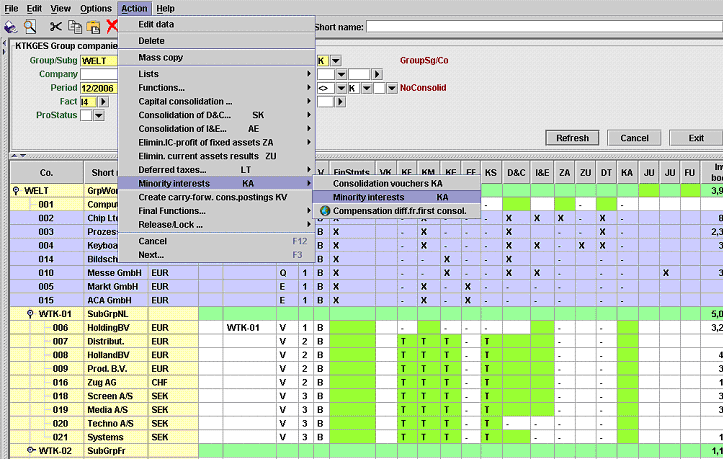

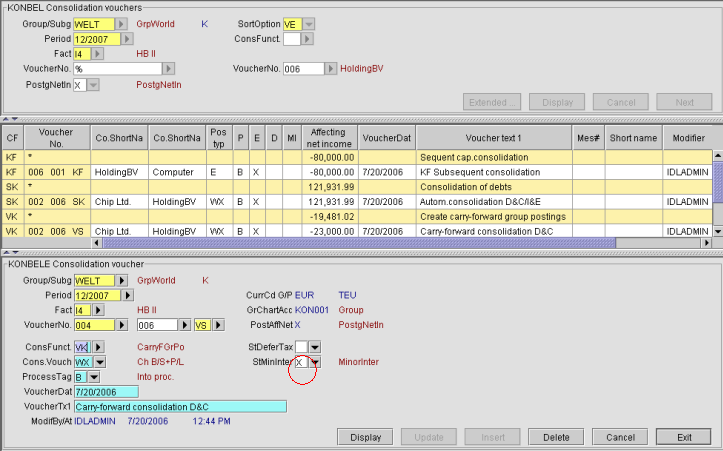

Before triggering the minority interest calculation, the "Consolidation statements for KA" can be used to determine the operative consolidation entries, if any, in which the third parties should participate. Therefore, the calculation of minority interests should be triggered after all other consolidation processing steps.

Example: If, starting with company 006, you right-click "Minority interests", and then "Consolidation statements for KA", the following overview will appear:

Screenshot: KONBEL with all consolidation statements with an impact on earnings for company 006

By highlighting a line and right-clicking 'Edit', you can specify whether the minority interests are to be included in these consolidation bookings in respect of the statement in question.

Screenshot: KONBEL, highlighting to make a selection for minority interest calculation

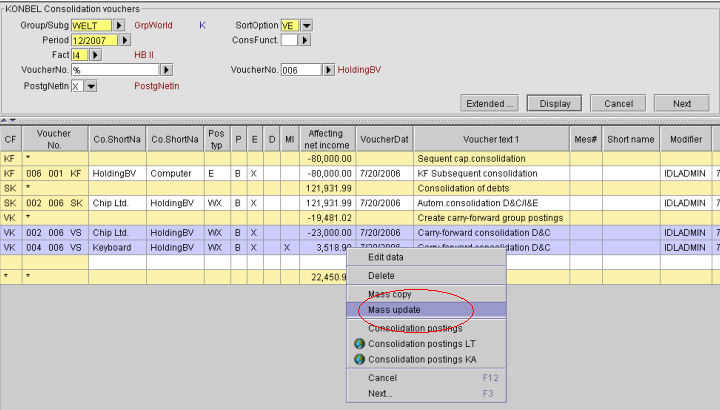

Alternatively, you can use the 'mass update' function. After highlighting the statements to be included, this function can be triggered by right-clicking. All highlighted statements will then be process in one step.

Screenshot: KONBEL, using 'mass update' to highlight a selection for the minority interest calculation

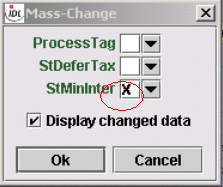

Screenshot: 'mass update' for the "KA Status"

If items in the statement headers are highlighted as described above, all operative entries are included in the minority interest calculation. If individual entries within a statement are not to be included, the relevant KA entry can be removed from the corresponding entry line in the accounting statement.

Screenshot: Entry line in "KA-Status"

The accounting statement can be accessed by highlighting the line and clicking "Edit". There, the entry highlighted and stored in the statement header can be selectively removed.

Screenshot: "KA" accounting statement entry

Alternatively, if several entries need to be edited, you can use 'mass update' to trigger batch processing.

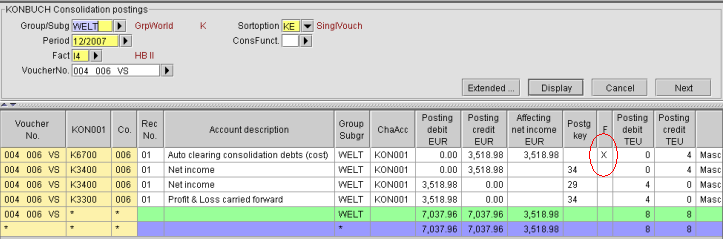

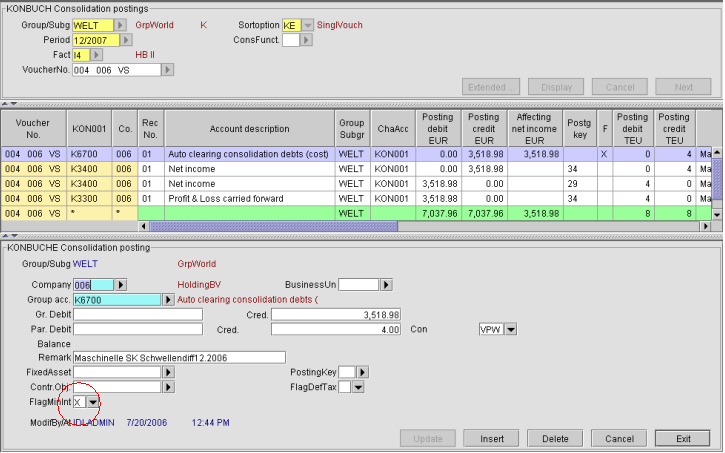

If, after highlighting individual statements, the calculation of minority interests is triggered, the minority interest statement in respect of the above example will be expanded as follows:

The consolidation's effect on the result was EUR 3,518.98. Of this, the minority interest shareholder is entitled to a share of 20%, or EUR 703.80. Since the consolidation involved an expenditure booking, the minority interest shareholder's share must fall; the adjustment item should therefore be booked as a debit item.

Screenshot: Minority interest statement incorporating a consolidation booking

The highlighted consolidation measures are entered in the minority interest statement using accounting record number 09. The correction of the minority interest share in net profit is controlled in the account in accordance with the information in the KTKPARKA, in the "Elimination of operative booking" field. The offsetting entry is made in the "Minority interest shares" account.

No currency conversion effects are included in these consolidation entries, since the original consolidation entries charged to income already exist in the group currency.

In the same way in which minority interests are entered to all entries charged to income, minority interests can now also be generated in respect of all entries which - in addition to the capital consolidation - relate to the equity of the company in question.

For this purpose, the key for operative consolidation statements (KONBEL) was extended to include one more attribute, 'K'. 'X' is assigned as before, if the statement has an operative effect on the result. 'K', however, is automatically assigned if the statement includes entries on capital accounts, without this involving a capital consolidation statement (consolidation processing 'Kx', 'Ex') .

The subsequent "Consolidation statements for KA" request from the group circle monitor (KTKGES) will no longer set the impact on earnings to 'X', but to '%'. If '%' is indicated, the consolidation statements (KONBEL) overview will select not only the statements with 'X' impact on earnings, but also those with 'K' impact on earnings. In the individual data set application (KONBELE), not only the statements with an impact on earnings = 'X', but also those with an impact on earnings = 'K', can be tagged with the KA key. In the latter case, however, it is not the entries in the profit-and-loss accounts, but rather those in the capital accounts that are tagged with the KA key .

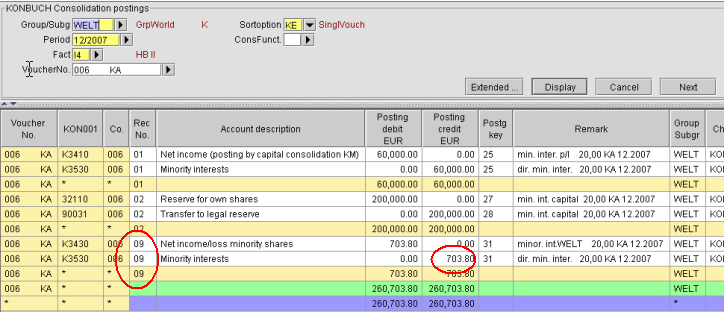

When booking the minority interests, all entries tagged with the KA key are processed. In contrast to the previous procedure of selecting and highlighting the entries on the profit-and-loss accounts, elimination in the capital account is carried out directly on the account. These entries are entered using the same accounting record number (BN 09) as those entered in respect of statements with an impact on earnings. Example:

On principle, it is also possible for currency differences to exist in the shareholdings of a foreign currency company, resulting from the difference between the shareholding's historic group currency value and the shareholding's group currency value in respect of the exchange rate pertaining on the computation date. These sums are also taken into consideration, in a pro-rata manner, using accounting record number 02.

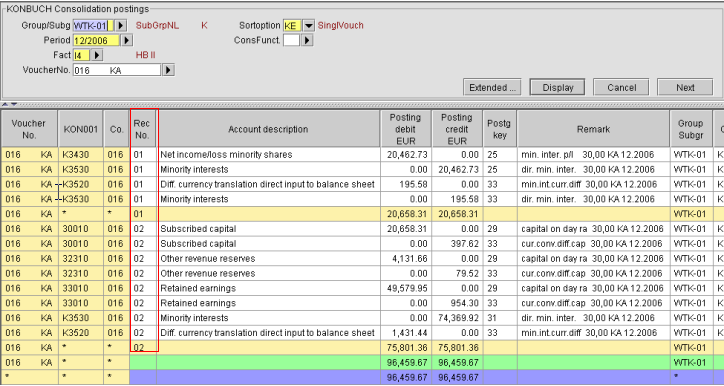

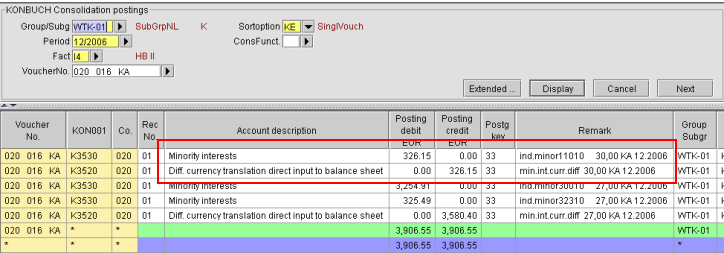

Example: company 016 (30% minority interest shareholder) owns company 020. Both companies have different non-Euro currencies (Swiss Francs, Swedish Kroner). After triggering the minority interest calculation for Company 020, the following booking is entered on the statement using two company numbers:

Screenshot: Entering the currency differences with respect to holdings

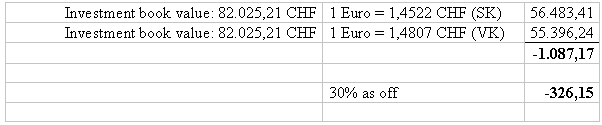

A corrective entry is made reflecting the level of the minority interest holding in 016. The amount is determined as follows: The parent company has a investment book value of CHF 82,025.21. Converted using the exchange rate on the computation date (SK), this results in the figure shown below. This is compared with the historic value recorded at the time of initial consolidation for the purpose of converting the holding (VK). Based on the resulting currency difference in respect of the investment (reflected in the adjustment item for currency differences in the individual annual accounts of 016), 30% is now calculated (minority interest in the parent company).

The corrective entry is carried out in a manner similar to the other currency differences; in this case "Minority interest adjustment items" to "Currency conversion adjustment items".

The currency difference in respect of holdings in companies to be consolidated is depicted for each parent company, line of business and participation account, and reduced by the minority interest in the parent company. Consolidation entries carried forward relating to the currency difference in respect of the investment are cancelled during the current period, and a new exchange rate effect is determined between the historic group conversion and the actual exchange rate on the computation date.

Starting situation:

Pre-conditions for a correct minority interest calculation:

Due to the 10% change, the following statement will be created after re-determining the minority interest during the current period, .

Screenshot: Determining the direct minority interest in the current period following a percentage change to the minority interest

The change to the minority interests will be included in a separate accounting record number (BN) 03:

The system carries out the following steps to facilitate this depiction:

In the case of foreign currency companies, the type of depiction is identical to the above, with the addition of the adjustment item from the currency conversion.

Starting situation:

Pre-conditions for a correct minority interest calculation:

In the current period, based on the new capital movement (entered using BSL 07=capital increase), the following statement is created following a re-calculation of the minority interest.

Screenshot: Calculation of the direct minority interest in the current period, including the capital increase

The system carries out the following steps to facilitate this depiction:

The foreign currency companies are represented in the same way, but include the adjustment item from the currency conversion.

Starting situation:

Pre-conditions for a correct minority interest calculation:

During the current period, based on the 10% change, the following statement will be created following the re-calculation of the minority interest.

Screenshot: Calculation of the direct minority interest in the current period given a percentage change to the minority interest and a change in the KAPBEW

The change in the minority interests is taken into account in a separate accounting record number (BN) 03:

System execution of the calculation is identical to the process described in the two previous chapters.

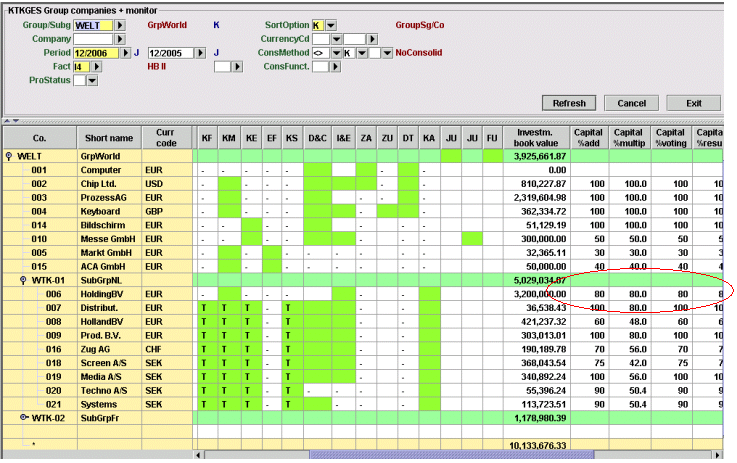

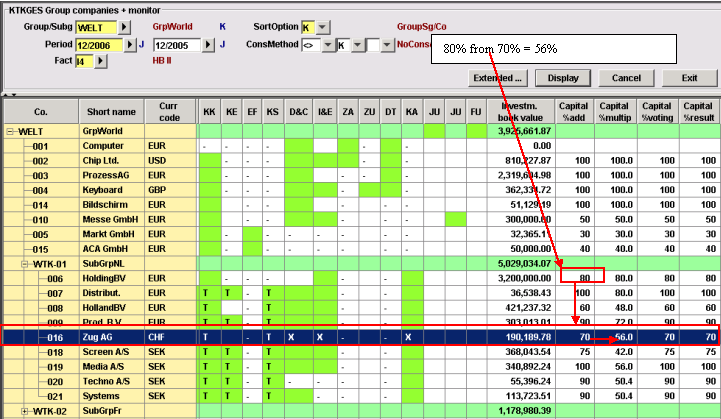

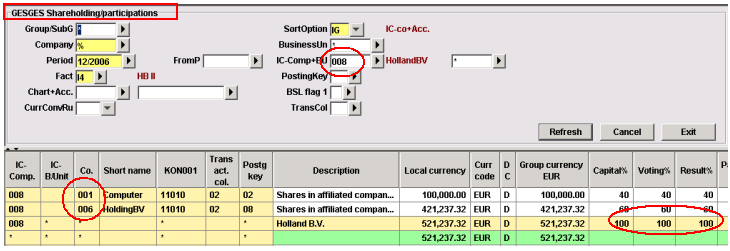

Indirect minority interest exists in a company if its parent company is also not owned by the Group at 100%. Multiplication and addition of the interest percentages, starting with the parent company, result in the multiplicative interest percentage recorded in KTKGES. The indirect minority interest represents the difference between additive and multiplicative interest percentages.

Example:

In our example, Company 016 (B) holds an additive interest percentage of 70%. Its parent company 006 (A) holds an additive and multiplicative interest percentage of 80%. This results for Company 016 in a multiplicative interest percentage of 70% x 80%=56%, as well as an indirect minority interest of 70% - 56% = 14%.

Screenshot: KTKGES

For the calculation of indirect minority interest, the system uses account balances and consolidation entries exclusively.

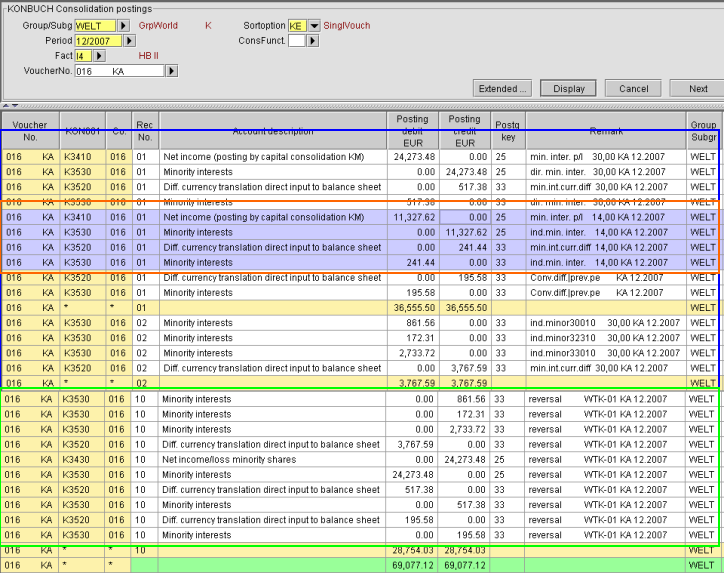

After the automatic minority interest has been assessed, the calculated result is shown in the following statement:

Screenshot: KONBUCH for indirect minority interests

Explanations concerning statement:

In case the status overview in KTKGES in column KA remains in yellow after processing has been triggered, check if any difference amount generated in secondary subgroups should be corrected.

In case any difference amounts (DA) have been generated and accounted for during capital consolidation (KK, KS and KF) in the secondary subgroup, this of course must be adjusted by the indirect minority interest in the primary group in which these indirect minorities participate. See the following example for Company 016:

Screenshot: KONBUCH for KK

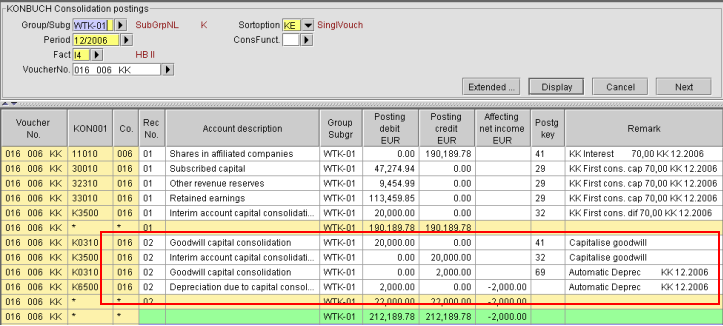

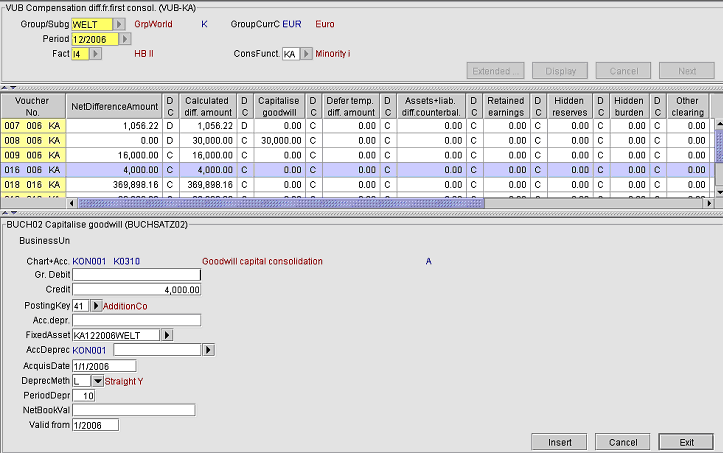

Example:The computerized capital consolidation determines a difference amount of EUR 20,000 and capitalized as goodwill. Depreciation is set linearly for 10 years (EUR 2,000 p.a.).

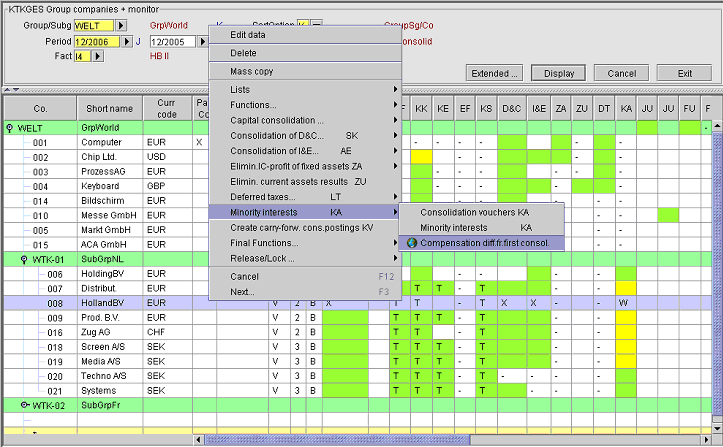

For the processing of indirect minority interests, a difference correction must be applied. Starting with KTKGES, use the right mouse button to pull up the "Minority Interests...KA" menu, then click the "Accounting for Difference Amount" application.

Screenshot: Menu in "Accounting for Difference Amount"

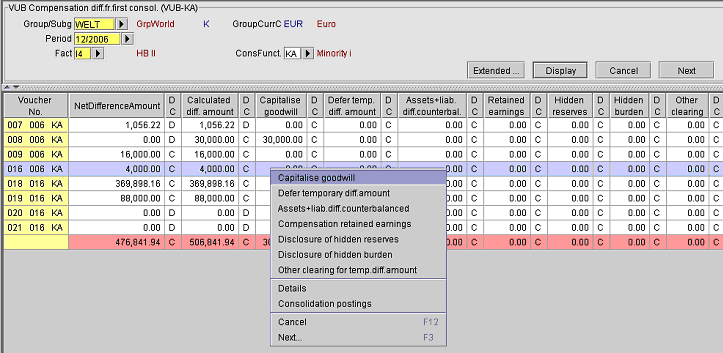

Analogous to capital consolidation, the correction window opens, to allow for specification as to how the pro-rated difference amount is to be adjusted.

Screenshot: Correction of pro-rated difference amount

Since the difference amount was capitalized and depreciated in the secondary subgroup, select "Capitalize Goodwill".

Screenshot: Capitalization of pro-rated DA

Analogous to capital consolidation, depreciation type and duration are entered here. The investment object is automatically generated and receives the suffix "KA" to indicate the calculation of minority interests. Care should be taken to ensure that depreciation type and duration correspond to those selected for goodwill in the secondary group.

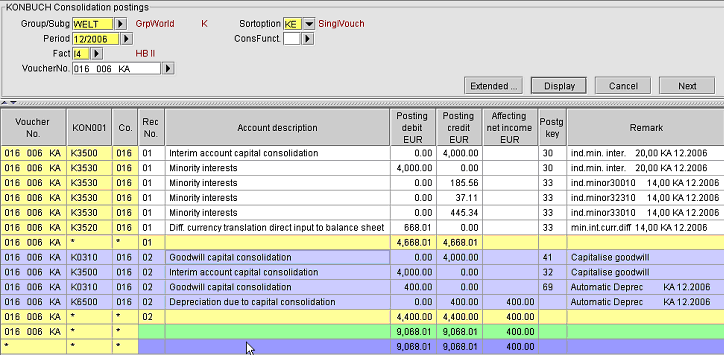

Screenshot: Correction statement for pro-rated DAs

The thus generated statement comprises 2 companies (016__006__KA). Under accounting record number 01, corrections are made for both, the pro-rated difference amount and the effect of prices on capital accounts. Under accounting record number 02, corrections are made to the pro-rated depreciation of goodwill. (The annual surplus, as described above, has already been corrected in the individual company statement.)

The carry-forward is determined per individual statement generated.

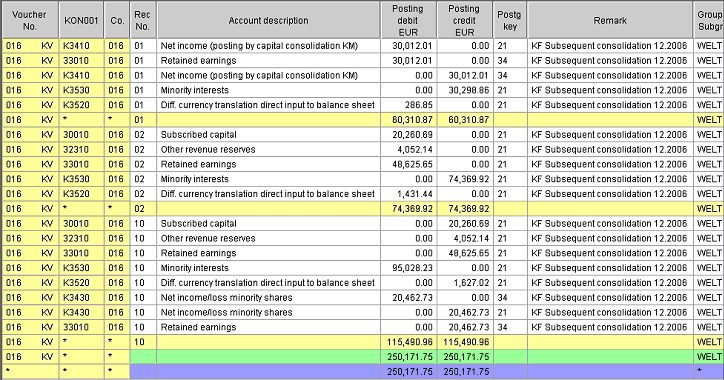

Screenshot: Carry-forward for statement 016__KA

The statement reflects a consolidation of accounts per accounting record number. The current share of indirect minority interest holders is recorded in a newly generated KA statement.

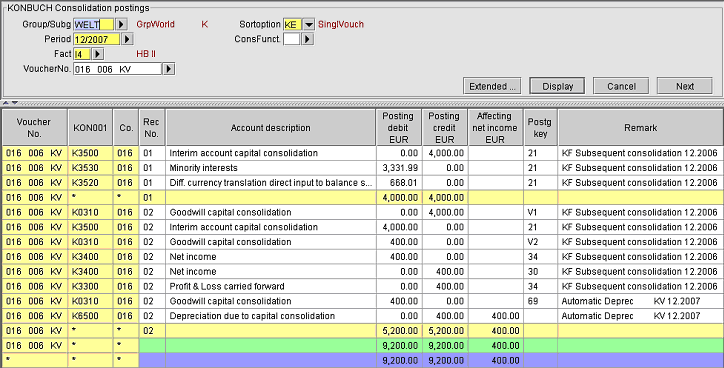

Screenshot: Carry-forward for statement 016__006__KA

A consolidation of accounts per accounting record number also takes place here. A new statement "016 006 KA" is generated if currency exchange fluctuations and/or changes in the underlying capital consolidation occur.

The carry-forward logic is equivalent to that of capital consolidation.

In the single set application KTKGESE, the code "(WithoutIndMI)" = Without indirect minority interests can be used to control whether or not indirect minority interests should be calculated for any given company.

Screenshot: Turning off calculation of indirect minority interests in KTKGES

Using the group monitor, the companies without indirect minority interest calculation are marked with an 'X' in the column with header 'F'.

Screenshot: KTKGES Turning off indirect minority interest calculation

If, following this entry, the calculation of minority interests is triggered, the statements of the direct minority interest owners from the secondary group will simply be copied and cancelled in the primary group (Global in this case) in which these indirect minority interest owners should not be included (see Explanation on indirect minority interests). No further booking takes place.

Screenshot: Statement after turning off indirect minority interest calculation

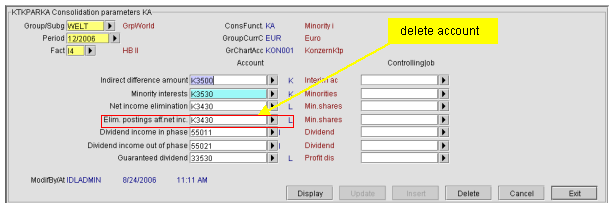

The elimination of minority interests on the annual surplus can be suppressed , by leaving out the account information for "Elimination of Annual Surplus / Deficit Amount (E)" in the KTKPARKA consolidation parameter. This then applies to all minority interest companies within this group/subgroup.

Screenshot: Changing entry in KTKPARKA

If minority interests are now calculated, only the individual capital items without annual surplus / deficit are accounted in the adjustment items for minority interests. Accounting record number 01 remains unused.

Screenshot: Minority interest statement without annual surplus share of minority interests

Optionally, the same effect may be achieved in treating share ownership by entering the share to which the holding company is entitled in field "Yield%". This would be 100%, for example, if minority interests are not to partake in the annual surplus.

Screenshot: Entry in share ownership; group share in yield: 100%

Upon recalculation of the minority interests, a statement similar to the above screenshot would be generated.

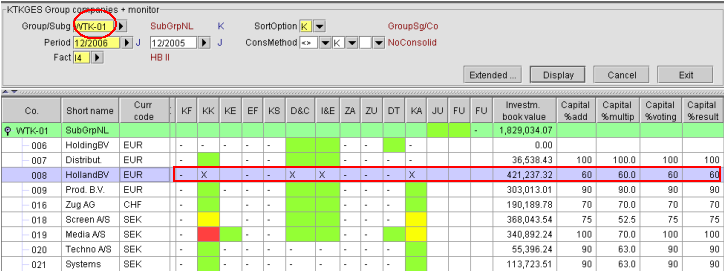

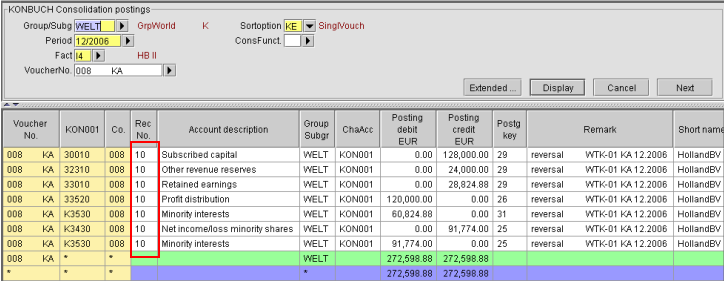

In case a group structure exists in which, from a subgroup perspective but not from the overall group perspective, minority interests exist, initiation of IDL KONSIS issues, after triggering the "Calculation of Minority Interests" process, a cancellation statement for the primary group which cancels the posting of all minority interests of the secondary group.

Example: Company 006 holds a 60% interest in Company 008 of the subgroup. The remaining 40% are held by the primary parent company 001. From the overall group?s perspective, there are no additional minority interests. The statement originating from the secondary group must therefore be cancelled.

Screenshot: Summary: 60% interest in subgroup, and 100% interest in global group

Screenshot: Posting in Subgroup

The cancellation statement is posted under accounting record number 10.

Screenshot: Cancellation posting in primary group

The posting text in the cancellation statement specifies the subgroup to which the cancellation applies. If a statement exists in the secondary group with two company keys included in the statement number, these would likewise be cancelled under the two-digit statement number.

Profit distributions by one company, and profit receipt by another company can be divided into two types of payout and receipt, leading to a different treatment of minority interests.

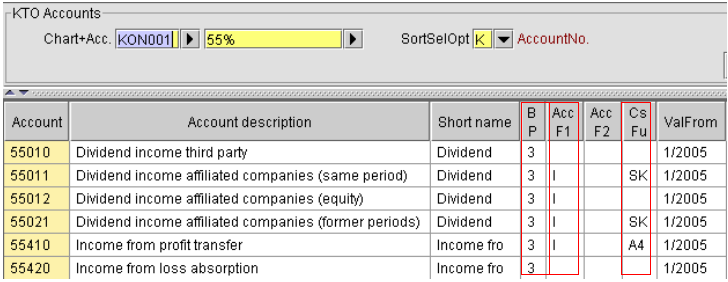

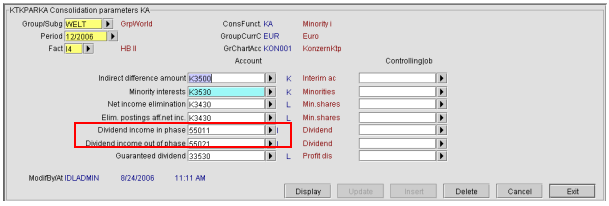

To allow for an automatic consideration of profit distributions, separate "Dividend Yield (in-phase)" and "Dividend Yield (out-of-phase)? accounts must be provided in the KTKPARKA as Yield Account, Inter-Company Account and Consolidation Processing = SK.

Screenshot: Dividend Yield Accounts in KTO

Screenshot: KTKPARKA with entry of dividend yield account (in-phase/out-of-phase)

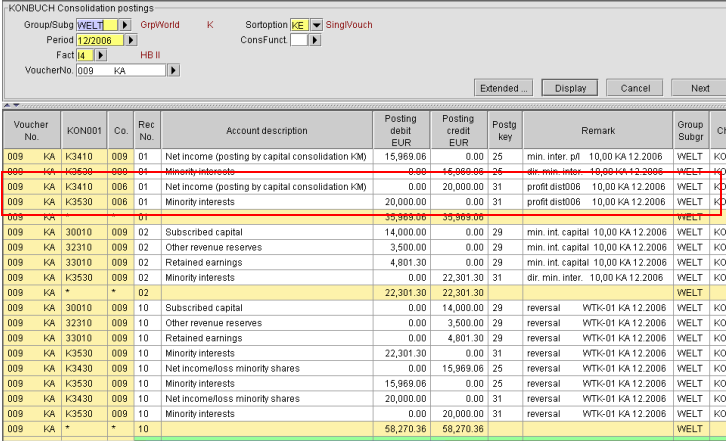

Example: Company 006 holds an interest of 90% in Company 009. Company 006 discloses in account 55011 a profit payout in the amount of EUR 200,000.00 in favor of Company 009. After the minority interest calculation for Company 009 has been triggered, the statement looks as follows:

Aside from accounting for the pro-rated annual surplus in BN01, the statement also reflects a corrective entry in the amount of 10% (direct interest) on the in-phase payout made to Company 006 of EUR 200,000 (resulting in EUR 20,000). This correction is made because the annual surplus of the distributing company (here Company 009) has not been reduced yet, and therefore the minority interest holders would have been accommodated by an excessive amount (basis for the minority interest calculation is the annual surplus not yet reduced by the payout, since in-phase).

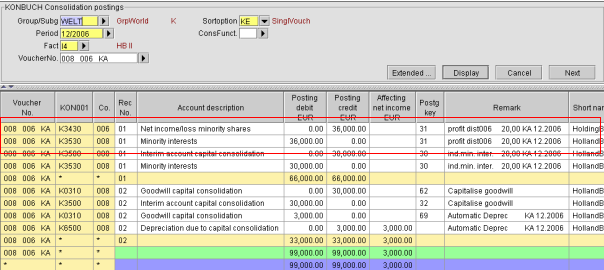

Example: Company 006 holds an interest of 60% in Company 008. In account 55021, company 006 discloses a profit payout in the amount of EUR 180,000.00 in favor of Company 008. Company 006 is also the parent company of 008. There are direct and indirect minority interests in Company 008 through the minority interests in 006. After initiating the minority interest calculation for Company 008, the statement looks as follows:

For out-of-phase profit distributions, all entries are listed in statements with two companies as part of the statement number. The second company is always the IC balance-keeping company.

Aside from recording the pro-rated business and company asset in this statement, accounting record number 01 also corrects for the distribution amount to which the direct minority interest holders in the parent company are entitled (20% of EUR 180,000 = EUR 36,000). This correction is necessary in order to avoid a duplicate consideration of minority interests in profit distributions, i.e., once through distribution from 008 to 006, and secondly through the increased annual surplus of the receiving company (006).

The calculation of minority interests is based on IC account balances for those accounts which list the consolidating company as the IC company. The entry is made from account "Minority Interest - Annual Surplus" to account "Minority Interest - Adjustment Items".

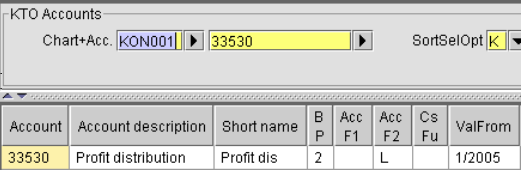

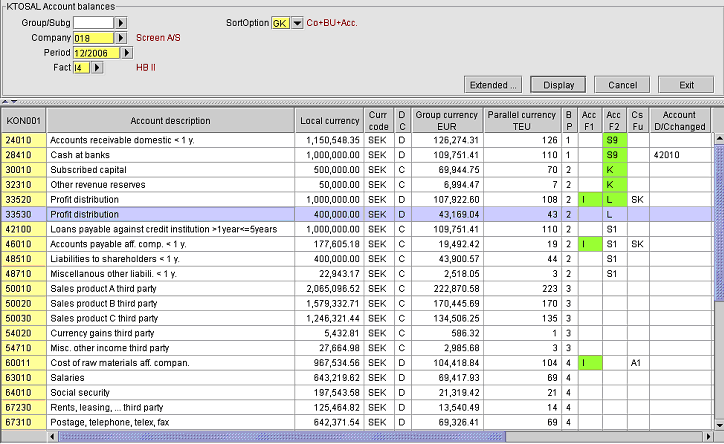

In case the minority interest in the annual result is specified by contract as a fixed amount (guaranteed dividend), said minority interest in the annual result shall not be calculated as a percentage of the annual surplus/deficit but with the fixed amount of the guaranteed dividend. Said amount shall be treated as a balance in the respective account (application "KTOSAL") for the company which promises a guaranteed dividend to the minority interest holders.

Since this is a user account subject to the annual result, this account must have account code 2 equal to "L".

Screenshot: Account master record for guaranteed dividend account

Screenshot: Account balance for guaranteed dividend account

In the above example, the minority interest holders would not receive 25% of the annual result in the amount of EUR 151,091.64 (= EUR 37,772.,91) but instead would receive the balance in the guaranteed dividend account 33530 in the amount of EUR 43,169.04.

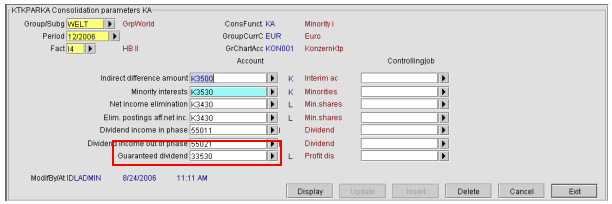

The prerequisite for computerized control is that for the calculation of minority interests the guaranteed dividend account is in fact entered in this very field in the KTKPAR set.

Screenshot: KTKPARKK with entry of a guaranteed dividend account

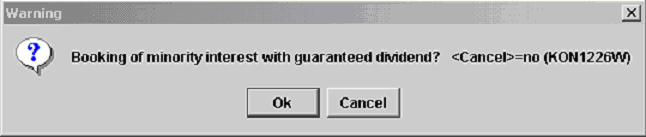

If the "Calculation of Minority Interests" process is now triggered in KTKGES for Company 018, the following message window appears:

Screenshot: Message after triggering minority interest calculation

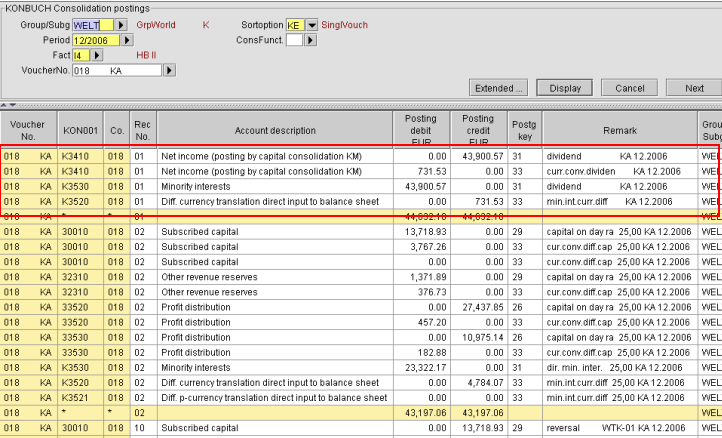

Screenshot: Entry statement upon confirmation with "OK" (with guaranteed dividend)

In the above example, the amount of the guaranteed dividend (EUR 43,900.57 - EUR 731.51 = EUR 43,169.04) is entered in accounting record number 01 with the corresponding price difference. The price difference results from the difference between period average and cutoff date prices.

Calculation of price difference:

Screenshot: Calculation of price difference

The consolidation entry is made in account "Minority Interest - Annual Surplus", the counter entry is made in account "Minority Interest - Adjustment Items".

In case the guaranteed dividend account shows a zero balance for the company accounts and calculation of minority interest with guaranteed dividend is selected with "OK", a value of zero would be taken into account. If you click "Cancel", the pro-rated annual result would be calculated and assigned to the minority interests.