For the consolidation of equity com panies you need three consolidation parameters for each subgroup, period and fact:

The parameters have to be defined only once. In the following years they are carried forward within the group carry-forward. For being able to present several per iods it is necessary to also enter the parameters in the previous period before starting the equity consolidation.

An account must only be defined once in all three parameters, otherwise the values cannot be prepared correctly.

Sig nification of the individual accounts:

[Difference amount]: The account for the differe nce amount is used for posting the difference amount determined in the capital consolidation. Here it is irrelevant whether the summation of the investment book value and the prorated capital results in an active or passive difference amount. This fiel d allows only assets or liability accounts (B/S, P+L-flag. = 1 or 2) with the account flag 'T' = difference amount.

[Capitalise goodwill]: In case the investment book value and the prorated capital are summed up to an active difference amount, it might, among other possibilities, be capitalised as goodwill. In IDL Konsis you require a separate a ccount for posting this process. This field allows only assets accounts (B/S, P+L-flag = 1) with the account flag 2=A (fixed ass ets account)

[Compensation difference amount in local currency]: According to IFRS goodwill, w hich is created by the consolidation of foreign companies, has to be capitalised in their local currency and adjusted in the sub sequent years according to the market trend. Equally it is possible to capitalise an emerging goodwill with another, third c ompany. If you want to use this functionality, you need to enter an account in this field, which is used as clearing account in order to adjust the individual vouchers at the different companies. You have to enter a capital account in this field. For f urther information about Reverse goodwill IFRS, in particular about the possibility of posting currency conversion differences, please see chapter Goodwill local currency in the GUIDE Capital consolidation

[Clearing badwill]: If a badwill remains, it can be posted with the corresponding action in the application <Compensation diff.fr.first consol.(VUB)> to the account entered here. Different from the consolidation parameter (KK ) for fully consolidated companies, here you can enter a fixed assets account, because a negative goodwill is accounted for on the asset side within the "Investment associated company". In order to be able to display this position in the development fi xed assets, the account has to be defined as a fixed assets account.

[Retained earnings clearing] : If you want to compensate a difference amount, which remains after detecting hidden reserves, without affecting net inc ome, you use this account.

[Depreciations]: Fixed assets objects resulting from the capital co nsolidation of equity companies are depreciated via this account.

[Depreciations goodwill]: If you want to post depreciations for goodwill on another account than the one mentioned above, you have to enter this one.

[Depreciations participation]: If the participation is depreciated in the parent company, you ha ve to eliminate this depreciation with a consolidation posting. If you enter the depreciation account in this field, the pos ting is automatically performed contra this account.

[Currency conversion effect participation]: If there are participations in a foreign currency, each period creates currency conversion differences. If those are to be el iminated via the capital consolidation, you need to enter the respective account in this field.

[ Currency conversion participations]: If participations are held by a foreign holding company, the currency conversion wil l produce differences in each period. If those are to be eliminated via the capital consolidation, you need to enter the respect ive account in this field

[Reposting participation]: For at Equity companies the respective pa rticipation from the group view has to be recorded as investment in associated companies. The usually separately created account has to be entered here.

[Carry-forward]: Postings affecting net income from the equity co nsolidation are reposted to this account during the carry-forward. We recommend the use of a separate account, which differs from the companies+ financial statement and from the statement/II. In this field you can only enter a liability account.

[Accounts for neutralisation]: If effects from postings between holding and subsidiary have to be ne utralised, two separate accounts (allocated to fixed assets) have to be entered here.

The consolid ation parameter EF is used for the update of Equity companies. You have to define it for each subgroup, period and fact. During the group carry-forward it is carried forward to the subsequent periods. Just like the EK parameter this parameter has also to be created in the previous period before starting the equity consolidation.

Signification of the i ndividual accounts:

[Prorated net income]: On this P/L-account is posted the prorated n et income of the subsidiary.

[Prorated net loss]: If you want to post the prorated net loss to a separate account, you need to enter it in this field. Otherwise both net income and loss are posted together on the previous account.

[Effect for elimination of IC-profit]: If the equity company sells fixed assets, thus creating IC-profits, these have to be eliminated. For these cases you can enter a separate P+L account in this field.

[Deferred taxes on IC-profits]: The deferred taxes on the above mentioned IC-profits have to be pos ted via this P+L account.

[Collected dividend]: This field is provided for the account the parent company posts the shareholding results of equity companies to. It has to be an intercompany account with the respective IC details. If one period contains an account balance, it is cancelled with the update equity consolidation and the investme nt book value is reduced accordingly.

[Dissolution diff. amount as liability]: A difference am ount of liabilities can only be dissolved via this account. An entry into the data entry sheet produces a posting on the account "Defer temporary diff. amount" from the EK parameter.

[Impairment / Appreciation goodwill]: At this point the account for the goodwill is copied and displayed by the parameter EK. In this field you need to enter the p osting keys for the (manual) posting of the impairment or the appreciation goodwill on this account.

[Impairment / Appreciation of hidden reserves]: Here, too, you only need to enter the posting keys for the manual posting of the impairment or the appreciation of hidden reserves.

[Currency translation effect goodwill] : If a foreign company creates goodwill there may emerge currency conversion differences. If those are to be posted via t he Update equity, you need to enter a respective account in this field.

[Currency translation eff ect capital / income]: Equally currency translation effects can be generated in the capital and in particular in the inco me, for which you can enter accounts in this field.

[Other income / expenses]: For other incom e / expenses affecting net income, which do not belong to the items mentioned above, you have to enter P+L accounts (required fi elds).

[Corporate action]: In case of capital transactions in a subsidiary, which cannot be al located in the shareholding/participations and thus cannot be eliminated with the first consolidation, they can be included with this account.

[Necessary adjustments revaluation reserves]: If the capital in the equity company changes through facts not affecting net income, in particular by, e.g., generating and changing the adjustment revaluati on reserves, these changes have to be reflected in the book value of the equity participations. In these fields you have to enter the corresponding accounts for these facts.

The EH parameter is also used for the update equ ity consolidation, especially if a negative book value has to be adjusted to 0,00.

Signification of the individual accounts:

[Devaluation of postulation]: If a negative book value has to be adjusted in form of a devaluation of postulation, enter the account here

[Accumulation of r eserves]: If a reserve hast to be build as correction of the negative book value the respective account has to be entered here

[Clearing of changes net income]:

[Clearing of changes no t net income]:

Moreover you need a valid data record in the shareholdings for the first consolidation of an equity company. For this purpose you can use the same posting keys you use for the full and quota consolidations. With a ll posting keys for addition you can either perform the manual or the automatic consolidation. With the equity companies you will almost never use the automatic one, because it requires the account balances and sometimes the capital transactions of the company.

The capital consolidation requires the following posting keys:

[BSL 02 = A ddition of participation]: In case of transactions with this posting key you have to enter a local currency value and inv estment capital percentages. The transaction can be processed using either the manual or the automatic capital consolidation. If the subsidiary shows capital transactions, they have to be prorated up to the transaction date of the addition for the cons olidation. Here addition posting keys are used for the consolidation postings on fixed assets accounts.

[BSL 04 = Setting for begin of period]: First of all this posting key is used at the first implementation of IDL Konsis. Here carry-forward keys are used for the consolidation postings on fixed assets accounts.

[BSL 05 und 0 7 = Allowances and accumulated allowances]: If the KTKPAREK contains an account for "Depreciation participations", shareholding transactions with this posting key are automatically posted. With posting key = 05, allowances, directly on this account, and with posting key 07 = accumulated allowances on the carry forward account.

[BSL 08 = Addition of capital]: Unlike the shareholding addition you only need to enter a local currency value and if necessary a group currency value for the addition of capital and you do not have to enter investment capital percentages. If the equity com pany has account balances and capital transactions, the shareholdings/participations are posted contra capital transactions (posting key '02') with the same transaction date.

[BSL 10 = Disposal of capital]: Equivalent to t he posting key 08 = capital increase here you only need to enter a local currency value without considering the fields for the i nvestment capital percentages. The processing is performed just as in the capital increase, with the exception that all post ings have a corresponding negative sign. The reduction entered in the shareholding/participations is posted contra (as far as ex isting) capital disposals (KAPBEW with posting key '03') with the same transaction data in a EK voucher.

In the subsequent years the company carry-forward includes the carry-forward of these transactions; only current transactions have to be updated. For further information about the topic shareholding/participations (GESGES) please see chapter Shareholding / participations (GESGES) in the GUIDE for transactions in companies 'financial statements'.

All co mpanies scheduled for a capital consolidation have to be allocated to the respective group companies. The following table displa ys the allocation of an at equity company to the group +world+. It is important to set the consolidation type to "E" for equity consolidation.

The first co nsolidation automatic or forms can be reached via the menu -> capital consolidation in the group companies + monitor. The aut omatic first consolidation is performed in the background and is rarely used for equity companies, because for a correct res ult it requires account balances or capital transactions. The function "first consolidation forms" leads to the formular I-ERSTK ON where the prorated capital can be filled in.

In the formular I-ERSTKON the investment book value is oppo sed to the prorated capital. The coloumn "comp.financ.stmts.Trans.devel." shows the considered capital transactions if avail able. Postings are shown in the coloumn "Group.financ.stmts.equ.ratio" and can be changed. New lines can be added by pressing EN TER in the last field of a line. Postings can be deleted by entering 0,00 in the concerning field.

The post ings are registered with the posting record number 01 in an EK voucher. It is particular about the EK voucher that the capital i s eliminated "for information only" and is again cancelled in the same voucher. The determined difference amount is posted o n the one hand and the difference between the original investment book value and the difference amount on the other hand. An eme rged difference amount is distributed by the application "Compensation diff.fr.first consol.".

For further information about the topic first consolidation please see GUIDE Capital consolidation

A red status in the column "EF" shows that the update equity consolida tion for a company has not yet been carried out. After performing the update the application creates an EF voucher and the s tatus is changed to green. If there is no current result for a certain period, you still have to open the application and enter the zero value into the line "prorated result". Then the application creates an EF voucher with two zero lines.

You open the forms data entry "Update equity consolidation" via the group companies + monitor via <Action> <Capital consolidation> <Update equity consolidation EF> or by double clicking in the column "EF" of the equity company. First you get to the application "FORTEQ", which displays the possible relations between parent company and subsidiaries (where required for different business areas). By double clicking once again on the desired company pair you o pen the actual forms data entry.

The forms data entry can not only display the current entry period, but al so up to 3 annual financial statement periods (code 'J' in the master record ABR) next to each other, whereas you can only e nter values in the current period. For this purpose you have to change the previous period according to the desired view in the tabel FORTEQ.

The form is structured dynamically in connection with KTKPAR. The more accounts are e ntered in the EF or EN parameter, the more lines are provided.

The sheet is subdivided into three entry and display areas:

[Transfer/Carry forward]: Basis for the sequent consolidation is the investmen t book value at the parent company. Usually the block is a display area, to which the actual modification or the clearing of a negative amount stated are copied from the previous period. The first period (for this subsidiary /parent company) does not y et contain a KF voucher, but you can enter a value in the line "other changes affecting net income", which is posted to the carry forward account according to KTKPAR.

[Actual modification]: The more accounts have been entered in KTKPAR EF, the more entry lines are displayed in this area. You have to enter the prorated values in group currency f rom the shareholding view (i.e. a net loss with a 'minus'). In "collected dividend" the application automatically displays t he amount of the account for income from investments in KTKPAR at the parent company opposite to this subsidiary (IC balance). T he thus resulting posting eliminates these incomes from investments and reduces the stake valuation. The lines "Depreciation/ impairment / appreciation goodwill or hidden reserves are to be considered particularly. You cannot enter these values, but t hey rather display those postings, which have been posted either automatically (e.g. continued depreciation) or manually (e.g.impairment) in a EK V or EK voucher.Another special block are the input lines with the suffix "manual". Here, accounts and po sting keys for the postings to be done can be freely entered directly in the line. If more thant one line per category is re quired, additional lines can be generated by pressing ENTER at the end of the respective line. The actual modifications can be e ntered en bloc. By clicking on <save> they are written in an EF voucher. Already posted amounts can be deleted by entering a zero value. All subtotals and total sums are immediately updated during the data entry.

[C learing of negative value]: If the actual modifications in the current period lead to a negative total sum , you have to clear the negative amount with the first part of this block until the total sum results in 0.00. Only positive values have to be entered here. A clearing carried forward from the previous period can be reopened by an entry in that part, in which the en try lines contain "unwind", provided that the actual modifications of the current period have changed to be positive again. Only negative values have to be entered here.

The following plausibilities are checked during the entry:

If the actual modifi cations result in a negative total sum, you have to enter such values in the lines for clearing of negative values, which lead t o an exact total sum of 0.00.

If the actual modifications are positive and the final value of the previ ous period was negative, you first have to restore the carried forward clearing measures in the lines "Clearing of negative value". The entries in these lines, however, must not exceed the original clearing value, but only have to result in the respect ive balance of 0.00, thus leading to a positive result of possible remaining actual modifications.

If t he total sum is positive both in the current and the previous period, you cannot enter any value in the last entry area. The sam e applies to negative actual modifications.

If one of these plausibilities is not adhered to, the entry can not be saved.

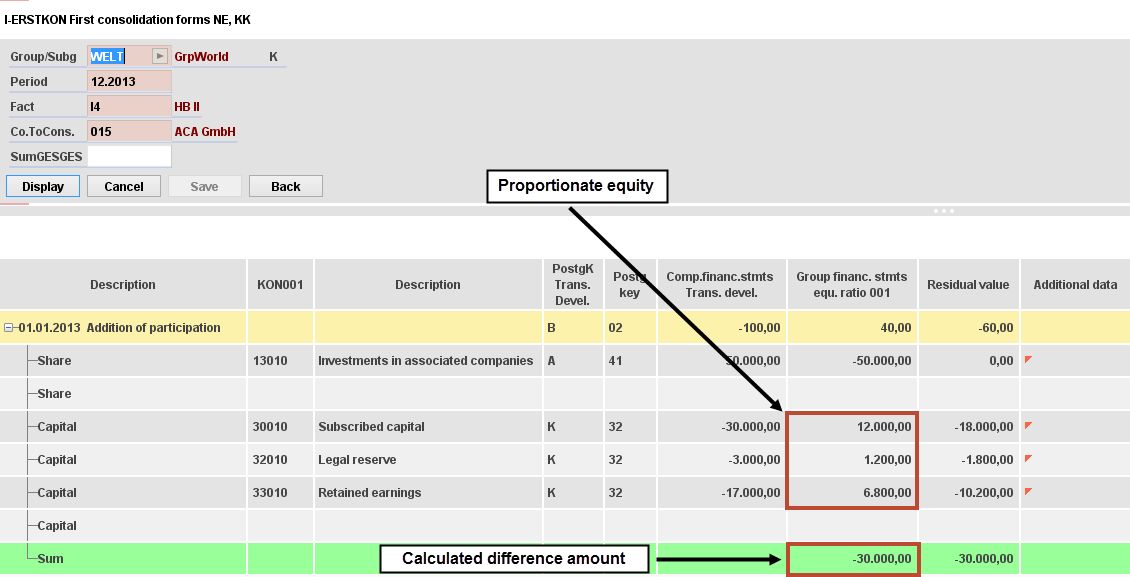

Company 001 holds 40 % of company 015 ,which were acquired on 01.01.21 for 50,000.00 Euro. The first inclusion to the consolidation financial statement with the at-equity method is planned for the financial year 2021 with the 01.01.21 being the date for the first consolidation. As from the 01.01.21 the capital of the associated company is s ubdivided as follows:

| 100% | pror.40% | |

|---|---|---|

| Capital stock | 30.000,00 | 12.000,00 |

| Revenue reserves by law | 3,000.00 | 1,200.00 |

| Carry forward | 17,000 .00 | 6,800.00 |

It is presumed that a possible goodwill, starting as from 2021, is linearly depreciated during 10 years. In the financial year 2021 the company has generated a net income of 20,000.00 Euro. In the following period the company 015 generates a net income of 30,000.00 Euro. In 2022 the parent company 00 1 obtains a dividend of Euro 5,000.00, which are contained in the account balances as shareholding results.

Our example contains the account balances for company 015. For display reasons, however, the first consolidation forms is presented here.

Figure: Clearing of the shareholding with the capital in the table I-ERSTKON

If the data for the first consolidation are correct and saved, you leave the application by clicking on "next" for getting back to KTKGES. The status has now changed to yellow, because a difference amount has been generated, which h as to be compensated via the action ->Capital consolidation ->Compensation difference from first consolidation.

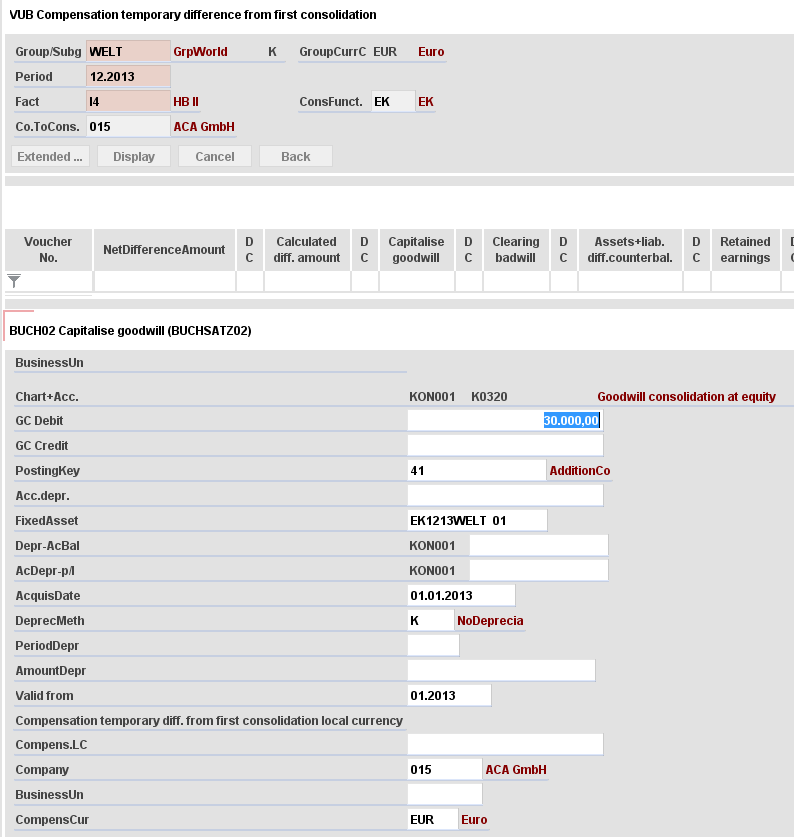

Capitalise goodwill

Via the application "Compensation diff.fr.first consol. VUB " you capitalise the generated difference amount as goodwill. According to the example the fixed asset is adjusted to a line ar depreciation during 10 years. Here you have to enter the 01.01.2021 as the date of acquisition, because the complete annual d epreciation has to be posted still in the same year. For further information about the application "VUB" please see GUIDE Compensation diff.fr.first consol.

Figure: Capitalisation of goodwill in the application VUB

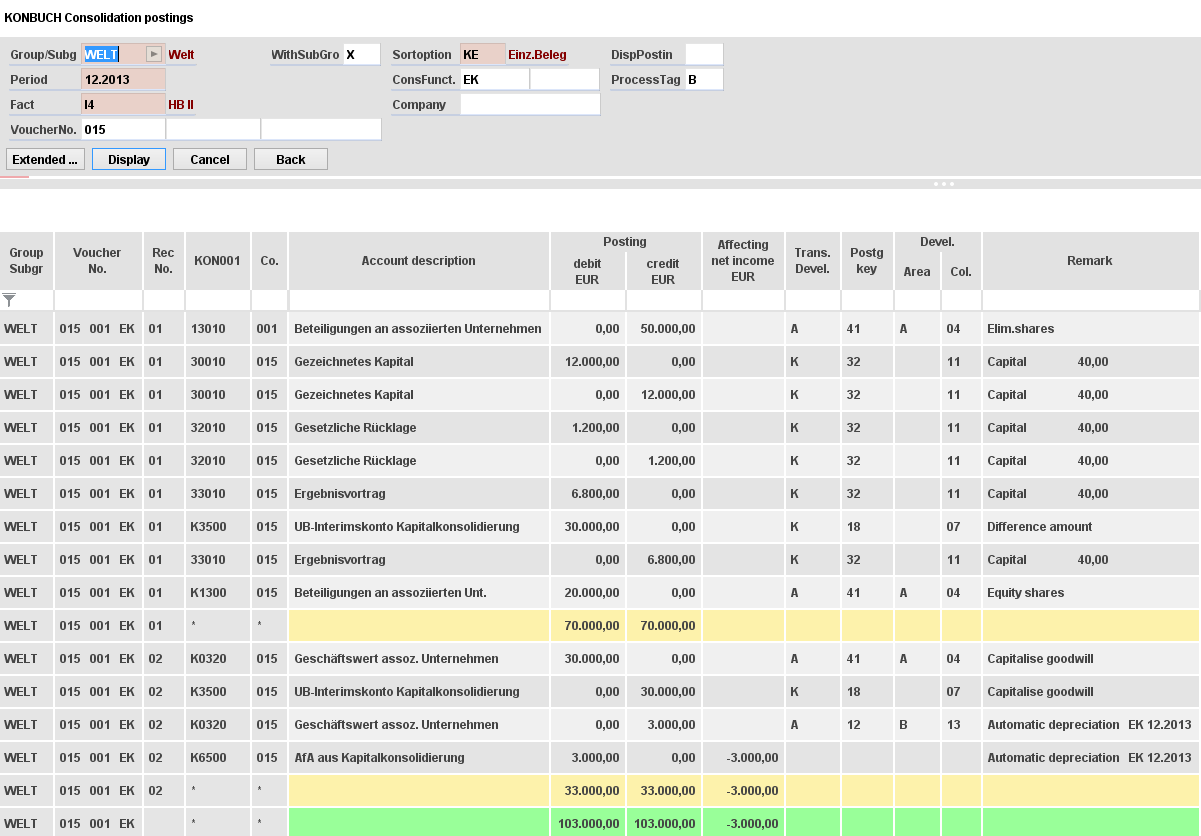

Herewith the fir st consolidation is completed, the status has changed to green and the voucher is complete. The following consolidation postings have been generated:

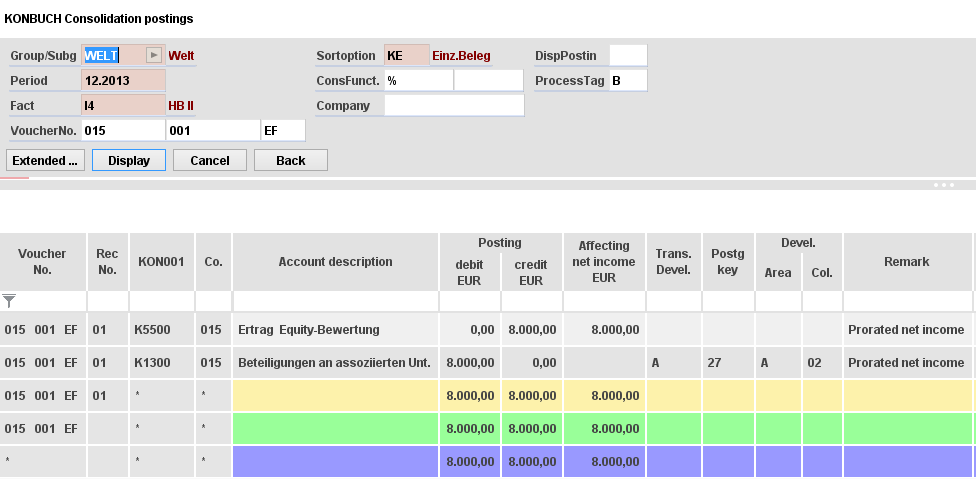

Figure: Cons olidation postings of the EK voucher

The capital is posted with the posting record no. 01 contra the invest ment book value and the difference amount is determined. It is particular about the EK voucher that it is eliminated for inf ormation only. The postings are cancelled again in the same voucher. On the one hand the difference amount and on the other hand the difference between the investment book value and the difference amount is posted, which is then posted to the account " Investment associated company" from KTKPAR.

The capitalisation of goodwill and the continued depreciation h ave been posted with the posting record no. 02. If you manually add postings, please keep the posting record no. system.

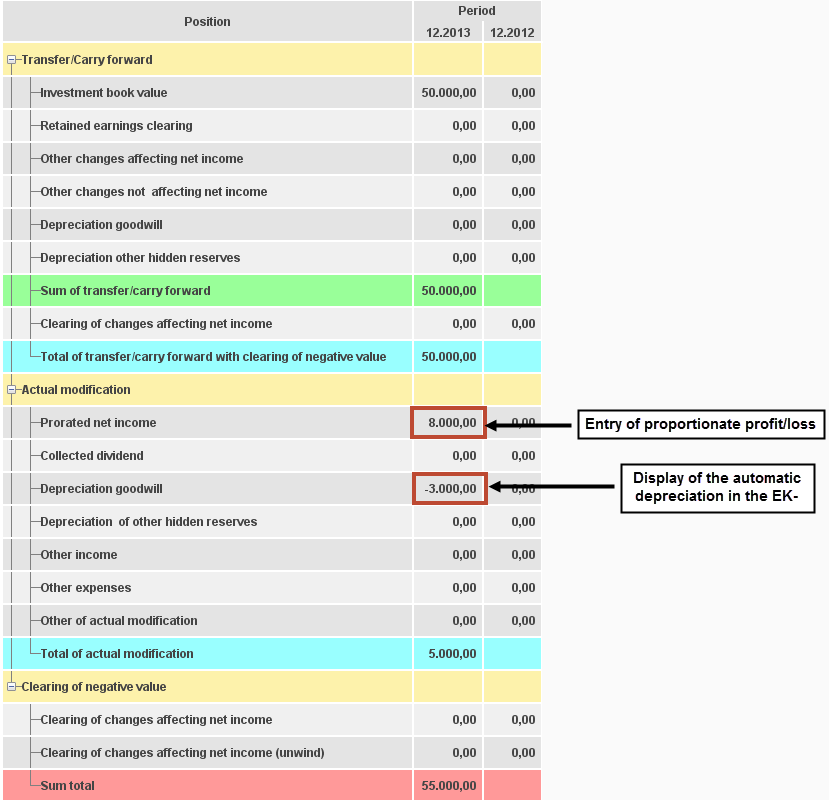

The investment book value of the equity company is changed in every period by the prorated annual result and the depreciation of the goodwill. The depreci ation is automatically posted in the EK or KF voucher, but for the prorated annual result you have to use a further function : The Update Equity within the capital consolidation (it can also be opened by double clicking on the column "EF").

At using the function you open the application "FORTEQ". By double clicking on the correct relation be tween parent company and subsidiary you open the application "I-FORTEQ", which at the same time is an overview and posting mask in the form of a forms data entry.

The goodwill depreciation, which has already been posted in the EK v oucher, is displayed at "depreciation goodwill". Now you only have to enter the 40% of the net income of 20,000 Euro = 8,000 Euro to the field "prorated net income" and save it.

Figure: The forms data entry for the Update equity EF

The entries have been posted in t he EF voucher as follows:

Figure: Consolidation postings of the EF voucher

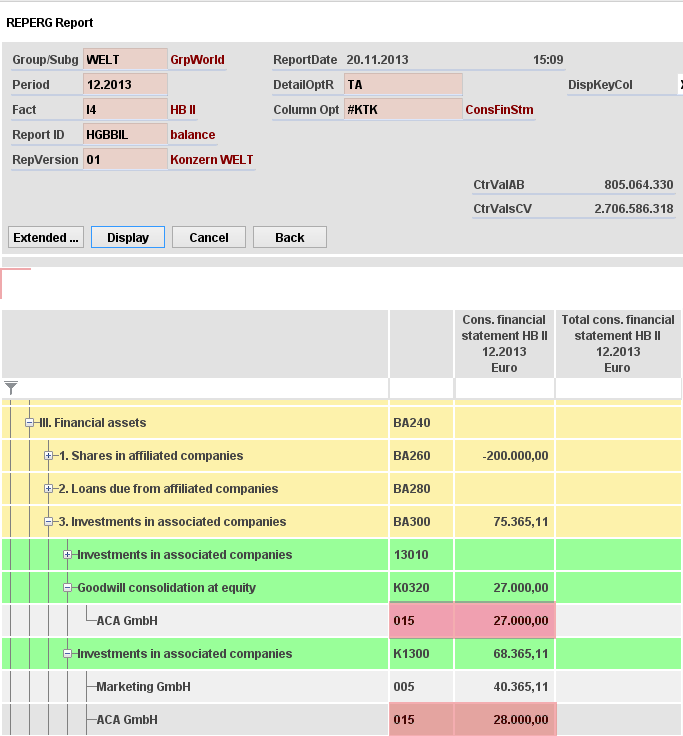

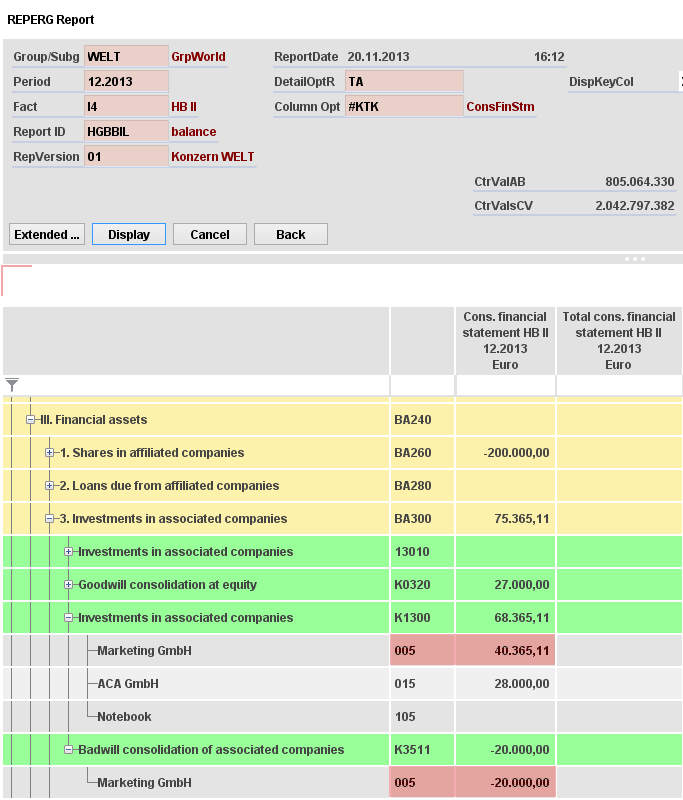

The individual partial amounts are summarized in the report as "Investment associated company".

Figure: Report for "Investment associated company"

With the group carr y forward the group structure and the posting vouchers are carried forward to 12/2022. In this context the EK and EF voucher are carried forward to a EK V voucher.

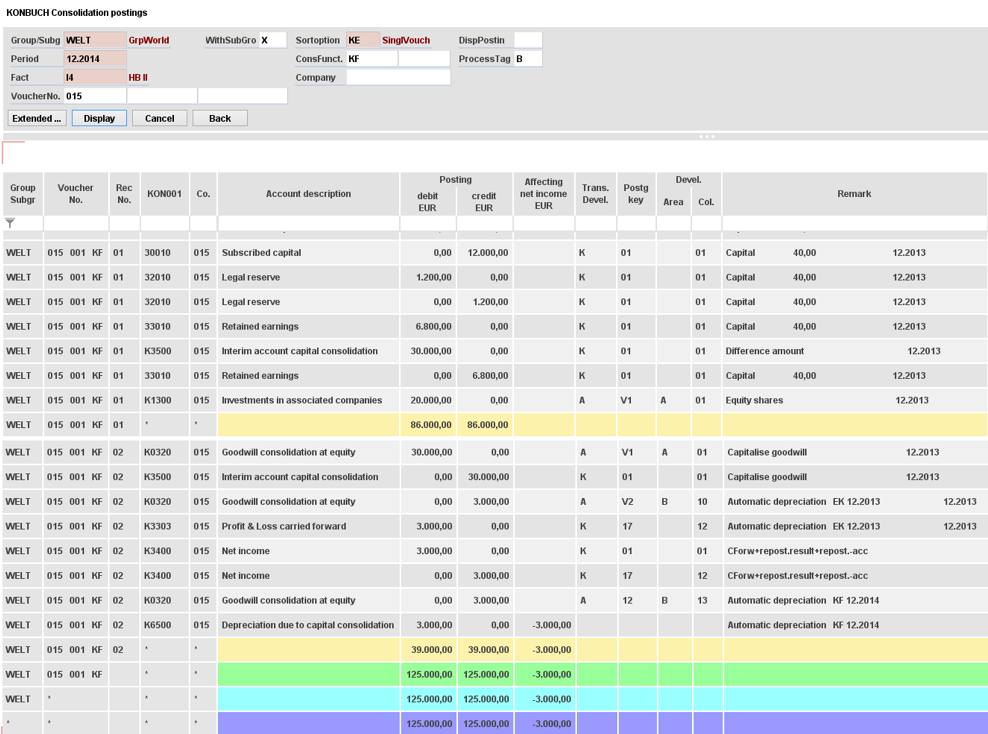

F igure: Consolidation postings of the EK V voucher subsequent period

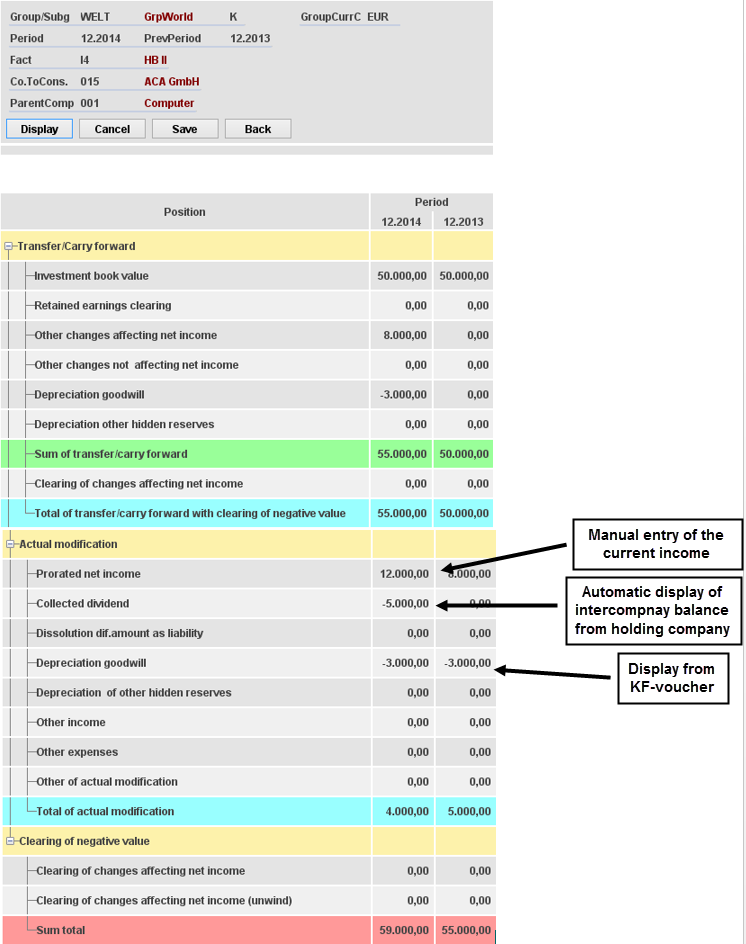

First the EF status is red; the update equity has to be carried out and displays the following:

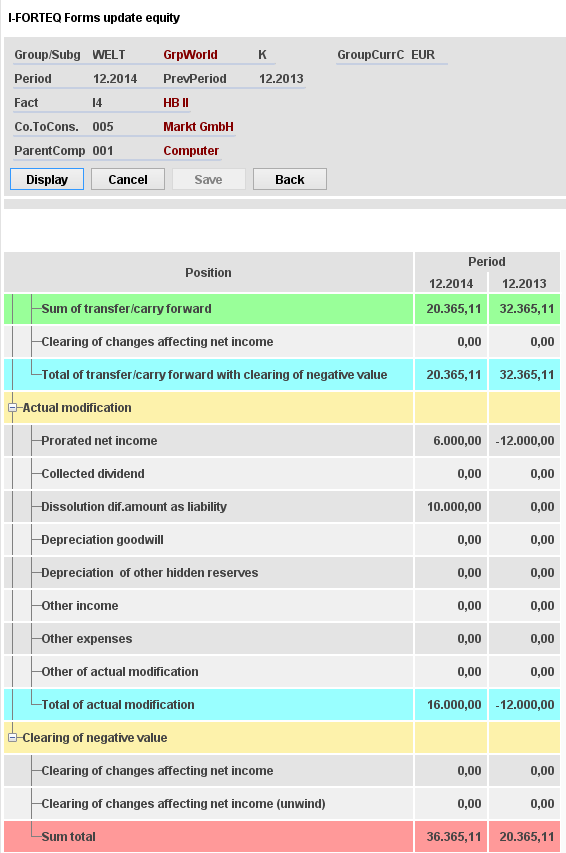

Figure: Forms Update equity subsequent period

The values from 12/2021 are displayed 1:1 in the column for the previous year. In the subsequent period 12/2022 the actual modifications posted in 12/2021 are summarized in the line "other changes affecting net income" of the upper carry-forward block. The block "actual modifica tion" shows the goodwill depreciation automatically posted in the EK V voucher. Moreover the dividend of 5,000.00 is preset. The y are to be found on the account in KTKPAREF for collected dividend in the IC balances of the parent company. You have to en ter the prorated annual result of 12,000 Euro, which results in a current book value of 59,000 Euro.

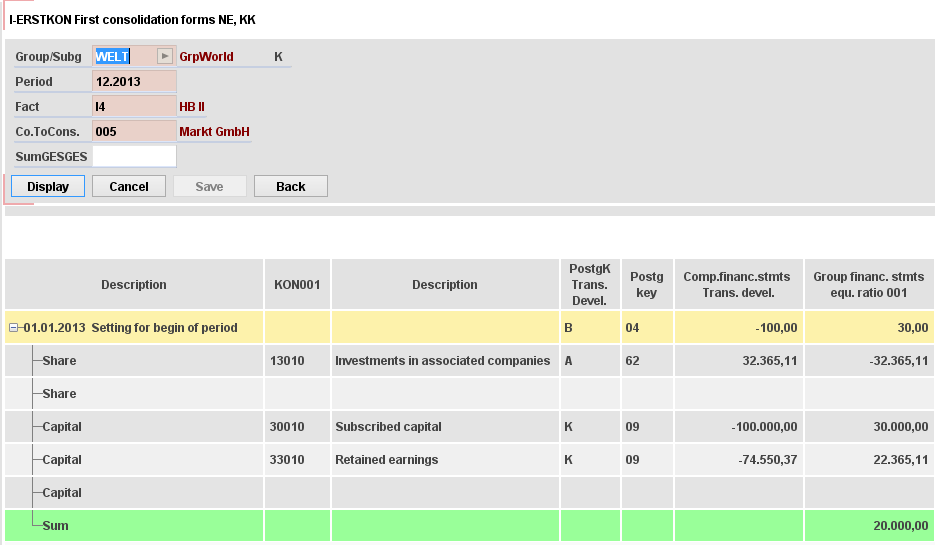

Company 001 holds 30% of company 005, which were acquired on 01.01.2021 at a price of 32,365.11 Euro and are included via the at-equity method for the f irst time in the financial year 2021.

As from the 01.01.13 the capital of the associated company is subdivi ded as follows:

| 100% | pror.30% | |

|---|---|---|

| Capital stock | 100,000.00 | 30,000.00 |

| Carry forward | 74,500. 37 | 22,365.11 |

The passive difference amount is dissolved in the subsequent years in the amount of 10,000 Euro in each case. In 2013 company 005 registers an annual loss of 40,000 Euro. In the financial year 2014 the company produces a net income of 20,000 Euro.

The first consolidation is started in the group companies + monitor via the pull-down menu " capital consolidation". For display reasons we choose the manual first consolidation. If the subsidiary has account balances or capital transactions, you can also apply the automatic first consolidation.

In the table I-ERSTKON the investment book value is copied from the shareholdings. The capital has to be entered manually, if there are no account balances available for the equity company (as it is usual).

Figure: Clearing of the shareholding with the capital in the table I-ERSTKON

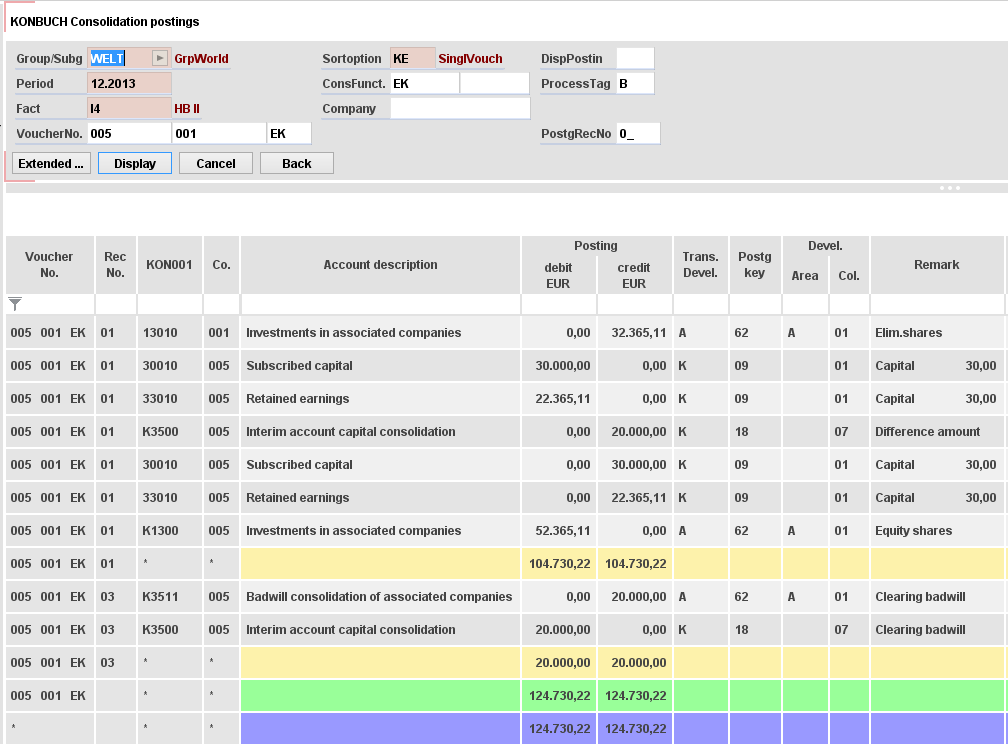

Compen sation difference from first consolidation

The difference amount is cleared with the action "compens ation difference from first consolidation" in the application VUB. The amount is posted to the account entered for EK in KTK PAR.

The following postings result from the two actions: the first consolidation with record no. 01 and the clearing of the difference amount with record no. 03.

Figure: Consolidation postings of the EK voucher

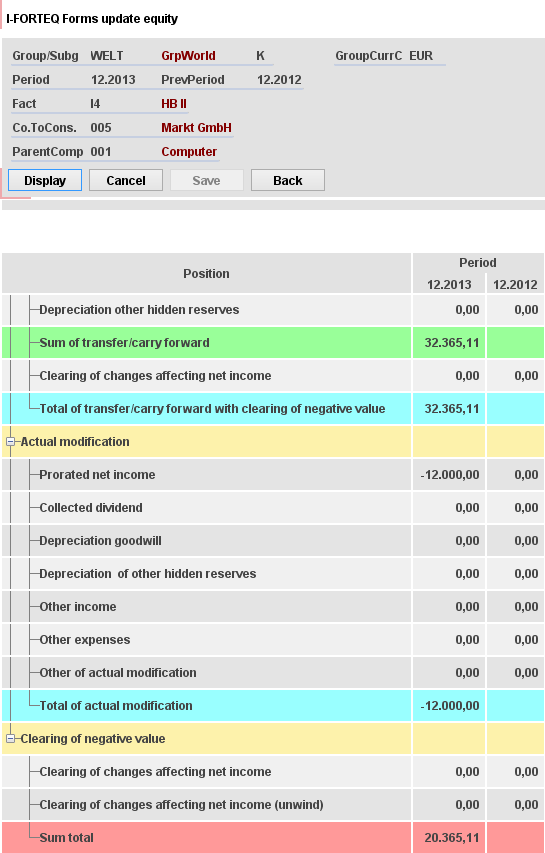

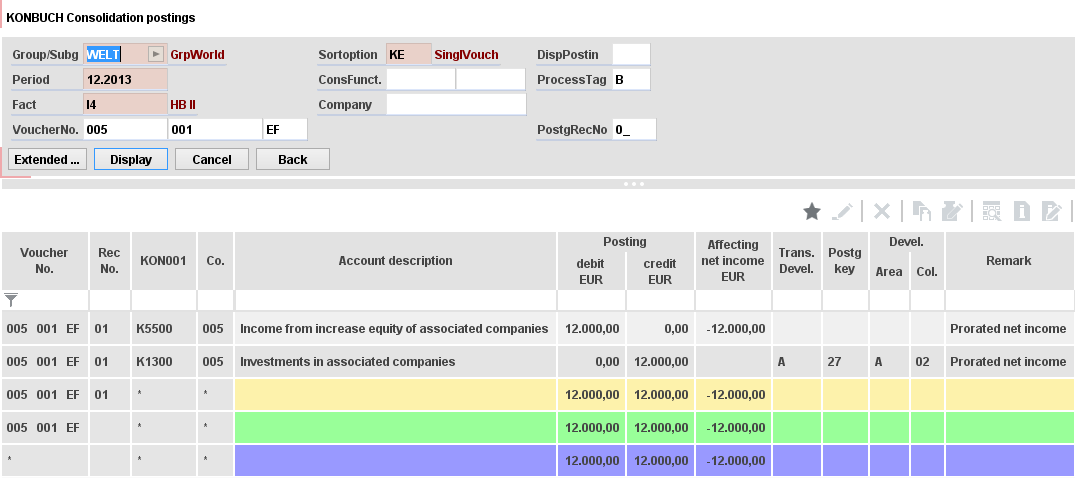

For entering the current prorated net income you open the update equity via the p ull-down menu "capital consolidation" in the group monitor or by double clicking in the column "EF". For the year 2011 you h ave to enter 30% of 40,000 Euro = 12,000 Euro with a minus, which results in a new investment book value of 20,365.11. By clicki ng on "save" the posting is written in an EF voucher. The difference amount is only meant to be dissolved proportionately in the subsequent year.

Figure: The forms data entry for the Update equity EF

The following posting has been created:

Figure: Consolidation postings of the EF voucher

Since the KTKPAREF does not contain a separate account for prorated loss, here is used the account for income.

In the report the values are displayed as follows:

Figure: Rep ort for "Investment associated company"

With the group carry forward the application automatically creates a EK V voucher, which contains th e postings of the EK and the EF voucher. For the current period you have to adjust the investment book value via the update equi ty. According to the task in this case you need to enter both the prorated net income of 6,000 Euro (30% of 20,000 Euro) and the dissolution of the difference amount as liability of 10,000 Euro.

Figure: The forms data entry for the Update equity EF in the subsequent period

Company 001 holds 30% of company 105, which were acquired for 1.00 Euro on 01.01.21. The first inclusion to the consolida tion financial statement with the at-equity method is planned for the financial year 2021 with the 01.01.21 being the date for t he first consolidation. The prorated capital amounts to:

Capital stock: 1.00 Euro

In the financial year 2021 company 105 shows a prorated net loss of 499.00 Euro, in the next period it generates a pror ated net income of 300.00 Euro.

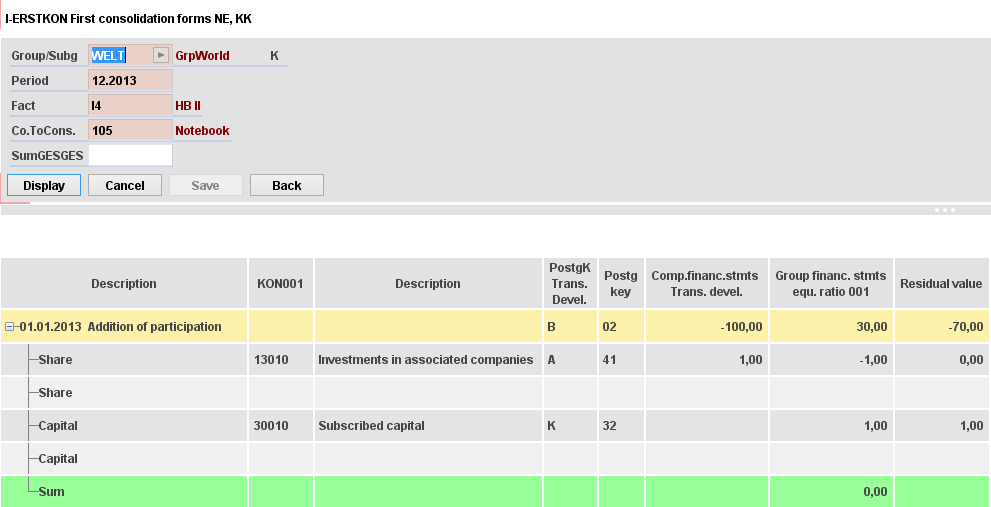

The fir st consolidation is started from the group companies + monitor and the capital of the subsidiary, which has to be eliminated, is entered in the table I-ERSTKON. Since here is not produced any difference amount, the status immediately becomes green at c hanging to the group companies + monitor.

Figure: Clearing of the shareholding with the prorated capital in the table I-ERSTKON

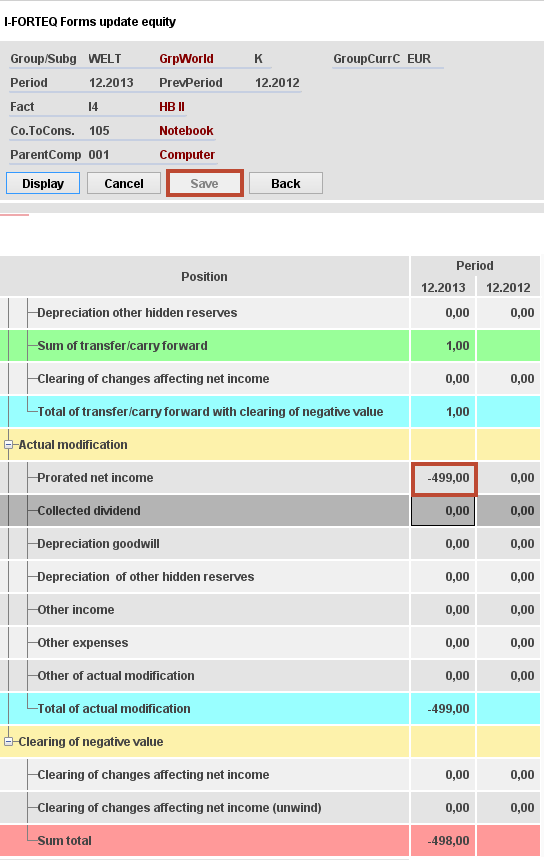

For entering the current prorated net loss of 499.00 Euro, yo u open the update equity via the pull-down menu "capital consolidation" in the group monitor or by double clicking in the co lumn "EF". This loss creates a negative book value. This value, however, must not be less than zero in the balance. For this rea son the button "save" is blocked (marked by a light grey). Now the lines in the lower block "clearing of negative value" are active and the clearing amount can be entered (as a positive value). The total sum of the clearing amounts has to adjust the fi nal sum to 0.00. Only then the button "save" is reactivated for saving the postings.

Figure: The forms data entry for the Update equity EF -> saving not possib le

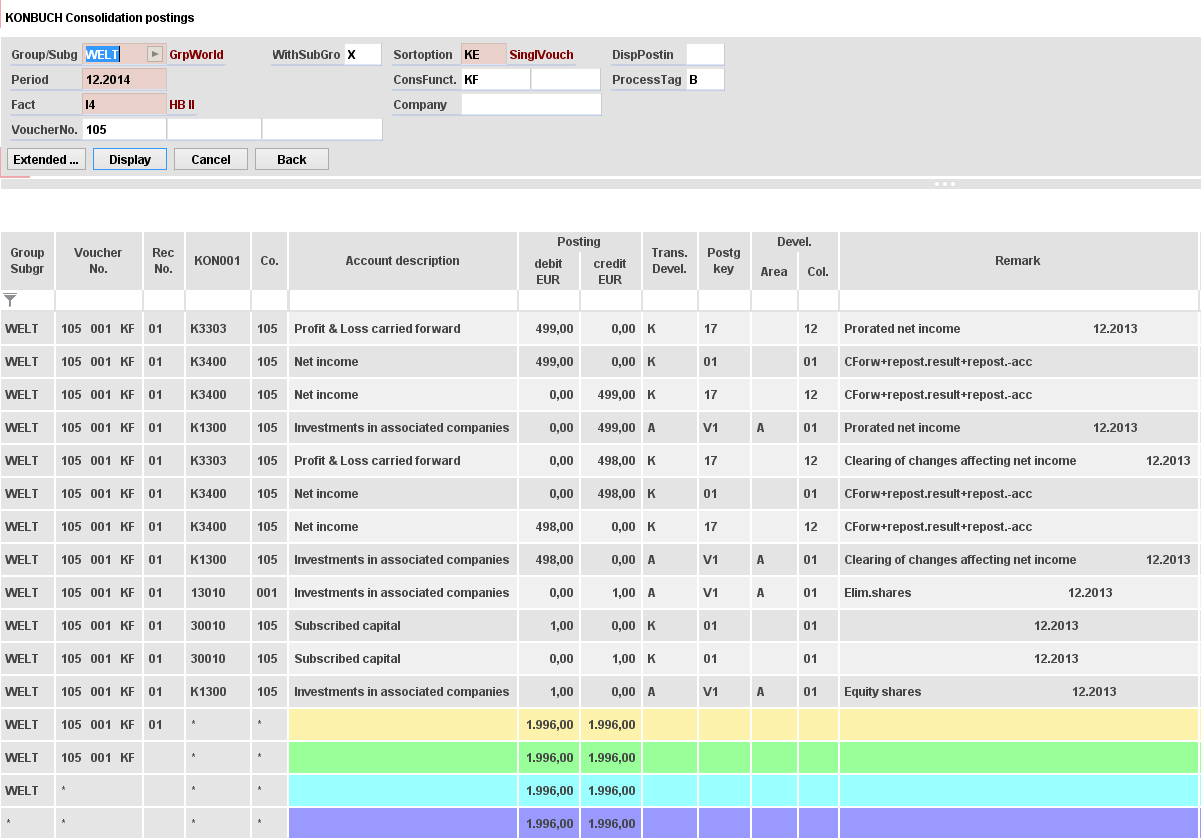

With the group carry forward the application automatically creates a EK V voucher, which contains the postings of the EK and the EF vouch er. Here the posting of the current result is not united with the clearing of the negative book value of the previous year f or always being able to keep in view the actual negative book value.

Figure: Consolidation postings of the EK V voucher

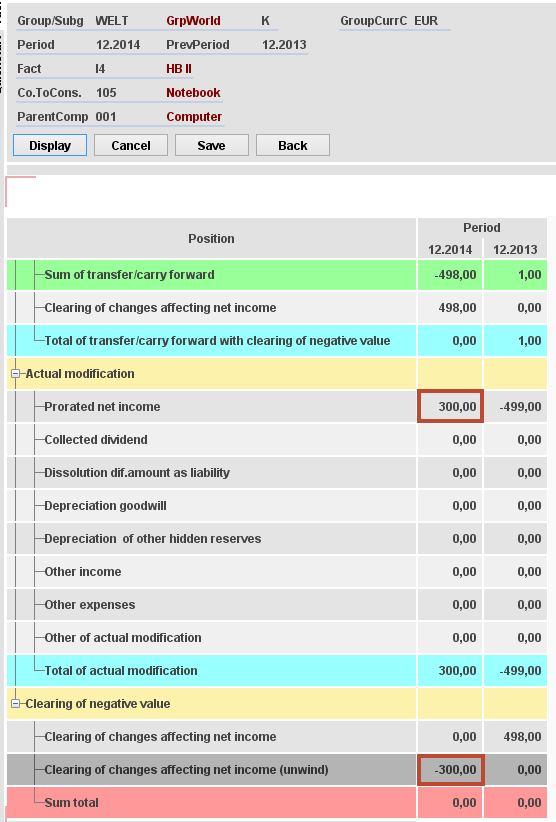

In the second year yo u have to enter a prorated net income of 300.00 Euro. After entering these 300.00 Euro, the button "save" is blocked at first (m arked with a light grey). This is due to the fact that the negative clearing of 498.00 in the upper block has been carried f orward and first has to be dissolved, before being able to raise the book value. The lines with the addition (unwind) In the blo ck "clearing of negative value" are now active. Here you have to enter the complete net income of 300.00 Euro (with a minus) thus leading to a total book value of 0.00 Euro. -198.00 Euros are carried forward to the next period as "clearing of changes a ffecting net income". Only after using them up, the book value can be changed again.

Figure: The forms data entry for the Update equity EF in the subsequent perio d